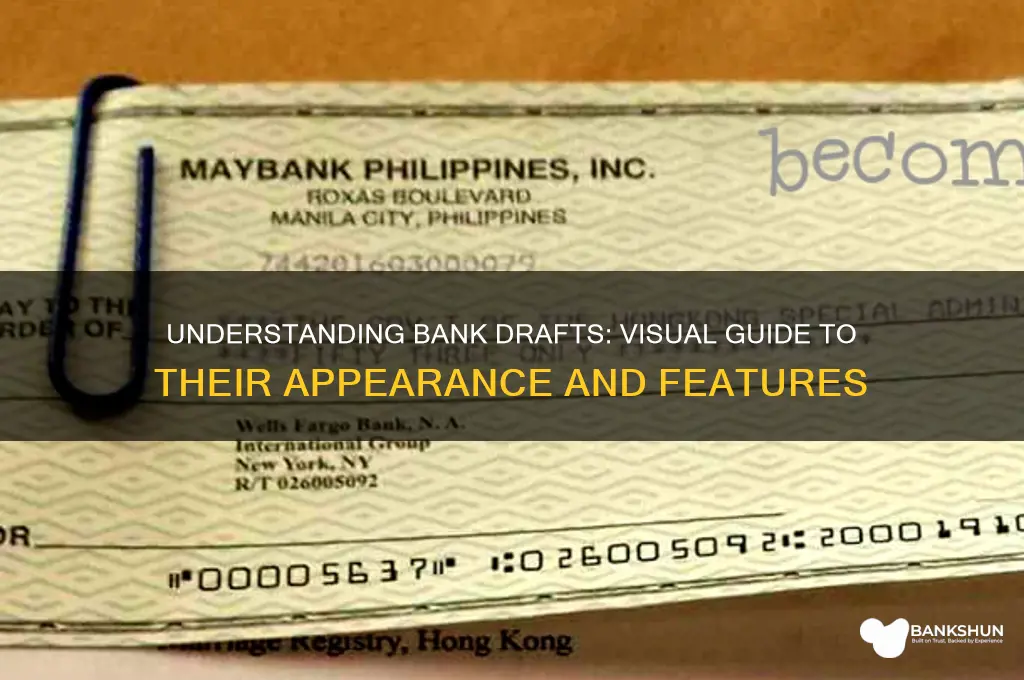

A bank draft, also known as a demand draft or banker's draft, is a secure and guaranteed payment method issued by a bank on behalf of a customer. It resembles a check but is drawn by the bank itself, ensuring the funds are pre-verified and available. Typically, a bank draft includes essential details such as the issuing bank's name, the date of issue, the payee's name, the amount in both numerical and written forms, a unique draft number, and the signature of a bank official. The document often features security elements like watermarks, holograms, or special ink to prevent fraud. Its standardized format and bank guarantee make it a trusted instrument for transactions, especially in scenarios requiring assured payments, such as international trade or large purchases.

| Characteristics | Values |

|---|---|

| Physical Appearance | Similar to a check, typically printed on special bank-issued paper with security features like watermarks, microprinting, and holograms. |

| Issuer | Issued by a bank on behalf of a customer. |

| Payee | Clearly states the name of the person or entity to whom the payment is made. |

| Amount | Specifies the exact amount to be paid, both in numerical and written form. |

| Drawer | Name of the bank issuing the draft. |

| Date of Issue | Date on which the draft is issued. |

| Drawee | Name of the bank where the draft is payable (usually a branch of the issuing bank or a correspondent bank). |

| Signature | Authorized signature of a bank official. |

| Draft Number | Unique identification number for the bank draft. |

| Security Features | May include watermarks, microprinting, holograms, and special ink to prevent forgery. |

| Instructions | May include instructions for the payee or the drawee bank. |

| Expiration Date | Some bank drafts may have an expiration date after which they cannot be cashed. |

Explore related products

What You'll Learn

- Bank Draft Header: Includes bank name, logo, and Bank Draft label for clear identification

- Payee Details: Specifies recipient's name, address, and account details for accurate payment

