The United States financial landscape is not solely dominated by traditional banks; it also encompasses a significant number of non-bank financial institutions that play a crucial role in the economy. These non-banks, which include credit unions, fintech companies, payday lenders, and other alternative financial service providers, offer a wide range of products and services that cater to diverse consumer needs. Understanding the number and impact of these non-banks is essential for grasping the full scope of the U.S. financial system, as they often fill gaps left by traditional banking institutions, particularly in underserved communities. While exact figures can vary due to differing definitions and regulatory classifications, estimates suggest there are thousands of non-bank entities operating across the country, contributing to a more inclusive and competitive financial environment.

Explore related products

$129.76 $199.99

$104.57 $129.99

What You'll Learn

![]()

Non-bank financial institutions definition

Non-bank financial institutions (NBFIs) are a critical component of the financial ecosystem, offering a wide range of services that complement those provided by traditional banks. By definition, NBFIs are organizations that offer financial services but do not hold a full banking license, meaning they cannot accept deposits from the general public in the same way banks do. Instead, they specialize in areas such as lending, investment management, insurance, and asset financing. Examples of NBFIs include credit unions, payday lenders, mortgage companies, investment funds, and leasing companies. These institutions play a vital role in expanding access to financial services, particularly for individuals and businesses that may not qualify for traditional bank offerings.

The definition of NBFIs is broad and encompasses entities that operate in various sectors of the financial market. For instance, credit unions are member-owned financial cooperatives that provide banking services to their members, while payday lenders offer short-term, high-interest loans to individuals. Investment funds, such as mutual funds and hedge funds, pool money from multiple investors to invest in securities, real estate, or other assets. Insurance companies, another type of NBFI, provide risk management solutions by offering policies that protect against financial losses. Each of these institutions operates under specific regulatory frameworks that differ from those governing traditional banks, reflecting their unique roles and risk profiles.

In the United States, the number of non-bank financial institutions is substantial, though exact figures vary depending on the source and the specific types of institutions included in the count. According to industry reports and regulatory data, there are tens of thousands of NBFIs operating across the country. For example, the credit union sector alone includes over 5,000 institutions, while the mortgage lending industry comprises thousands of independent companies. Additionally, the investment management sector is vast, with thousands of registered investment advisors and fund managers. The diversity and scale of NBFIs highlight their importance in providing financial services tailored to specific needs and market segments.

The rise of NBFIs in the U.S. can be attributed to several factors, including regulatory flexibility, technological innovation, and the evolving demands of consumers and businesses. Unlike banks, which are subject to stringent capital requirements and oversight by agencies like the Federal Reserve, NBFIs often face less regulatory scrutiny, allowing them to innovate and adapt more quickly. However, this flexibility also comes with risks, as some NBFIs operate in less regulated areas, such as payday lending or certain types of investment funds, which can lead to consumer protection concerns. As a result, policymakers and regulators continually work to balance innovation with oversight to ensure the stability and fairness of the financial system.

Understanding the definition and role of non-bank financial institutions is essential for grasping the full scope of the U.S. financial landscape. While the exact number of NBFIs is difficult to pinpoint due to their diverse nature and the dynamic market environment, their collective impact is undeniable. These institutions bridge gaps in financial access, provide specialized services, and foster competition, ultimately contributing to a more inclusive and efficient financial system. As the financial industry continues to evolve, NBFIs will likely remain a key area of focus for both market participants and regulators alike.

Bank Asset Insurance: What Protection Do Banks Have?

You may want to see also

Explore related products

$135.43 $169.99

![]()

Types of non-bank lenders in the U.S

The U.S. financial landscape is diverse, with a significant number of non-bank lenders operating alongside traditional banks. While the exact number of non-bank lenders in the U.S. is not definitively pinned down due to the dynamic nature of the industry, estimates suggest there are thousands of such entities. These non-bank lenders play a crucial role in providing credit and financial services to consumers and businesses that may not meet the stringent requirements of traditional banks. Below, we explore the various types of non-bank lenders in the U.S., each serving distinct market needs.

Online Lenders are among the most prominent types of non-bank lenders in the U.S. These entities operate primarily through digital platforms, offering a range of financial products, including personal loans, business loans, and lines of credit. Online lenders are known for their streamlined application processes, quick approval times, and use of alternative data to assess creditworthiness. Companies like LendingClub, SoFi, and Prosper are examples of online lenders that have gained significant traction. Their ability to leverage technology allows them to reach a broader audience, including individuals with non-traditional credit histories.

