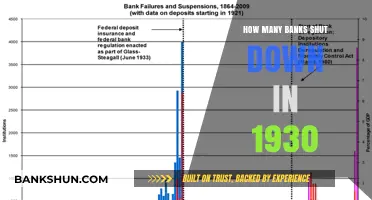

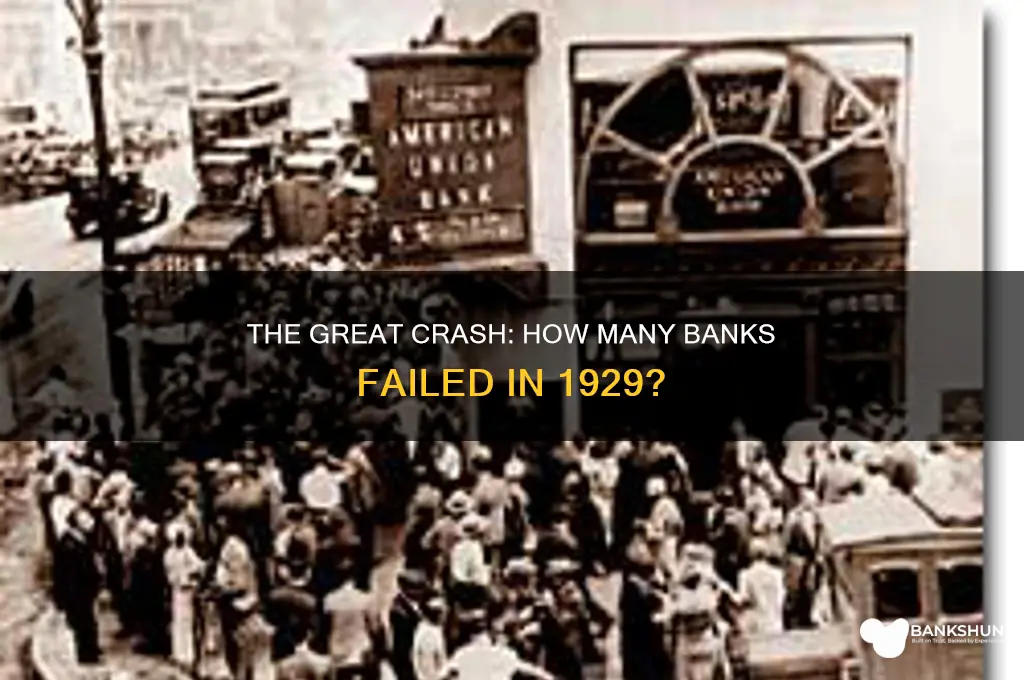

The year 1929 marked a pivotal moment in financial history, as the Great Depression began with the catastrophic stock market crash in October. This economic downturn had a profound impact on the banking sector, leading to widespread bank failures across the United States. By the end of 1929, over 600 banks had closed their doors, leaving countless Americans without access to their savings and contributing to a deepening sense of financial insecurity. This wave of bank failures was a stark indicator of the broader economic collapse that would define the 1930s, highlighting the fragility of the financial system during this tumultuous period.

Explore related products

What You'll Learn

- Bank Failures in 1929: Number of banks that collapsed during the Great Depression

- Causes of Bank Failures: Economic factors leading to widespread bank closures in 1929

- Regional Impact: Geographic distribution of bank failures across the United States

- Depositors' Losses: Effects of bank collapses on individual and business savings

- Government Response: Measures taken to address bank failures during the crisis

![]()

Bank Failures in 1929: Number of banks that collapsed during the Great Depression

The year 1929 marked the beginning of one of the most severe economic downturns in history, known as the Great Depression. A critical aspect of this crisis was the widespread failure of banks across the United States. While the exact number of bank failures in 1929 alone is often debated, records indicate that approximately 659 banks collapsed during that year. This figure, though significant, was just the initial wave of a much larger trend of bank failures that would continue throughout the 1930s. The fragility of the banking system, coupled with panic among depositors, created a domino effect that exacerbated the economic collapse.

The root causes of these bank failures were multifaceted. The 1920s had seen rapid speculation in the stock market, and many banks had invested heavily in risky assets. When the stock market crashed in October 1929, these investments lost value, leaving banks with insufficient capital to meet withdrawal demands. Additionally, the lack of deposit insurance meant that depositors rushed to withdraw their funds, triggering bank runs. This loss of confidence in the banking system led to a liquidity crisis, forcing many banks to close their doors permanently.