- Amount Section: Displays payment amount in numbers and words for verification

- Issuer Information: Contains issuing bank's details, branch, and draft number for traceability

- Security Features: Includes watermarks, holograms, and signatures to prevent fraud

![]()

Bank Draft Header: Includes bank name, logo, and Bank Draft label for clear identification

The Bank Draft Header is a critical component of a bank draft, serving as the primary means of identification and authentication. Positioned at the top of the document, it prominently displays the bank name, ensuring that the issuer of the draft is immediately recognizable. This information is typically presented in bold, clear font to avoid any ambiguity. Including the bank’s full legal name establishes trust and confirms the legitimacy of the transaction. For example, if the draft is issued by "First National Bank," this name should be clearly visible in the header to leave no room for confusion.

Adjacent to or integrated with the bank name, the bank logo is another essential element of the header. The logo acts as a visual identifier, reinforcing the bank’s brand and adding a layer of security. A well-designed logo not only enhances the professional appearance of the draft but also makes it harder to counterfeit. It is often placed to the left or right of the bank name, ensuring it is immediately noticeable. The logo should be high-resolution and consistent with the bank’s official branding guidelines to maintain authenticity.

The Bank Draft label is the third key component of the header, explicitly stating the nature of the document. This label is typically written in capitalized, bold letters, such as "BANK DRAFT," to distinguish it from other financial instruments like checks or money orders. Its placement is strategic, usually centered or aligned with the bank name and logo, to ensure it catches the recipient’s attention. This label leaves no doubt about the purpose and type of the document, facilitating quick recognition and processing.

The design and layout of the Bank Draft Header are intentionally straightforward to prioritize clarity and functionality. The bank name, logo, and draft label are often enclosed within a bordered section or a shaded area to set them apart from the rest of the document. This visual separation ensures that the header stands out, even at a glance. Additionally, the use of contrasting colors or fonts may be employed to further emphasize these elements, making the header both professional and easy to read.

Instructively, when creating or reviewing a bank draft, it is crucial to verify that the Bank Draft Header includes all three elements: the bank name, logo, and draft label. Omitting any of these could lead to delays in processing or questions about the draft’s validity. For recipients, the header serves as the first line of verification, providing immediate assurance that the document is genuine and issued by a recognized financial institution. Thus, the header is not just a design feature but a fundamental aspect of the bank draft’s security and functionality.

Ancient Greek Banking Origins: A Journey Through Early Financial Systems

You may want to see also

Explore related products

![]()

Payee Details: Specifies recipient's name, address, and account details for accurate payment

When examining a bank draft, one of the most critical sections is the Payee Details, which ensures the payment reaches the correct recipient without errors. This section is meticulously structured to include the recipient’s full name, as it appears in their official records, to avoid any discrepancies that could delay or misdirect the payment. The name must be spelled accurately, including any middle names or initials, as banks often require exact matches for processing. This precision is essential because even a minor error, such as a misspelled name, can render the draft invalid or cause complications in the payment process.

Following the recipient’s name, the Payee Details section includes the recipient’s complete address. This address should be current and detailed, encompassing the street name, house or building number, city, state, and postal code. The inclusion of the address serves a dual purpose: it verifies the recipient’s identity and provides a physical location for correspondence if needed. Banks use this information to cross-reference the payee’s details with their records, ensuring the payment is directed to the intended individual or entity. In some cases, international bank drafts may also require the country name to facilitate cross-border transactions.

Another vital component of the Payee Details is the recipient’s account information. This typically includes the account number and, in some cases, the bank’s routing number or SWIFT code, especially for international transactions. The account number is crucial as it directly links the payment to the recipient’s bank account, ensuring the funds are deposited accurately. For added security, some bank drafts may also include the recipient’s bank name and branch details, further minimizing the risk of errors. It is imperative that this information is filled out correctly, as incorrect account details can result in failed transactions or funds being sent to the wrong account.

The Payee Details section is often designed with clear labels and fields to prevent confusion. For instance, fields may be explicitly marked as "Payee Name," "Payee Address," and "Account Number," making it easy for both the issuer and the bank to verify the information. This clarity is particularly important in financial documents, where precision is paramount. Additionally, the section may include instructions or notes, such as "Ensure all details match the recipient’s bank records," to guide the person filling out the draft and reduce the likelihood of mistakes.