Credit Unions are another important category of non-bank lenders. While credit unions are member-owned financial cooperatives, they are not classified as banks. They offer many of the same services as banks, including loans, savings accounts, and credit cards, but often with more favorable terms for their members. Credit unions are typically community-based or affiliated with specific employers, organizations, or industries. Their focus on member service rather than profit maximization allows them to offer lower interest rates on loans and higher rates on deposits compared to traditional banks.

Payday Lenders cater to a different segment of the market, providing short-term, high-interest loans to individuals who need quick access to cash. These loans are typically due on the borrower's next payday, hence the name. While payday lenders provide a valuable service for those in immediate financial need, they have been criticized for their high fees and interest rates, which can lead to cycles of debt for vulnerable borrowers. Despite this, payday lenders remain a significant part of the non-bank lending landscape, with thousands of storefronts and online platforms across the U.S.

Peer-to-Peer (P2P) Lending Platforms represent a more recent innovation in non-bank lending. These platforms connect individual borrowers directly with individual lenders or investors, bypassing traditional financial institutions. P2P lending platforms use technology to facilitate transactions, assess risk, and determine interest rates. Borrowers can access loans for various purposes, including debt consolidation, home improvement, and business funding. Investors, on the other hand, can earn returns by funding these loans. Examples of P2P lending platforms include LendingClub and Prosper, which have popularized this model in the U.S.

Specialty Finance Companies focus on specific niches within the lending market, such as equipment financing, invoice financing, and merchant cash advances. These companies provide tailored financial solutions to businesses that may not qualify for traditional bank loans. For instance, equipment finance companies offer loans or leases to businesses looking to purchase machinery, vehicles, or other equipment. Invoice financing companies provide advances based on outstanding invoices, helping businesses improve their cash flow. Merchant cash advance providers offer funding in exchange for a percentage of future credit card sales, catering to small businesses with fluctuating revenue streams.

In conclusion, the U.S. non-bank lending sector is characterized by its diversity and adaptability, with various types of lenders meeting the needs of different consumer and business segments. From online lenders and credit unions to payday lenders, P2P platforms, and specialty finance companies, these entities collectively contribute to a more inclusive and dynamic financial ecosystem. Understanding the types of non-bank lenders available can help individuals and businesses make informed decisions when seeking financial services outside the traditional banking system.

How Banks Finance Third-Party Sales: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Number of fintech companies in the U.S

The fintech industry in the U.S. has experienced explosive growth over the past decade, significantly contributing to the broader category of non-bank financial institutions. While the exact number of fintech companies in the U.S. can vary depending on the definition and scope, estimates suggest there are over 10,000 fintech firms operating across the country as of 2023. These companies span a wide range of sectors, including payments, lending, wealth management, insurance, and blockchain technology. The rise of fintech has been driven by advancements in technology, changing consumer preferences, and the increasing demand for digital financial services.

To put this in perspective, fintech companies represent a substantial portion of the non-bank financial landscape in the U.S. Non-bank entities, which include fintech firms, credit unions, and other financial service providers, are estimated to number over 20,000 in total. Fintech, however, stands out due to its innovation and rapid growth. Major hubs like Silicon Valley, New York, and Chicago have become epicenters for fintech startups, attracting significant venture capital investment. In 2022 alone, U.S. fintech companies raised over $30 billion in funding, highlighting the sector's dynamism and potential.

The diversity within the fintech sector is another key factor in understanding its scale. For instance, payment processing companies like Stripe and Square (Block) have become household names, while lending platforms such as SoFi and LendingClub have disrupted traditional banking models. Additionally, robo-advisors like Betterment and Wealthfront have revolutionized wealth management, and insurtech firms like Lemonade have transformed the insurance industry. This specialization has allowed fintech companies to address specific pain points in the financial ecosystem, further driving their proliferation.

Regulatory considerations also play a role in the growth of fintech companies in the U.S. Unlike traditional banks, fintech firms often operate under different regulatory frameworks, which can both enable innovation and present challenges. The Office of the Comptroller of the Currency (OCC) and the Consumer Financial Protection Bureau (CFPB) are among the key regulators overseeing fintech activities. Despite regulatory complexities, the U.S. remains a global leader in fintech innovation, with its companies accounting for a significant share of the $150 billion global fintech market.

In conclusion, the number of fintech companies in the U.S. is a testament to the country's leadership in financial innovation. With over 10,000 fintech firms operating across various sectors, the U.S. fintech ecosystem is a critical component of the broader non-bank financial landscape. As technology continues to evolve and consumer demand for digital financial services grows, the number of fintech companies is expected to rise further, solidifying their role in shaping the future of finance.

