Banks play a crucial role in clearing derivatives by acting as intermediaries that facilitate the smooth and efficient settlement of these complex financial instruments. Derivatives, such as futures, options, and swaps, derive their value from underlying assets, and their trading involves significant counterparty risk. To mitigate this risk, banks often serve as central counterparties (CCPs) in clearinghouses, stepping in between buyers and sellers to guarantee the fulfillment of contractual obligations. By collecting margin requirements, monitoring positions, and managing default risks, banks ensure that derivative transactions are settled securely and transparently. This process not only reduces systemic risk but also enhances market liquidity and stability, making derivatives more accessible to a broader range of participants.

| Characteristics | Values |

|---|---|

| Role as Central Counterparty (CCP) | Banks act as CCPs, guaranteeing trades and reducing counterparty risk. |

| Margin Requirements | Collect initial and variation margins to cover potential losses. |

| Trade Confirmation | Validate and confirm derivative trades between counterparties. |

| Netting | Offset multiple positions to reduce exposure and margin requirements. |

| Settlement | Facilitate cash or physical settlements for derivative contracts. |

| Risk Management | Monitor and manage systemic risk through stress testing and analysis. |

| Regulatory Compliance | Ensure adherence to regulations like Dodd-Frank and EMIR. |

| Transparency | Provide trade reporting and data to regulators and market participants. |

| Collateral Management | Handle collateral posting, rehypothecation, and optimization. |

| Default Management | Manage default scenarios, including auctioning defaulted positions. |

| Technology Infrastructure | Provide platforms for trade matching, clearing, and reporting. |

| Liquidity Provision | Act as market makers to enhance liquidity in derivative markets. |

| Fee Structure | Charge clearing fees, margin fees, and other transaction-related fees. |

| Global Reach | Offer clearing services across multiple jurisdictions and currencies. |

| Innovation | Develop new clearing solutions for complex or emerging derivatives. |

Explore related products

What You'll Learn

- Central Counterparty Clearing (CCP): Acts as intermediary, reducing counterparty risk in derivative transactions

- Margin Requirements: Ensures sufficient collateral to cover potential losses in derivative positions

- Novation Process: Transfers derivative contracts to the CCP, simplifying risk management

- Settlement Mechanisms: Facilitates timely and accurate payment of derivative obligations

- Risk Monitoring: Continuously assesses and mitigates risks associated with derivative exposures

![]()

Central Counterparty Clearing (CCP): Acts as intermediary, reducing counterparty risk in derivative transactions

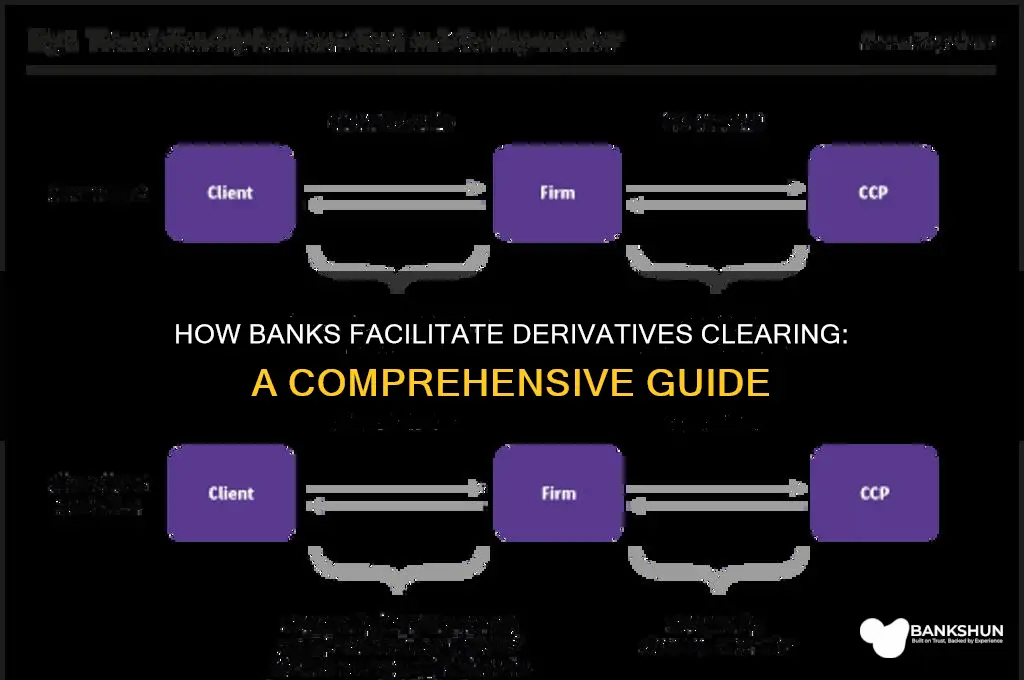

Central Counterparty Clearing (CCP) plays a pivotal role in the derivatives market by acting as an intermediary between buyers and sellers, thereby significantly reducing counterparty risk. When a derivative transaction is executed, instead of the two parties directly exchanging obligations, the CCP steps in to become the buyer to every seller and the seller to every buyer. This process, known as novation, ensures that neither party is exposed to the default risk of the other. For instance, if Party A buys a derivative from Party B, the CCP becomes Party A’s seller and Party B’s buyer, effectively guaranteeing the trade’s fulfillment regardless of either party’s financial health.