The impact of these bank failures was profound and far-reaching. As banks collapsed, millions of Americans lost their savings, further eroding consumer confidence and spending. Businesses, unable to secure loans, were forced to lay off workers or shut down entirely, contributing to the skyrocketing unemployment rate. The banking crisis also highlighted the inadequacies of the financial regulatory framework at the time, which lacked mechanisms to stabilize failing institutions or protect depositors.

By the end of 1929, the 659 bank failures represented a stark warning of the deeper troubles ahead. The following years would see even more dramatic numbers, with over 9,000 banks closing by 1933. This period underscored the need for systemic reforms, leading to the establishment of key institutions like the Federal Deposit Insurance Corporation (FDIC) in 1933, which aimed to restore trust in the banking system and prevent future collapses.

In conclusion, the bank failures of 1929 were a pivotal moment in the Great Depression, signaling the beginning of a decade-long struggle for economic stability. The 659 banks that collapsed that year were not just numbers but represented the loss of livelihoods, savings, and trust in the financial system. Understanding this period provides valuable insights into the importance of robust financial regulations and the role of government intervention in preventing economic catastrophes.

How Long Do Banks Retain Default Records? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Causes of Bank Failures: Economic factors leading to widespread bank closures in 1929

The year 1929 marked a pivotal moment in American financial history, characterized by widespread bank failures that exacerbated the Great Depression. One of the primary economic factors leading to these closures was the speculative stock market bubble. Throughout the 1920s, investors poured money into the stock market, often using margin loans from banks to finance their purchases. By late 1929, stock prices had reached unsustainable levels, detached from underlying economic fundamentals. When the market crashed in October, investors were unable to repay their loans, leading to significant losses for banks. This erosion of bank capital left many institutions insolvent, triggering a wave of failures.

Another critical factor was the agricultural crisis that preceded the stock market crash. Throughout the 1920s, farmers faced declining crop prices due to overproduction and reduced demand, both domestically and internationally. This led to widespread defaults on agricultural loans, as farmers were unable to generate sufficient income to repay their debts. Rural banks, heavily dependent on farm loans, were particularly vulnerable. As defaults mounted, these banks saw their asset quality deteriorate, ultimately leading to closures. The agricultural downturn thus created a ripple effect, weakening the financial system even before the stock market collapse.

The lack of deposit insurance also played a significant role in the widespread bank failures of 1929. At the time, depositors had no guarantee that their funds would be protected if a bank failed. This absence of safety nets led to panic withdrawals, or "bank runs," as depositors rushed to withdraw their money out of fear of losing it. Bank runs depleted reserves rapidly, forcing many solvent but liquidity-constrained banks to close their doors. The contagion effect of these runs further destabilized the banking system, turning localized failures into a national crisis.

Additionally, the overreliance on a single economic sector contributed to the fragility of many banks. During the 1920s, banks heavily concentrated their lending in sectors like agriculture, real estate, and stocks, which were all vulnerable to economic downturns. When these sectors collapsed, banks faced massive loan defaults and asset devaluations. This lack of diversification left banks with insufficient buffers to absorb losses, accelerating their failures. The interconnectedness of these sectors meant that distress in one area quickly spread to others, amplifying the crisis.

Lastly, monetary policy decisions by the Federal Reserve played a role in the economic conditions leading to bank failures. In the years leading up to 1929, the Fed maintained low interest rates, which fueled speculation and borrowing but failed to address underlying economic imbalances. When the Fed tightened monetary policy in 1928 and 1929 to curb speculation, it inadvertently restricted credit availability and slowed economic activity. This contraction reduced borrowers' ability to repay loans, further straining banks' balance sheets. The Fed's delayed response to the ensuing crisis also limited its ability to stabilize the banking system, allowing failures to proliferate.

In summary, the widespread bank closures in 1929 were the result of a combination of economic factors, including speculative excesses, agricultural distress, lack of deposit insurance, sectoral concentration, and monetary policy missteps. These factors collectively undermined the stability of the banking system, turning what could have been a localized crisis into a national catastrophe. Understanding these causes provides critical insights into the vulnerabilities of financial systems and the importance of regulatory safeguards to prevent similar collapses in the future.

Avoid Bank Fees: Strategies for Smart Banking and Financial Freedom

You may want to see also

Explore related products

![]()

Regional Impact: Geographic distribution of bank failures across the United States

The Great Depression, triggered by the stock market crash of 1929, had a profound and uneven impact on the banking sector across the United States. The geographic distribution of bank failures reveals significant regional disparities, reflecting the varying economic vulnerabilities and dependencies of different areas. While the crisis was nationwide, certain regions were disproportionately affected due to their reliance on specific industries, agricultural conditions, and local economic structures. Understanding this regional impact provides critical insights into the depth and breadth of the financial collapse during this period.

