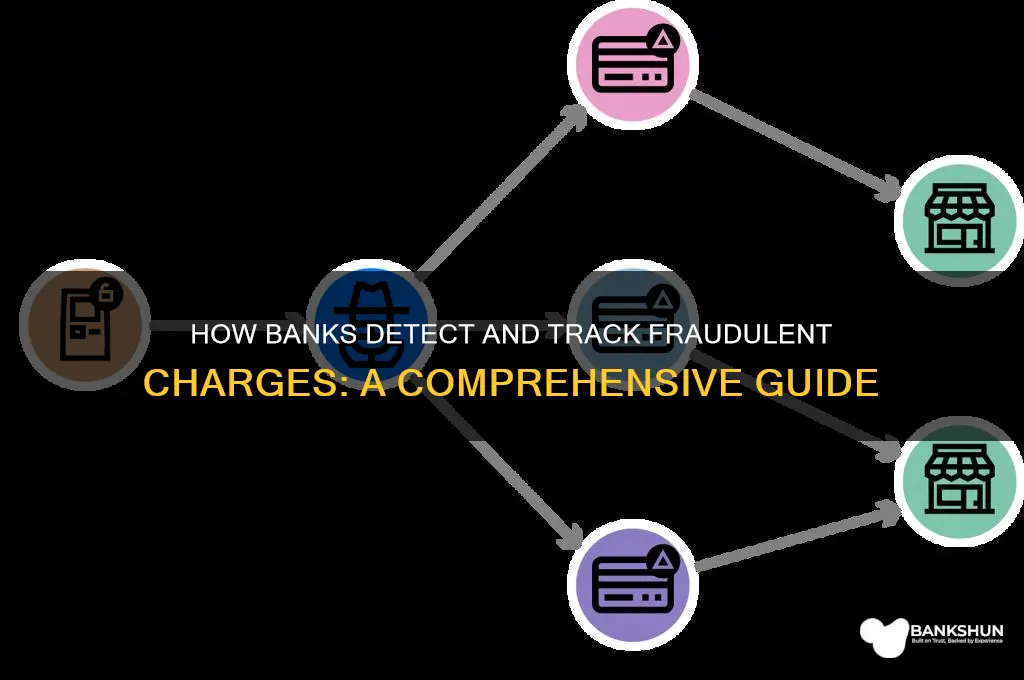

Banks employ sophisticated systems and technologies to track and prevent fraudulent charges, leveraging a combination of real-time monitoring, advanced algorithms, and machine learning. When a transaction occurs, the bank’s fraud detection system analyzes patterns, such as spending habits, location, and transaction size, to identify anomalies that deviate from the account holder’s typical behavior. Suspicious activities trigger alerts, prompting further investigation by the bank’s security team or automated systems. Additionally, banks use encryption, tokenization, and secure networks to protect customer data, while collaboration with global fraud databases and regulatory bodies helps identify known fraudulent schemes. Customers also play a role by receiving instant notifications and reporting unauthorized charges promptly, enabling banks to act swiftly to freeze accounts, reverse transactions, and minimize financial loss.

| Characteristics | Values |

|---|---|

| Transaction Monitoring Systems | Banks use AI and machine learning algorithms to analyze transaction patterns in real-time. |

| Behavioral Analysis | Tracks spending habits, location, and frequency to detect anomalies. |

| Geolocation Checks | Flags transactions occurring in unusual or impossible locations based on user history. |

| Velocity Checks | Monitors rapid, multiple transactions in a short period as potential fraud indicators. |

| Device Fingerprinting | Identifies devices used for transactions to detect unauthorized access. |

| Link Analysis | Examines connections between accounts, IPs, and devices for suspicious patterns. |

| Rule-Based Alerts | Predefined rules trigger alerts for high-risk activities (e.g., large transfers). |

| Customer Verification | Uses OTPs, biometric authentication, or callbacks to confirm transaction legitimacy. |

| Collaboration with Networks | Shares fraud data with payment networks (e.g., Visa, Mastercard) for broader detection. |

| Dark Web Monitoring | Scans dark web marketplaces for stolen card details linked to customer accounts. |

| Fraud Scoring Systems | Assigns risk scores to transactions based on multiple factors; high scores trigger reviews. |

| Manual Review Teams | Human analysts investigate flagged transactions for accuracy before blocking or approving. |

| Regulatory Compliance | Adheres to standards like PCI DSS and GDPR to ensure secure fraud detection practices. |

| Customer Reporting | Encourages customers to report suspicious activity via apps, SMS, or helplines. |

| Real-Time Blocking | Automatically freezes transactions or cards upon confirmed fraud detection. |

| Post-Fraud Analysis | Studies fraud cases to refine detection models and prevent future occurrences. |