One of the primary ways CCPs mitigate counterparty risk is through robust risk management frameworks. CCPs require participants to post initial margin—collateral upfront—to cover potential losses in case of default. Additionally, variation margin is collected daily to account for price fluctuations in the derivative’s value. These margin requirements are determined using sophisticated models that assess market volatility, liquidity, and other risk factors. By ensuring sufficient collateral is in place, CCPs protect all participants from the financial fallout of a counterparty’s default.

Banks play a critical role in facilitating CCP clearing by acting as clearing members. These banks provide access to CCP services for their clients, who may not meet the stringent membership requirements. Clearing members are responsible for posting margins on behalf of their clients, ensuring compliance with CCP rules, and managing the operational aspects of clearing. In return, banks earn fees for their services, while also benefiting from reduced counterparty risk in their own derivative transactions. This intermediary role of banks is essential for broadening access to CCP clearing and enhancing market stability.

CCPs also contribute to market transparency and standardization. By centralizing clearing, CCPs aggregate transaction data, allowing regulators and market participants to monitor systemic risk more effectively. Furthermore, CCPs typically clear standardized derivative contracts, reducing complexity and increasing liquidity in the market. This standardization ensures that derivatives are more easily valued and traded, which is particularly important during periods of market stress. Banks leverage this transparency to better manage their own risk exposures and provide more reliable services to their clients.

In summary, Central Counterparty Clearing (CCP) acts as a critical intermediary in derivative transactions, significantly reducing counterparty risk through novation, margin requirements, and robust risk management practices. Banks, as clearing members, facilitate access to CCP services, ensuring broader market participation and stability. By centralizing clearing, CCPs enhance transparency, standardize contracts, and provide a safer environment for derivative trading. This collaborative framework between CCPs and banks is essential for maintaining the integrity and efficiency of the global derivatives market.

How to Get a Cash Advance with Bank of the West

You may want to see also

Explore related products

![]()

Margin Requirements: Ensures sufficient collateral to cover potential losses in derivative positions

Margin requirements are a critical component of how banks help clear derivatives, serving as a safeguard to ensure that all parties involved in derivative transactions can meet their financial obligations. When a bank acts as a clearinghouse or intermediary for derivative trades, it imposes margin requirements on the counterparties to mitigate the risk of default. These requirements mandate that traders deposit a certain amount of collateral, typically in the form of cash or securities, to cover potential losses that may arise from adverse price movements in the derivative positions. By doing so, banks create a buffer that protects both the bank and the trading parties from significant financial harm in volatile market conditions.

The calculation of margin requirements is based on sophisticated risk models that assess the potential exposure of derivative positions. These models consider factors such as the type of derivative, its underlying asset, market volatility, and the time to maturity. For instance, highly volatile assets or long-dated derivatives typically require higher margins due to the increased risk of substantial price swings. Banks use these models to determine the initial margin, which is the collateral required when a position is first opened, and the variation margin, which adjusts the collateral based on daily changes in the position’s value. This dynamic approach ensures that margin levels remain adequate to cover losses as market conditions evolve.

Margin requirements also play a key role in maintaining the integrity of the financial system by reducing counterparty risk. In over-the-counter (OTC) derivative markets, where trades are privately negotiated, the lack of a centralized clearinghouse can expose parties to significant risk if a counterparty defaults. Banks, acting as clearing agents, centralize this risk by requiring margins from both parties and stepping in as intermediaries. If one party fails to meet its obligations, the bank uses the posted margin to cover the losses, ensuring that the other party is protected. This mechanism fosters trust and stability in derivative markets, encouraging greater participation and liquidity.

Furthermore, margin requirements are closely monitored and enforced through regular margin calls. If the value of a derivative position moves against a trader, the bank may issue a margin call, demanding additional collateral to restore the margin to the required level. Failure to meet a margin call can result in the bank liquidating the trader’s position to recover the shortfall, thereby limiting the bank’s exposure to loss. This process underscores the importance of margin requirements in maintaining discipline among market participants and preventing excessive risk-taking.