Citizens Bank's Customer Base: A Large Number of People

You may want to see also

Explore related products

![]()

Non-bank mortgage lenders statistics

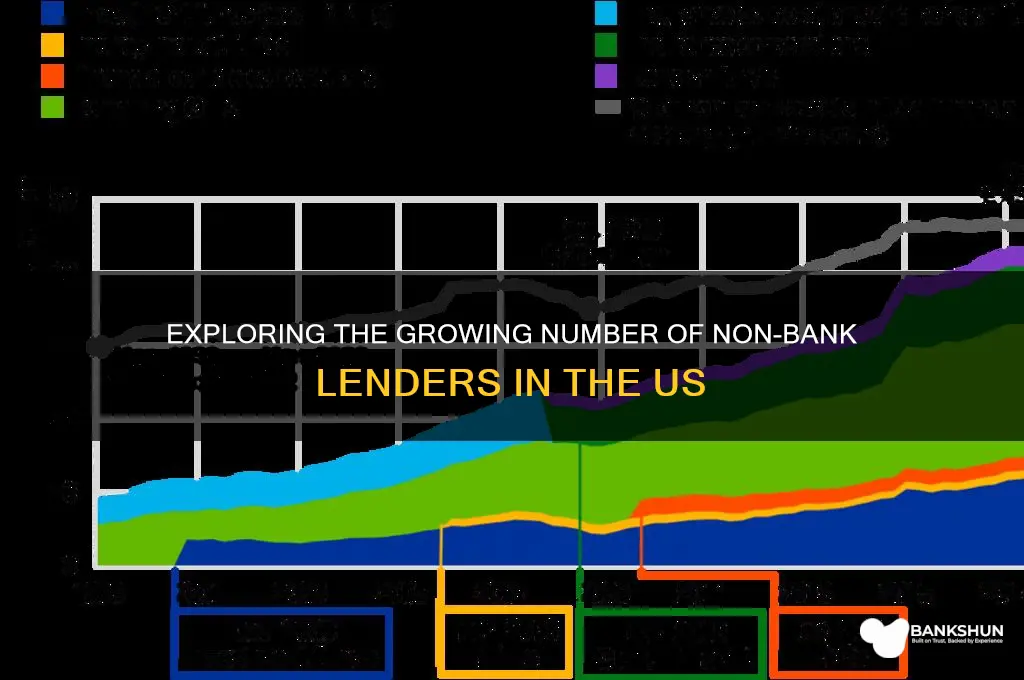

The non-bank mortgage lending sector in the United States has experienced significant growth over the past decade, reshaping the landscape of home financing. As of recent data, there are approximately 3,000 to 4,000 non-bank mortgage lenders operating in the U.S., though the exact number fluctuates due to market entry and exit dynamics. These entities, which include independent mortgage companies, online lenders, and specialty finance firms, now originate a substantial portion of residential mortgages. According to the Urban Institute, non-bank lenders accounted for over 60% of mortgage originations in 2022, up from just 10% in 2009. This shift reflects their increasing dominance in the market, often attributed to their agility, technological innovation, and ability to cater to niche borrower segments.

One of the most striking statistics is the volume of loans originated by non-bank lenders. In 2022, non-banks originated over $2 trillion in mortgage loans, a figure that underscores their critical role in the housing finance ecosystem. This growth has been fueled by their focus on digital platforms, streamlined application processes, and competitive rates, which appeal to tech-savvy borrowers. However, their rise has also raised regulatory concerns, as non-banks are not subject to the same capital requirements as traditional banks, potentially posing risks during economic downturns.

Geographically, non-bank mortgage lenders are concentrated in states with high housing demand and robust real estate markets. California, Texas, Florida, and New York are among the top states with the highest number of non-bank lenders, given their large populations and active housing markets. Smaller lenders often specialize in local markets, offering tailored products to meet regional needs. Despite their widespread presence, non-banks face challenges such as rising interest rates, which can reduce refinancing activity, and increasing regulatory scrutiny to ensure consumer protection.

Another key statistic is the market share of non-bank lenders in specific mortgage segments. For example, non-banks dominate the Federal Housing Administration (FHA) and Veterans Affairs (VA) loan markets, originating over 70% of FHA loans and 50% of VA loans in recent years. These government-backed loans are critical for first-time homebuyers and veterans, and non-banks have effectively leveraged their flexibility to serve these demographics. In contrast, traditional banks maintain a stronger presence in conventional, jumbo, and portfolio loan markets, where their established relationships and capital reserves provide a competitive edge.