Explore related products

What You'll Learn

- Monitoring Transaction Patterns: Analyzing spending habits to detect unusual or inconsistent activities

- Real-Time Alerts: Using automated systems to flag suspicious transactions instantly

- AI and Machine Learning: Employing algorithms to identify anomalies and predict fraud risks

- Customer Verification: Requiring additional authentication for high-risk or unusual transactions

- Fraud Detection Teams: Specialized teams investigating flagged transactions and customer reports

![]()

Monitoring Transaction Patterns: Analyzing spending habits to detect unusual or inconsistent activities

Banks employ sophisticated systems to monitor transaction patterns as a critical line of defense against fraudulent charges. By analyzing a customer’s spending habits, banks establish a baseline of normal behavior, which includes typical purchase amounts, frequencies, locations, and types of merchants. This baseline is created using historical transaction data and is continuously updated to reflect changes in the customer’s lifestyle or financial behavior. Any deviation from this established pattern triggers alerts for further investigation, allowing banks to proactively identify potential fraud before significant damage occurs.

To effectively monitor transaction patterns, banks utilize advanced algorithms and machine learning models. These tools analyze vast amounts of data in real time, identifying anomalies such as unusually large purchases, transactions in unfamiliar locations, or multiple charges within a short timeframe. For example, if a customer who typically shops locally suddenly makes a high-value purchase in a foreign country, the system flags this activity as inconsistent with their usual behavior. The algorithms are designed to adapt to individual spending habits, ensuring that legitimate transactions are not mistakenly flagged while fraudulent ones are caught.

Geolocation and time-based analysis are also integral to monitoring transaction patterns. Banks track the geographic locations of transactions and compare them to the customer’s known travel patterns or residence. A transaction occurring in a city where the customer has no known ties, especially if it happens shortly after a purchase in their home city, raises red flags. Similarly, time-based anomalies, such as late-night purchases in a category the customer rarely uses, are scrutinized. This multi-dimensional approach ensures that inconsistencies in both location and timing are detected.

Merchant category analysis is another key aspect of monitoring transaction patterns. Banks categorize merchants based on their industry (e.g., groceries, travel, entertainment) and compare new transactions to the customer’s historical spending in those categories. If a customer who rarely dines out suddenly makes multiple high-value restaurant purchases in a single day, the system identifies this as unusual. Additionally, banks monitor for transactions with high-risk merchants or those frequently associated with fraud, adding another layer of scrutiny to protect customers.

Finally, banks often combine transaction pattern analysis with customer-specific data, such as income levels and spending capacity, to enhance fraud detection accuracy. For instance, a low-income customer making luxury purchases inconsistent with their financial profile would trigger an alert. This holistic approach ensures that the monitoring system is not only reactive but also predictive, identifying potential fraud before it escalates. By continuously refining their algorithms and incorporating new data sources, banks stay ahead of evolving fraud tactics while minimizing false positives to maintain customer trust.

Understanding Your Borrowing Power: How Banks Assess Your Loan Capacity

You may want to see also

Explore related products

![]()

Real-Time Alerts: Using automated systems to flag suspicious transactions instantly

Banks employ sophisticated automated systems to detect and flag suspicious transactions in real-time, a critical component of their fraud prevention strategies. These systems leverage advanced algorithms, machine learning, and artificial intelligence to analyze transaction patterns and identify anomalies that may indicate fraudulent activity. Real-time alerts are generated instantly when a transaction deviates from a customer’s typical behavior or matches known fraud patterns, allowing banks to take immediate action to protect their customers’ accounts.

The foundation of real-time alert systems lies in the continuous monitoring of transaction data. Every transaction, whether it’s a credit card purchase, ATM withdrawal, or online transfer, is scrutinized against a customer’s historical spending habits, location data, and other relevant factors. For example, if a customer typically makes purchases in their hometown and suddenly a transaction occurs in a foreign country, the system flags this as potentially suspicious. Similarly, unusually large transactions or multiple purchases within a short timeframe can trigger alerts. This instantaneous analysis ensures that fraudulent activity is caught before significant damage occurs.

Machine learning plays a pivotal role in enhancing the accuracy of these systems. By learning from vast datasets of both legitimate and fraudulent transactions, the algorithms become increasingly adept at distinguishing between normal and suspicious behavior. They can detect subtle patterns that might elude human analysts, such as small, recurring unauthorized charges or transactions that mimic a customer’s usual spending but are actually fraudulent. Over time, these systems adapt to new fraud tactics, ensuring ongoing effectiveness in a rapidly evolving threat landscape.