In summary, margin requirements are a cornerstone of how banks help clear derivatives by ensuring sufficient collateral to cover potential losses. Through rigorous risk assessment, dynamic margin adjustments, and strict enforcement, banks mitigate counterparty risk, protect market participants, and uphold the stability of the financial system. By requiring traders to post collateral, banks create a robust framework that facilitates the safe and efficient trading of derivatives, even in highly volatile markets.

Steps to Becoming a Successful Mortgage Banker

You may want to see also

Explore related products

![]()

Novation Process: Transfers derivative contracts to the CCP, simplifying risk management

The novation process is a critical mechanism through which banks facilitate the clearing of derivative contracts, transferring them to a Central Counterparty Clearing House (CCP). This process begins when two counterparties agree to transfer their existing bilateral derivative contract to the CCP. Upon novation, the CCP steps in as the legal counterparty to both the buyer and the seller, effectively replacing the original bilateral agreement with two separate agreements: one between the CCP and each counterparty. This transformation centralizes counterparty risk, as the CCP assumes the responsibility for ensuring that both parties fulfill their obligations. By doing so, the novation process reduces the complexity of managing multiple bilateral exposures and streamlines risk management for banks and other market participants.

Once the novation is executed, the CCP imposes margin requirements on both counterparties to mitigate potential losses in case of default. These margins, which include initial margin (to cover potential future exposure) and variation margin (to cover daily gains or losses), are calculated based on the CCP’s risk models and market conditions. Banks play a pivotal role in this stage by ensuring compliance with margin calls, managing collateral, and maintaining sufficient liquidity to meet these obligations. The use of standardized margin requirements across all participants enhances transparency and reduces the likelihood of disputes, further simplifying risk management for banks involved in derivative transactions.

Another key benefit of the novation process is the application of standardized contracts by the CCP. Bilateral derivative contracts often vary in terms and conditions, making them difficult to compare and manage. However, when these contracts are novated to the CCP, they are converted into standardized formats, which facilitates easier valuation, netting, and risk assessment. Banks benefit from this standardization as it reduces operational complexity and allows for more efficient allocation of resources. Additionally, standardized contracts enable better risk aggregation across the bank’s portfolio, providing a clearer picture of overall exposure.

The novation process also enhances risk management through the CCP’s default management framework. In the event of a counterparty default, the CCP steps in to manage the situation, using the defaulting party’s margins and default fund contributions to cover losses. This mechanism protects non-defaulting counterparties, including banks, from direct exposure to the default. Banks contribute to the CCP’s default fund as part of their membership obligations, further strengthening the system’s resilience. By centralizing default management, the novation process reduces the systemic risk associated with derivative transactions and ensures that banks can continue to operate with confidence in the market.

Finally, the novation process supports regulatory compliance for banks by aligning derivative transactions with global standards such as the Dodd-Frank Act and EMIR. These regulations mandate the clearing of certain derivatives through CCPs to increase market transparency and reduce systemic risk. By participating in the novation process, banks demonstrate adherence to these regulatory requirements, avoiding potential penalties and reputational damage. Moreover, the centralized clearing model provides regulators with better visibility into market activities, enabling more effective oversight. In this way, the novation process not only simplifies risk management for banks but also contributes to the overall stability of the financial system.

Does US Bank App Include Zelle? A Comprehensive Guide

You may want to see also

Explore related products

$10.17 $16.99

![]()

Settlement Mechanisms: Facilitates timely and accurate payment of derivative obligations

Banks play a crucial role in facilitating the timely and accurate payment of derivative obligations through robust settlement mechanisms. These mechanisms are designed to ensure that all parties involved in a derivative transaction fulfill their financial commitments efficiently and securely. One of the primary ways banks achieve this is by acting as intermediaries in the clearing process. When a derivative trade is executed, the bank, often through a central clearinghouse, steps in to guarantee the settlement, reducing counterparty risk. This involves matching the obligations of buyers and sellers, ensuring that payments are made as agreed upon in the contract terms.

To streamline settlement, banks employ automated systems that process large volumes of transactions with precision and speed. These systems are integrated with real-time payment networks, enabling instantaneous or near-instantaneous transfers of funds. For instance, in over-the-counter (OTC) derivatives, banks use multilateral netting processes to consolidate multiple obligations into a single net payment, minimizing the number of transactions and reducing settlement risk. This netting process is particularly critical in complex derivative portfolios, where numerous trades may be outstanding between counterparties.

Another key aspect of settlement mechanisms is the use of collateral management systems. Banks require counterparties to post collateral, such as cash or securities, to mitigate credit risk associated with derivative positions. These systems ensure that collateral is adjusted daily based on market movements, a process known as margin calls. By managing collateral effectively, banks provide an additional layer of security, ensuring that funds are available to cover obligations even if one party defaults.

