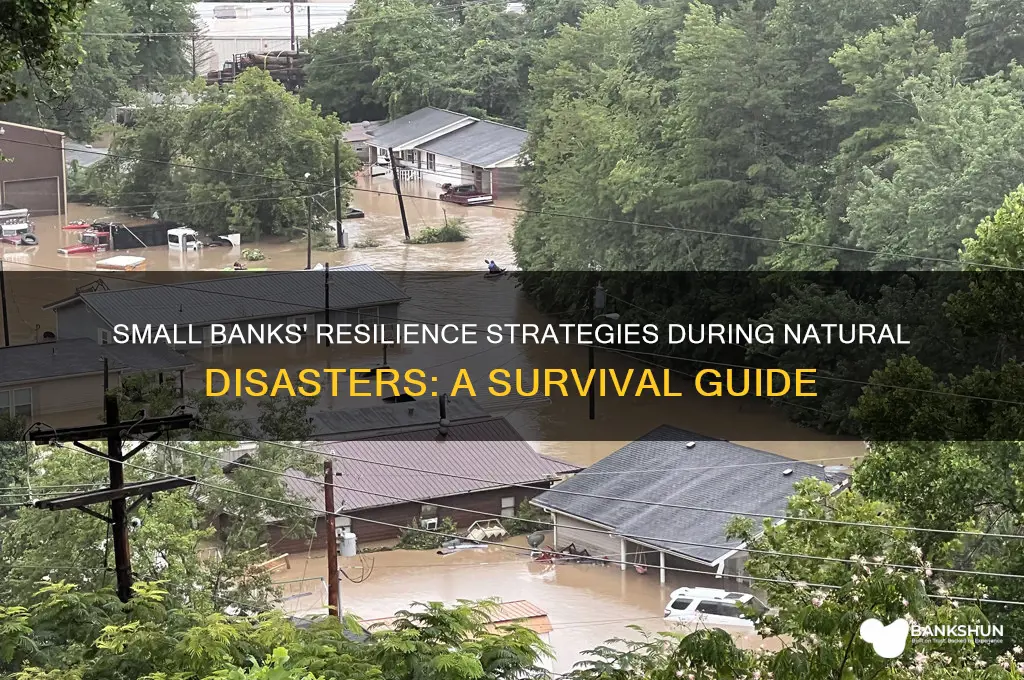

Small banks play a critical role in supporting local communities during natural disasters, often serving as a lifeline for individuals and businesses in affected areas. Unlike larger financial institutions, small banks are deeply rooted in their communities, enabling them to respond swiftly and empathetically to the unique needs of their customers. They frequently offer tailored relief measures, such as payment deferrals, emergency loans, and reduced fees, to help residents and businesses recover. Additionally, their localized decision-making processes allow for quicker approvals and more flexible solutions compared to larger banks. However, small banks also face significant challenges, including limited resources and exposure to localized economic downturns, which can strain their ability to provide sustained support. Despite these hurdles, their community-focused approach often fosters resilience and trust, making them indispensable during times of crisis.

Explore related products

What You'll Learn

- Emergency preparedness planning for small banks in disaster-prone areas

- Post-disaster recovery strategies to restore banking operations quickly

- Leveraging technology for remote banking during natural disasters

- Financial resilience through insurance and risk mitigation measures

- Community support and relief efforts led by small banks

![]()

Emergency preparedness planning for small banks in disaster-prone areas

Small banks in disaster-prone areas face unique challenges when it comes to emergency preparedness, as they must safeguard both their operations and the financial well-being of their customers. Developing a comprehensive emergency preparedness plan is critical to ensuring business continuity, protecting assets, and maintaining customer trust during and after a natural disaster. The first step in this process is conducting a thorough risk assessment to identify potential threats specific to the region, such as hurricanes, floods, wildfires, or earthquakes. Understanding these risks allows banks to tailor their preparedness strategies to address the most likely scenarios, ensuring resources are allocated efficiently.

Once risks are identified, small banks should establish a detailed emergency response plan that outlines clear roles and responsibilities for staff members. This plan should include protocols for securing physical assets, such as cash, important documents, and technology infrastructure, as well as procedures for evacuating personnel and customers if necessary. Regular training and drills are essential to ensure employees are familiar with the plan and can execute it effectively under stress. Additionally, banks should invest in backup power systems, off-site data storage, and redundant communication channels to maintain operations even if the primary facility is compromised.

Customer communication is another critical component of emergency preparedness for small banks. During a disaster, customers rely on their bank for access to funds and financial services, so banks must have a strategy to keep customers informed about branch closures, alternative service options, and steps to protect their accounts. This can include leveraging digital channels like mobile banking apps, social media, and email, as well as establishing partnerships with local media outlets to disseminate information quickly. Proactive communication helps reduce panic and ensures customers know how to access essential services during an emergency.

Collaboration with local authorities, emergency services, and other financial institutions is also vital for small banks in disaster-prone areas. Building relationships with these stakeholders before a disaster strikes can streamline response efforts and provide access to additional resources when needed. For example, banks can work with local law enforcement to ensure the security of their facilities or partner with larger banks to share backup resources like mobile branches or temporary office space. Such partnerships enhance the resilience of the entire community and demonstrate the bank’s commitment to its customers and region.