Once a suspicious transaction is flagged, the automated system triggers a real-time alert to both the bank’s fraud monitoring team and the customer. Customers are often notified via text message, email, or push notification, allowing them to confirm whether the transaction is legitimate or fraudulent. Simultaneously, the bank’s team investigates the alert, potentially freezing the account or contacting the customer directly to verify the activity. This dual-notification approach ensures swift action while keeping customers informed and engaged in the security process.

To further refine the system, banks continuously update their fraud detection models with new data and feedback from resolved alerts. False positives—legitimate transactions mistakenly flagged as fraudulent—are analyzed to improve the system’s accuracy. This iterative process ensures that real-time alerts remain both effective and customer-friendly, minimizing disruptions while maximizing fraud prevention. By combining cutting-edge technology with proactive customer communication, banks can stay one step ahead of fraudsters and safeguard their customers’ financial well-being.

Central Banks' Role: Shaping Economic Growth and Stability

You may want to see also

Explore related products

![]()

AI and Machine Learning: Employing algorithms to identify anomalies and predict fraud risks

Banks are increasingly leveraging AI and Machine Learning (ML) to combat fraudulent charges by employing sophisticated algorithms that identify anomalies and predict fraud risks in real time. These technologies analyze vast datasets, including transaction histories, user behavior patterns, and external threat intelligence, to detect deviations from normal activity. For instance, if a customer typically makes purchases in their home city but suddenly has a transaction in a foreign country, the system flags this as a potential anomaly. ML models, trained on historical fraud data, continuously learn and adapt to new fraud schemes, ensuring that detection mechanisms remain effective against evolving threats.

One of the key advantages of AI and ML is their ability to process and interpret data at scale and speed unattainable by humans. Traditional rule-based systems rely on predefined thresholds and patterns, which can be easily circumvented by sophisticated fraudsters. In contrast, AI-driven systems use unsupervised learning to identify unusual patterns without explicit instructions, while supervised learning models classify transactions based on labeled datasets of fraudulent and legitimate activities. This dual approach enables banks to detect both known fraud patterns and novel schemes, reducing false positives and improving accuracy.

Behavioral analytics is another critical application of AI in fraud detection. By creating a baseline of a customer’s typical behavior—such as spending habits, transaction times, and device usage—ML algorithms can flag activities that deviate significantly from this norm. For example, if a user who usually shops online suddenly makes a high-value in-store purchase at an unusual hour, the system can trigger an alert or temporarily block the transaction for verification. This proactive approach minimizes financial losses and enhances customer trust.

Predictive analytics powered by AI also plays a vital role in assessing fraud risks before they materialize. By analyzing trends and correlations across multiple data points, ML models can forecast potential vulnerabilities in the banking system or identify customers at higher risk of fraud. For instance, if a particular region experiences a surge in phishing attacks, the system can proactively monitor accounts associated with that area. Additionally, natural language processing (NLP) can analyze unstructured data like customer complaints or social media posts to detect early signs of emerging fraud trends.

To maximize the effectiveness of AI and ML in fraud detection, banks must ensure their models are trained on diverse, high-quality data and regularly updated to reflect new fraud tactics. Collaboration with industry partners and regulatory bodies is essential to share threat intelligence and improve collective defenses. Moreover, transparency and explainability in AI decision-making are critical to maintaining customer trust and complying with regulatory requirements. By integrating AI and ML into their fraud detection frameworks, banks can stay one step ahead of fraudsters and safeguard their customers’ financial assets.

Tyra Banks' Weight Gain: How Much is a Lot?

You may want to see also

Explore related products

![]()

Customer Verification: Requiring additional authentication for high-risk or unusual transactions

Banks employ sophisticated systems to detect and prevent fraudulent charges, and one of the critical layers in this defense mechanism is Customer Verification, particularly for high-risk or unusual transactions. When a transaction deviates from a customer’s typical spending patterns—such as a large purchase in a foreign country or an unusual merchant category—banks flag it as potentially fraudulent. At this point, the system triggers additional authentication steps to verify the customer’s identity before approving the transaction. This process ensures that even if a fraudster gains access to account details, they cannot complete the transaction without the legitimate account holder’s involvement.

The most common method of additional authentication is two-factor authentication (2FA), where the bank requires the customer to provide a second form of verification beyond their card details. This could be a one-time password (OTP) sent via SMS or email, a biometric identifier like a fingerprint or facial recognition, or a response to a security question. For example, if a customer attempts to make a high-value online purchase from an unfamiliar device, the bank may send an OTP to their registered mobile number. The transaction will only proceed if the customer correctly inputs this code, confirming their identity.

In some cases, banks use behavioral biometrics to assess the legitimacy of a transaction. This involves analyzing patterns such as typing speed, device usage, and location data to determine if the transaction aligns with the customer’s usual behavior. If discrepancies are detected, the bank may require further verification, such as a phone call to the customer’s registered number or a visit to a branch for in-person verification. This multi-layered approach ensures that fraudulent transactions are halted even if initial security measures are bypassed.