Finally, the financial performance of non-bank mortgage lenders highlights their resilience and adaptability. Despite operating with thinner capital buffers than banks, many non-banks have reported strong profitability, driven by high origination volumes and efficient cost management. However, their reliance on warehouse lines of credit and secondary market sales exposes them to liquidity risks, particularly during periods of market volatility. As the housing market evolves, monitoring these statistics will be crucial for understanding the role of non-banks in ensuring access to credit and maintaining financial stability.

Ally Bank Application Timeline: What to Expect During the Process

You may want to see also

Explore related products

![]()

Regulation of non-bank financial entities

The regulation of non-bank financial entities (NBFEs) in the United States is a critical aspect of maintaining financial stability and consumer protection. NBFEs encompass a wide range of institutions, including fintech companies, payday lenders, money service businesses, and investment funds, which operate outside the traditional banking sector. As of recent estimates, there are thousands of non-bank financial entities in the U.S., with the exact number varying depending on the specific category and regulatory definitions. This diversity underscores the need for a robust regulatory framework to ensure these entities do not pose systemic risks or exploit consumers.

Regulatory oversight of NBFEs is primarily divided among federal and state authorities, with key agencies including the Consumer Financial Protection Bureau (CFPB), the Securities and Exchange Commission (SEC), the Financial Crimes Enforcement Network (FinCEN), and state regulators. The CFPB, for instance, focuses on consumer protection by enforcing laws against unfair, deceptive, or abusive practices in the financial marketplace. It has increasingly targeted non-bank entities, particularly in areas like debt collection, payday lending, and digital payment services, where consumer vulnerabilities are high. State regulators also play a crucial role, as many NBFEs operate under state-specific licenses, requiring compliance with local laws and regulations.

One of the challenges in regulating NBFEs is the rapid innovation in financial technology (fintech), which often outpaces existing regulatory frameworks. Fintech firms, such as peer-to-peer lenders and cryptocurrency platforms, operate in regulatory gray areas, necessitating adaptive and forward-looking policies. Regulators are increasingly focusing on activity-based regulation rather than entity-based regulation, meaning oversight is applied based on the financial activity performed rather than the type of institution. This approach ensures that similar risks are regulated consistently, regardless of whether they originate from a bank or a non-bank entity.

Another critical area of regulation is anti-money laundering (AML) and counter-terrorism financing (CTF) compliance. FinCEN requires many NBFEs, such as money transmitters and cryptocurrency exchanges, to register, implement AML programs, and report suspicious activities. This regulatory focus is essential given the potential for NBFEs to be exploited for illicit financial flows. Additionally, the SEC and the Commodity Futures Trading Commission (CFTC) oversee investment-related NBFEs, ensuring compliance with securities and derivatives laws to protect investors and market integrity.

Despite these regulatory efforts, gaps remain, particularly in areas like data privacy, cybersecurity, and the oversight of emerging financial products. Policymakers are increasingly calling for comprehensive federal legislation to address these gaps and harmonize regulatory standards across states. Strengthening the regulatory framework for NBFEs is essential not only to protect consumers and investors but also to ensure that innovation in the financial sector contributes positively to economic growth without undermining stability. As the number and complexity of non-bank financial entities continue to grow, so too must the sophistication and adaptability of the regulatory environment.

The Role of Clearing Houses in Banking

You may want to see also

Frequently asked questions

The exact number of non-banks in the US is not centrally tracked, as the term encompasses a wide range of entities, including fintech companies, payday lenders, and other financial service providers not regulated as traditional banks. Estimates suggest there are tens of thousands of such entities operating across the country.

A non-bank is any financial institution or company that provides banking-like services but is not regulated as a traditional bank. Examples include mortgage lenders, credit unions, payday loan providers, and fintech platforms offering loans, payments, or other financial services.

Yes, non-banks are regulated, but the oversight varies by type and activity. Some are regulated by state authorities, while others fall under federal agencies like the Consumer Financial Protection Bureau (CFPB) or the Federal Trade Commission (FTC). However, regulation is generally less stringent than for traditional banks.

Non-banks play a significant role by providing alternative financial services, especially to underserved populations or those who cannot access traditional banking. They often offer faster, more flexible solutions, such as online lending, digital payments, and specialized credit products, contributing to financial inclusion and innovation.