Finally, small banks must regularly review and update their emergency preparedness plans to reflect changing conditions, such as new regulatory requirements, advancements in technology, or shifts in the local risk landscape. After a disaster, conducting a post-event analysis to identify strengths and weaknesses in the response can provide valuable insights for improving future plans. By adopting a proactive and adaptive approach to emergency preparedness, small banks can minimize the impact of natural disasters, protect their operations, and continue serving their communities effectively.

Are Your Bank CDs Covered by FDIC Insurance?

You may want to see also

Explore related products

![]()

Post-disaster recovery strategies to restore banking operations quickly

In the aftermath of a natural disaster, small banks face unique challenges in restoring their operations swiftly to serve their communities. One critical post-disaster recovery strategy is to activate pre-established emergency response plans. These plans should include clear communication protocols, designated recovery teams, and prioritized tasks to ensure a coordinated effort. Small banks should regularly update and test these plans to address potential gaps and ensure all staff are familiar with their roles. Immediate actions, such as assessing physical damage to branches and ATMs, should be undertaken to determine the extent of disruption and allocate resources effectively.

Another essential strategy is to leverage technology to restore digital banking services quickly. Small banks should invest in robust backup systems, cloud-based platforms, and mobile banking solutions to ensure customers can access essential services even if physical branches are inaccessible. Implementing failover systems for core banking operations and data recovery mechanisms can minimize downtime. Additionally, banks should communicate with customers through multiple channels, such as SMS, email, and social media, to provide updates and reassure them of ongoing efforts to restore services.

Collaborating with local authorities, community organizations, and other financial institutions is a vital component of post-disaster recovery. Small banks can partner with larger institutions or industry associations to share resources, expertise, and temporary infrastructure. Engaging with local emergency management agencies can also help banks access critical information and support, such as temporary power supplies or security assistance. By working together, banks can expedite recovery efforts and contribute to the broader community’s resilience.

Prioritizing employee well-being and safety is crucial for a swift recovery. Small banks should ensure their staff have access to necessary resources, such as emergency funds, counseling services, and safe accommodations, to address personal challenges arising from the disaster. Providing clear guidance and support enables employees to focus on their roles in the recovery process. Banks should also consider temporary staffing solutions or cross-training employees to fill critical roles if some team members are unable to work.

Finally, conducting a post-disaster review and updating recovery plans is essential for long-term resilience. Small banks should evaluate the effectiveness of their response efforts, identify lessons learned, and incorporate these insights into their emergency plans. This includes reassessing risk exposure, updating insurance coverage, and investing in additional safeguards to better prepare for future events. By continuously improving their recovery strategies, small banks can enhance their ability to restore operations quickly and maintain customer trust in the face of adversity.

Citi Bank Record Retention: How Long Are Your Records Kept?

You may want to see also

Explore related products

![]()

Leveraging technology for remote banking during natural disasters

In the face of natural disasters, small banks must adapt quickly to ensure continuity of services for their customers. Leveraging technology for remote banking becomes a critical strategy to maintain operations when physical branches are inaccessible or damaged. One of the first steps small banks should take is to invest in robust digital banking platforms that enable customers to perform essential transactions remotely. This includes mobile banking apps, online banking portals, and telephone banking services. These platforms should be designed with user-friendly interfaces to cater to a diverse customer base, including those who may not be tech-savvy. By ensuring that customers can check balances, transfer funds, pay bills, and apply for loans from the safety of their homes, banks can minimize disruption and maintain customer trust during crises.

To further enhance remote banking capabilities, small banks should adopt cloud-based solutions for data storage and application hosting. Cloud technology ensures that banking systems remain operational even if physical infrastructure is compromised. It also allows for scalability, enabling banks to handle increased transaction volumes that may occur during emergencies. Additionally, cloud-based systems facilitate real-time updates and backups, reducing the risk of data loss. Implementing multi-factor authentication and encryption protocols is essential to safeguard customer information, as cybersecurity threats often increase during natural disasters when people are more vulnerable to scams and phishing attacks.

Another key aspect of leveraging technology is the use of communication tools to keep customers informed. Small banks should utilize SMS alerts, email notifications, and social media updates to provide timely information about branch closures, alternative banking options, and disaster relief programs. Automated messaging systems can be particularly useful for reaching a large number of customers simultaneously. Banks can also set up dedicated helplines or chatbots to address customer inquiries and provide assistance. Clear and consistent communication helps alleviate customer concerns and demonstrates the bank’s commitment to their well-being during challenging times.

Collaboration with fintech companies can also empower small banks to enhance their remote banking capabilities. Fintech partnerships can provide access to advanced technologies such as AI-driven customer service, digital payment solutions, and fraud detection systems. For instance, AI chatbots can handle routine customer queries, freeing up human resources to focus on more complex issues. Similarly, integrating digital wallet services can offer customers additional payment options when traditional methods are disrupted. By embracing fintech innovations, small banks can improve their resilience and responsiveness during natural disasters.