The Midwest and Great Plains regions, often referred to as the "Dust Bowl" states, experienced some of the most severe banking crises. States like Iowa, Kansas, and Oklahoma saw a high concentration of bank failures due to a combination of agricultural distress and economic downturn. Farmers in these areas were already struggling with drought and falling crop prices, which led to widespread defaults on loans. As agricultural communities collapsed, local banks that had heavily invested in farm mortgages were unable to recover, resulting in a wave of closures. By 1933, over 5,000 banks had failed in these regions alone, leaving many communities without access to financial services and exacerbating the economic hardship.

In contrast, the Northeast and Mid-Atlantic states, which were more industrialized, experienced a different pattern of bank failures. Cities like New York, Philadelphia, and Boston had banks that were heavily exposed to stock market investments and industrial loans. When the stock market crashed in 1929, these banks faced significant liquidity issues as investors withdrew funds en masse. However, the impact was somewhat mitigated by the diversification of their economies and the presence of larger, more established financial institutions. Still, the region saw a notable number of bank failures, particularly among smaller banks that lacked the resources to weather the crisis.

The South, already economically disadvantaged before the Depression, was hit particularly hard by bank failures. States like Mississippi, Alabama, and South Carolina had banking systems that were fragile due to widespread poverty and limited industrial development. The collapse of cotton prices and the decline in agricultural revenues further weakened these banks, leading to a high failure rate. Additionally, racial and economic inequalities in the South meant that African American communities were disproportionately affected, as they often relied on smaller, local banks that were more susceptible to failure.

The West Coast, while not as severely impacted as the Midwest or South, still experienced significant banking distress. California, in particular, saw a notable number of bank failures due to its reliance on real estate and speculative investments. The collapse of the housing market and the decline in construction activity left many banks exposed. However, the region's relatively diversified economy, including emerging industries like entertainment and agriculture, helped prevent an even greater number of failures. Despite this, the loss of banks in key urban centers like Los Angeles and San Francisco had long-lasting effects on local economies.

In summary, the geographic distribution of bank failures in 1929 and the subsequent years of the Great Depression highlights the regional economic vulnerabilities of the United States. The Midwest and Great Plains suffered the most due to agricultural collapse, while the Northeast faced challenges tied to industrialization and stock market exposure. The South's fragile banking system and the West Coast's reliance on speculative investments also contributed to significant failures. This regional impact underscores the complex interplay between local economies and the broader financial crisis, shaping the recovery efforts and policy responses of the era.

Does Republic Bank Offer Overdraft Protection? What You Need to Know

You may want to see also

Explore related products

![]()

Depositors' Losses: Effects of bank collapses on individual and business savings

The collapse of banks during the 1929 financial crisis had devastating effects on depositors, both individuals and businesses, leading to significant losses in savings. Historical records indicate that over 9,000 banks failed between 1929 and 1933, a period marked by the Great Depression. These bank failures eroded public confidence in the financial system and resulted in the loss of billions of dollars in deposits. Many depositors found themselves unable to access their savings, as banks closed their doors, leaving account holders with little to no recourse. The absence of federal deposit insurance prior to the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 meant that depositors bore the full brunt of these losses.

Individual depositors were particularly vulnerable to the effects of bank collapses. For many families, bank accounts represented their life savings, intended for emergencies, education, or retirement. When banks failed, these savings were often wiped out overnight, forcing individuals to rely on meager incomes or charitable aid. The psychological impact was profound, as financial security was replaced by uncertainty and fear. Families were compelled to drastically alter their lifestyles, postponing major purchases, reducing consumption, and, in extreme cases, facing homelessness or hunger. The loss of savings also stifled economic mobility, as individuals lacked the capital to invest in education, start businesses, or improve their living conditions.

Businesses, too, suffered immense losses due to bank collapses. Companies relied on bank deposits to manage cash flow, pay employees, and fund operations. When banks failed, businesses lost access to their working capital, leading to widespread layoffs, reduced production, and, in many cases, bankruptcy. Small and medium-sized enterprises were especially hard-hit, as they often lacked the financial reserves or access to alternative credit sources to weather the crisis. The ripple effects of these business failures further exacerbated the economic downturn, as suppliers, customers, and entire communities felt the impact of reduced economic activity.