Banks also facilitate settlement by adhering to standardized processes and regulatory frameworks, such as those outlined by the Dodd-Frank Act or EMIR (European Market Infrastructure Regulation). These regulations mandate central clearing for certain derivatives, enhancing transparency and reducing systemic risk. Banks act as clearing members, interfacing between clients and central counterparties (CCPs), and ensuring compliance with regulatory requirements. This includes reporting trades, managing margin requirements, and settling obligations in a standardized manner.

Lastly, banks provide reconciliation and reporting services to ensure accuracy in derivative settlements. They maintain detailed records of all transactions, reconcile discrepancies, and generate reports for both internal and external stakeholders. This transparency is vital for audit purposes and for maintaining trust among counterparties. By combining advanced technology, regulatory compliance, and risk management practices, banks ensure that derivative obligations are settled in a timely, accurate, and secure manner, thereby supporting the integrity of the financial markets.

Banking Hours: New Year's Eve Operations

You may want to see also

Explore related products

![]()

Risk Monitoring: Continuously assesses and mitigates risks associated with derivative exposures

Banks play a critical role in clearing derivatives by acting as intermediaries that manage and mitigate the risks associated with these complex financial instruments. One of the core functions in this process is Risk Monitoring, which involves the continuous assessment and mitigation of risks tied to derivative exposures. This is essential to ensure the stability of both the bank and the broader financial system. Risk monitoring is a multifaceted process that requires sophisticated tools, methodologies, and expertise to identify, measure, and address potential threats in real time.

To effectively monitor risks, banks employ advanced risk management frameworks that include stress testing, scenario analysis, and value-at-risk (VaR) models. These tools help quantify the potential losses that could arise from adverse market movements, counterparty defaults, or other risk factors. For instance, stress testing involves simulating extreme market conditions to evaluate the resilience of the bank’s derivative portfolio. Scenario analysis, on the other hand, assesses the impact of specific events, such as interest rate hikes or currency fluctuations, on the portfolio’s value. By integrating these methodologies, banks gain a comprehensive understanding of their risk exposure and can take proactive measures to mitigate it.

Counterparty risk is another critical aspect of risk monitoring in derivative clearing. Banks continuously evaluate the creditworthiness of counterparties to ensure they can fulfill their obligations. This includes monitoring credit ratings, collateral requirements, and margin calls. Margin requirements, in particular, are adjusted dynamically based on market volatility and the risk profile of the derivative positions. If a counterparty’s risk profile deteriorates, the bank may demand additional collateral or liquidate positions to protect itself from potential defaults. This proactive approach minimizes the likelihood of financial losses and maintains the integrity of the clearing process.

Liquidity risk is also a key focus in risk monitoring. Derivatives markets can experience sudden illiquidity, making it difficult to exit positions or hedge risks. Banks address this by maintaining sufficient liquidity buffers and diversifying their portfolios to reduce concentration risk. Additionally, they monitor market depth and trading volumes to anticipate potential liquidity constraints. By staying ahead of liquidity issues, banks ensure they can meet their obligations and continue to facilitate smooth derivative transactions.

Finally, operational risk is an integral part of risk monitoring in derivative clearing. Banks implement robust internal controls, compliance protocols, and technology systems to prevent errors, fraud, or system failures. Regular audits and risk assessments are conducted to identify vulnerabilities and implement corrective actions. Operational resilience is further enhanced through contingency plans and backup systems that ensure continuity in the event of disruptions. By addressing operational risks, banks safeguard the efficiency and reliability of the clearing process.

In summary, risk monitoring is a cornerstone of how banks help clear derivatives. Through continuous assessment and mitigation of risks—including market, counterparty, liquidity, and operational risks—banks ensure the stability and integrity of derivative transactions. This proactive approach not only protects the bank’s financial health but also contributes to the overall resilience of the financial system. By leveraging advanced tools, methodologies, and expertise, banks play a vital role in managing the complexities of derivative clearing.

Deutsche Bank's Unique Approach: Differentiating Factors from Competitors

You may want to see also

Frequently asked questions

A bank acts as a clearing member, facilitating the settlement and risk management of derivative transactions by ensuring both parties meet their obligations.

Banks use central clearing counterparties (CCPs) to act as intermediaries, guaranteeing trades and reducing the risk of default by either party.

Banks offer margin management, collateral services, trade confirmation, and reporting to ensure smooth and compliant clearing processes.

Banks provide the infrastructure, expertise, and capital required to manage the complexity and risks associated with OTC derivatives, ensuring market stability.