Another effective method is velocity checks, which monitor the frequency and volume of transactions within a specific timeframe. For instance, if multiple high-value transactions occur within minutes, the bank flags this as suspicious and initiates customer verification. Similarly, geolocation checks compare the transaction location with the customer’s known whereabouts. If a purchase is made in a city where the customer has no recent travel history, the bank may block the transaction and request verification before reprocessing it.

Banks also leverage machine learning algorithms to continuously refine their verification processes. These algorithms analyze vast datasets to identify emerging fraud patterns and adapt authentication requirements accordingly. For example, if a particular type of transaction is increasingly associated with fraud, the bank may automatically require additional verification for all similar transactions. This proactive approach minimizes the risk of fraudulent charges while maintaining a seamless experience for legitimate customers.

Ultimately, Customer Verification for high-risk or unusual transactions is a cornerstone of fraud prevention in banking. By requiring additional authentication, banks create a robust barrier against unauthorized access, ensuring that customers’ funds and personal information remain secure. This process not only protects individual account holders but also safeguards the integrity of the entire financial system.

Does the Fed Buy Bonds from Banks? Understanding Open Market Operations

You may want to see also

Explore related products

$37.99 $39.99

![]()

Fraud Detection Teams: Specialized teams investigating flagged transactions and customer reports

Banks employ sophisticated mechanisms to detect and prevent fraudulent activities, and one of the critical components in this process is the Fraud Detection Team. These specialized teams play a pivotal role in safeguarding customer accounts and the bank's integrity by meticulously investigating flagged transactions and customer reports. When a potentially fraudulent transaction is identified through automated systems or reported by a customer, it is immediately escalated to these experts for further scrutiny. The team's primary objective is to determine the legitimacy of the transaction, protect the customer's funds, and mitigate any potential financial loss.

Fraud Detection Teams are typically composed of highly trained professionals with expertise in financial crime, data analysis, and investigative techniques. They utilize advanced tools and technologies, such as machine learning algorithms and transaction monitoring systems, to analyze patterns and anomalies in account activity. When a transaction is flagged, the team reviews it against established risk criteria, including the transaction amount, location, frequency, and historical account behavior. For instance, a large purchase in a foreign country by a customer who rarely travels would raise red flags and prompt a detailed investigation.

Customer reports are another vital source of information for these teams. When a customer notices unauthorized activity on their account, they can report it directly to the bank. The Fraud Detection Team then takes immediate action by freezing the account to prevent further unauthorized transactions and initiating a thorough investigation. This process often involves contacting the customer to verify the disputed transactions and gathering additional details to assess the situation accurately. The team may also collaborate with law enforcement agencies if the fraud involves criminal activity.

The investigation process is both systematic and time-sensitive. Team members scrutinize transaction details, review account history, and may even analyze IP addresses or device information associated with online transactions. They also cross-reference data with known fraud patterns and databases of compromised cards or accounts. Once the investigation is complete, the team makes a determination: if the transaction is confirmed as fraudulent, the bank reverses the charges, credits the customer's account, and takes steps to secure it further, such as issuing a new card. If the transaction is legitimate, the team communicates this to the customer and lifts any temporary holds on the account.

Continuous improvement is a key aspect of Fraud Detection Teams' operations. They regularly update their knowledge of emerging fraud schemes and adapt their strategies accordingly. Additionally, these teams contribute to refining the bank's fraud detection algorithms by providing feedback on false positives and negatives, ensuring the system becomes more accurate over time. Through their expertise and vigilance, Fraud Detection Teams are indispensable in maintaining the security and trustworthiness of banking systems, protecting both customers and financial institutions from the ever-evolving threat of fraud.

Does Berkeley Mechanics Bank Exchange Iraqi Dinars? Facts and Insights

You may want to see also

Frequently asked questions

Banks use advanced fraud detection systems that monitor transaction patterns, location, and spending behavior. Unusual activity, such as large purchases in unfamiliar locations, triggers alerts for further investigation.

AI analyzes vast amounts of transaction data in real-time to identify anomalies and patterns associated with fraud. It continuously learns from new data to improve detection accuracy.

Banks may cross-reference transaction details with historical spending patterns, contact the account holder for confirmation, or use additional security measures like two-factor authentication.

The bank typically freezes the transaction, notifies the account holder, and may temporarily block the card. The holder is asked to confirm if the charge is unauthorized.

Yes, banks monitor online transactions using secure networks and collaborate with merchants and payment processors to trace the source of fraudulent activity, even if the card isn’t physically present.