Lastly, the Payee Details section is usually accompanied by security features to protect against fraud. These may include watermarks, holograms, or microprinting around the area where the recipient’s details are entered. Such measures ensure that the bank draft is authentic and that the payee’s information has not been tampered with. By combining detailed, accurate information with robust security features, the Payee Details section plays a pivotal role in the functionality and reliability of a bank draft, guaranteeing that payments are processed smoothly and securely.

Buy Gold and Silver Coins at Banks: A Smart Investment?

You may want to see also

Explore related products

![]()

Amount Section: Displays payment amount in numbers and words for verification

The Amount Section of a bank draft is a critical component designed to ensure clarity and prevent fraud. This section typically appears prominently on the draft, often in a designated box or area that immediately draws the eye. The primary purpose of this section is to display the payment amount in two formats: numerical figures and written words. This dual representation serves as a verification tool, allowing both the payer and the payee to confirm the exact amount being transferred. For example, if the amount is $1,500, it will be written as "1,500.00" in numbers and "One Thousand Five Hundred and 00/100" in words. This redundancy ensures that there is no ambiguity regarding the payment amount.

In the numerical format, the amount is usually printed in a clear, bold font to make it easily readable. It is often accompanied by a currency symbol, such as "$" for USD, and includes decimal places to denote cents or smaller denominations. The numerical representation is straightforward and universally understood, making it a quick reference for both parties involved in the transaction. Additionally, the use of a standardized font and formatting reduces the risk of misinterpretation or tampering.

The written format, on the other hand, spells out the amount in words, followed by a fraction indicating the cents or smaller units. This format is particularly important as it provides a secondary verification method. For instance, "One Thousand Five Hundred and 00/100" leaves no room for confusion, as it explicitly states the amount in a language-based format. This dual representation is a security feature, as altering one without the other would be immediately noticeable, thus deterring fraudulent activities.

The Amount Section is often accompanied by additional security features, such as watermarks, microprinting, or special inks, to further protect against counterfeiting. These features are especially important given the financial significance of a bank draft. The placement of this section is also strategic, usually near the center or top of the draft, ensuring it is one of the first details noticed by anyone reviewing the document.

Finally, the Amount Section is legally binding and must match the amount indicated in the transaction request. Any discrepancy between the numerical and written amounts would render the bank draft invalid. Therefore, both the issuing bank and the recipient must carefully verify this section to ensure accuracy. This meticulous attention to detail underscores the importance of the Amount Section in maintaining the integrity and reliability of bank drafts as a secure payment instrument.

How Banks Verify Social Security Numbers: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Issuer Information: Contains issuing bank's details, branch, and draft number for traceability

A bank draft is a secure and reliable financial instrument, and its design includes several key elements to ensure authenticity and traceability. One of the most critical sections is the Issuer Information, which provides essential details about the bank that issued the draft. This section typically appears at the top of the document, prominently displaying the name of the issuing bank in bold, clear lettering. The bank’s name is often accompanied by its official logo, which serves as a visual identifier and adds an extra layer of security. This information is crucial as it confirms the legitimacy of the draft and establishes the bank’s responsibility for the transaction.

Beneath the bank’s name, the Issuer Information section includes the specific branch details where the draft was issued. This includes the branch name, address, and sometimes even the contact information such as phone number or email. The inclusion of branch details is vital for traceability, as it allows recipients or verifying parties to contact the exact location where the draft originated. This ensures that any discrepancies or inquiries can be addressed directly with the responsible branch, streamlining the verification process and enhancing trust in the instrument.

Another critical component of the Issuer Information is the draft number, a unique identifier assigned to each bank draft. This number is typically a combination of letters and digits, designed to be distinct from all other drafts issued by the bank. The draft number serves as a reference point for both the issuing bank and the recipient, enabling easy tracking of the transaction within the bank’s system. It is often printed in a prominent location, such as the top-right corner, and may be accompanied by a barcode or QR code for quick scanning and verification.