The losses incurred by depositors also had broader macroeconomic consequences. As individuals and businesses lost their savings, consumer spending and investment plummeted, deepening the Great Depression. The reduction in aggregate demand led to deflation, further depressing economic activity. Additionally, the widespread bank failures highlighted the fragility of the financial system, prompting a wave of regulatory reforms. The establishment of the FDIC in 1933, which provided federal insurance for bank deposits, was a direct response to the depositor losses of the early 1930s, aimed at restoring confidence in the banking system and preventing future crises.

In conclusion, the bank collapses following the 1929 financial crisis resulted in catastrophic losses for depositors, both individual and business. These losses not only devastated personal finances and business operations but also contributed to the severity and duration of the Great Depression. The absence of deposit insurance during this period underscored the need for systemic safeguards to protect savers. The lessons learned from this era led to significant financial reforms, shaping the modern banking system and its focus on depositor protection. Understanding these historical effects is crucial for appreciating the importance of financial stability and the role of regulatory measures in safeguarding savings.

Does Merrick Bank Offer a Rewards Program? Find Out Here

You may want to see also

Explore related products

![]()

Government Response: Measures taken to address bank failures during the crisis

The 1929 stock market crash precipitated a severe banking crisis, with thousands of banks failing across the United States. By 1933, over 9,000 banks had closed, wiping out billions in assets and eroding public confidence in the financial system. The government response to these bank failures was initially fragmented but eventually evolved into a series of comprehensive measures aimed at stabilizing the banking sector and restoring trust. The Hoover administration, in office during the early years of the crisis, took limited steps, such as encouraging voluntary bank mergers and providing loans through the Reconstruction Finance Corporation (RFC). However, these efforts were insufficient to stem the tide of bank failures, as the economic downturn deepened and depositors continued to withdraw funds en masse.

One of the most significant government responses came with the inauguration of President Franklin D. Roosevelt in 1933. His administration acted swiftly to address the banking crisis, beginning with the declaration of a nationwide "bank holiday" in March 1933. This temporary closure of all banks allowed time to assess their solvency and prevented further panic-driven withdrawals. During this period, Congress passed the Emergency Banking Act, which provided a framework for reopening banks after federal inspectors deemed them financially sound. This measure was critical in restoring public confidence, as only stable banks were permitted to resume operations, while insolvent institutions were either liquidated or reorganized.

Another pivotal measure was the establishment of the Federal Deposit Insurance Corporation (FDIC) under the Glass-Steagall Act of 1933. The FDIC insured bank deposits up to $5,000 (later increased), providing a safety net for depositors and reducing the likelihood of bank runs. This insurance program was a cornerstone of the government’s effort to stabilize the banking system, as it assured the public that their savings were secure even if a bank failed. The FDIC’s creation marked a fundamental shift in the government’s role in banking, from a hands-off approach to active oversight and protection of depositors.

In addition to deposit insurance, the government implemented regulatory reforms to prevent future bank failures. The Glass-Steagall Act also separated commercial and investment banking activities, reducing risky speculation by banks. The Federal Reserve was given greater authority to oversee banks and manage the money supply, ensuring more stability in the financial system. These regulatory changes aimed to address the root causes of bank failures, such as excessive risk-taking and inadequate capital reserves, by imposing stricter standards and accountability on financial institutions.

Finally, the government provided direct financial support to struggling banks through the Reconstruction Finance Corporation (RFC), which was expanded under Roosevelt. The RFC offered loans to banks, railroads, and other businesses, helping to recapitalize institutions and prevent further collapses. While the RFC’s effectiveness was debated, it played a crucial role in providing liquidity to the banking system during a time of severe credit contraction. Together, these measures—the bank holiday, deposit insurance, regulatory reforms, and financial assistance—formed a multifaceted government response that gradually restored stability to the banking sector and laid the foundation for long-term financial security.

Is Cash App a Bank? Understanding Its Financial Role and Limits

You may want to see also

Frequently asked questions

Over 650 banks failed in the United States in 1929 alone, marking the beginning of a wave of bank failures during the Great Depression.

Approximately 5% of all banks in the U.S. closed in 1929, with the number of failures increasing significantly in subsequent years.

No, while the U.S. experienced the most significant number of bank failures in 1929, the financial crisis also impacted banks in Europe and other parts of the world.

Bank failures eroded public confidence in the financial system, leading to widespread panic, reduced lending, and a contraction in economic activity, which deepened the Great Depression.

The Federal Reserve took limited action in 1929, focusing on stabilizing the stock market rather than directly addressing bank failures, which critics argue exacerbated the crisis.