The Issuer Information section is also where the date of issuance is recorded, providing a timestamp for the transaction. This date is important for determining the validity period of the draft, as bank drafts typically have an expiration date. Additionally, some drafts may include a watermark or security feature in the background of this section, further safeguarding against fraud. These elements collectively ensure that the Issuer Information is not only informative but also secure, reinforcing the integrity of the bank draft as a financial instrument.

In summary, the Issuer Information on a bank draft is a meticulously designed section that includes the issuing bank’s details, branch information, and a unique draft number. These elements work together to provide traceability, authenticity, and accountability, making the bank draft a trusted method for transferring funds. By clearly displaying this information, the draft ensures transparency and facilitates smooth transactions between parties, whether for personal or business purposes. Understanding this section is essential for anyone handling a bank draft, as it forms the foundation of the document’s reliability and security.

Does SunTrust Bank Hire English-Speaking Agents? Exploring Job Opportunities

You may want to see also

Explore related products

![]()

Security Features: Includes watermarks, holograms, and signatures to prevent fraud

Bank drafts are designed with robust security features to prevent fraud and ensure authenticity. One of the primary security measures is the use of watermarks, which are embedded directly into the paper during the manufacturing process. These watermarks are typically visible when held up to light and often display the bank’s logo, name, or other unique identifiers. Counterfeiters find it extremely difficult to replicate watermarks accurately, making them a critical deterrent against forgery. When examining a bank draft, always look for these subtle, integrated designs to verify its legitimacy.

Another advanced security feature is the inclusion of holograms, which are three-dimensional images that shift or change appearance when viewed from different angles. Holograms on bank drafts are often placed in strategic locations, such as the corners or center, and may contain intricate patterns, logos, or text. Their complexity and sensitivity to movement make them nearly impossible to reproduce with standard printing techniques. To authenticate a bank draft, tilt it under light and observe the hologram for the expected visual changes, ensuring it is not a static or poorly replicated image.

Signatures also play a vital role in the security of bank drafts. These documents typically bear the authorized signatures of bank officials, which are verified and recorded internally. Genuine signatures are often accompanied by a unique signing style, ink type, or even specialized pens that leave a distinct mark. Additionally, some bank drafts may include a second line of defense, such as a machine-printed signature or a digital signature verification code, to further enhance security. Always compare the signatures on the draft with known samples or contact the issuing bank if there is any doubt about their authenticity.

To strengthen fraud prevention, bank drafts often combine these features in a multi-layered security approach. For instance, watermarks and holograms may be positioned in a way that overlaps or complements each other, making it harder for counterfeiters to tamper with the document without detection. Similarly, signatures are usually placed near other security elements, such as holograms or microprinting, to create an integrated security network. When inspecting a bank draft, consider the overall design and how these features work together to protect against unauthorized alterations.

Lastly, it is essential to familiarize yourself with the specific security features of the bank issuing the draft, as these can vary. Many banks provide guidelines or sample images of their drafts online, highlighting the unique watermarks, holograms, and signature placements. If you are handling a bank draft, take the time to cross-reference these details with the provided resources. In case of uncertainty, always consult the issuing bank directly to confirm the draft’s authenticity and ensure you are not dealing with a fraudulent document.

The Future of Banking: What's Next for Banks?

You may want to see also

Frequently asked questions

A bank draft is a payment instrument issued by a bank, guaranteeing funds availability. Unlike a regular check, which draws funds directly from the payer’s account, a bank draft is prepaid, ensuring the recipient receives the full amount.

A bank draft usually includes the issuing bank’s name, the payer’s name, the recipient’s name, the amount in words and numbers, a unique draft number, issue date, and the bank’s signature or stamp.

Yes, a bank draft typically resembles a check but is printed on official bank stationery. It often includes security features like watermarks, holograms, or special ink to prevent fraud.

Yes, there are different types, such as cashier’s checks and demand drafts. While they share a similar format, cashier’s checks are often more secure and may include additional features like a bank officer’s signature, whereas demand drafts may vary slightly in design depending on the issuing bank.