Finally, small banks should conduct regular disaster preparedness drills to test the effectiveness of their remote banking systems. This includes simulating various disaster scenarios to identify potential weaknesses and implement necessary improvements. Staff training is equally important, as employees need to be familiar with remote banking procedures and emergency protocols. Banks should also establish backup power and internet connectivity solutions to ensure uninterrupted service. By proactively preparing for natural disasters through technology-driven strategies, small banks can protect their operations, support their customers, and contribute to the overall recovery of their communities.

Exploring CBZ Bank's Reach: Total Number of Branches Revealed

You may want to see also

Explore related products

![]()

Financial resilience through insurance and risk mitigation measures

Small banks, often operating with limited resources compared to their larger counterparts, must prioritize financial resilience to withstand the economic shocks caused by natural disasters. One of the most effective strategies for achieving this resilience is through comprehensive insurance coverage and proactive risk mitigation measures. Insurance acts as a critical financial safety net, enabling banks to transfer a significant portion of their risk to insurers. Policies such as property insurance, business interruption insurance, and flood or earthquake coverage are essential for protecting physical assets, revenue streams, and operational continuity. For instance, business interruption insurance can cover lost income and ongoing expenses if a disaster forces the bank to close temporarily, ensuring liquidity and stability during recovery.

Beyond insurance, risk mitigation measures are vital for minimizing the impact of natural disasters. Small banks should conduct thorough risk assessments to identify vulnerabilities in their operations, infrastructure, and geographic locations. This includes evaluating the likelihood and potential severity of disasters such as hurricanes, wildfires, or floods. Based on these assessments, banks can implement physical safeguards, such as reinforcing buildings, installing backup power systems, and securing critical data through off-site storage or cloud-based solutions. Additionally, developing a robust disaster recovery plan is essential. This plan should outline clear procedures for communication, employee safety, and operational resumption, ensuring the bank can respond swiftly and effectively in the aftermath of a disaster.

Diversification of operations and resources is another key aspect of financial resilience. Small banks should avoid concentrating their assets or services in high-risk areas. For example, maintaining multiple branch locations or leveraging digital banking platforms can reduce reliance on a single physical site. Similarly, diversifying funding sources and maintaining adequate liquidity reserves can provide a buffer during times of crisis. Stress testing and scenario analysis can help banks understand their financial exposure and prepare for worst-case scenarios, ensuring they remain solvent even in the face of significant disruptions.

Collaboration and community engagement also play a crucial role in enhancing financial resilience. Small banks can partner with local governments, emergency management agencies, and other financial institutions to share resources, best practices, and contingency plans. Participating in community preparedness initiatives not only strengthens the bank’s ability to respond to disasters but also fosters goodwill and trust among customers. Moreover, educating clients about disaster preparedness and offering financial products like emergency loans or savings accounts can empower communities while reinforcing the bank’s role as a stabilizing force.

Finally, leveraging technology and innovation can significantly enhance a small bank’s ability to mitigate risks and recover from disasters. Implementing early warning systems, remote monitoring tools, and automated disaster response protocols can improve reaction times and reduce potential losses. Digital banking services ensure continuity of operations even when physical branches are inaccessible. Investing in cybersecurity is equally important, as disasters often coincide with increased cyber threats targeting vulnerable institutions. By integrating these technological solutions into their risk management frameworks, small banks can build a more resilient and adaptable financial infrastructure.

In conclusion, financial resilience for small banks in the face of natural disasters requires a multi-faceted approach centered on insurance and risk mitigation. By securing appropriate insurance coverage, implementing proactive safeguards, diversifying resources, fostering community partnerships, and embracing technological advancements, these institutions can protect their assets, maintain operations, and support their customers during challenging times. Such measures not only ensure survival but also position small banks as reliable pillars of economic stability in disaster-prone regions.

Are Capital One Bank's Fees Fair and Reasonable? A Review

You may want to see also

Explore related products

![]()

Community support and relief efforts led by small banks

Small banks play a pivotal role in community support and relief efforts during natural disasters, leveraging their local presence and deep understanding of the community’s needs. When disaster strikes, these banks often act as first responders in the financial sense, providing immediate assistance to individuals and businesses. One of the primary ways they contribute is by offering emergency loans with low or no interest rates to help residents and local businesses recover. These loans are designed to cover essential expenses such as home repairs, medical bills, or inventory replacement, ensuring that the community can begin rebuilding without the burden of high debt. Additionally, small banks frequently waive fees for services like ATM usage, wire transfers, and late payments, providing much-needed financial relief during a crisis.

Beyond financial products, small banks actively engage in grassroots relief efforts by organizing and participating in community initiatives. Many banks collaborate with local nonprofits, food banks, and emergency services to distribute essential supplies like food, water, and clothing. They also serve as collection points for donations, mobilizing their customer base to contribute to relief funds or supply drives. By acting as a hub for these activities, small banks strengthen community bonds and ensure that resources reach those most in need. Their employees often volunteer their time, further demonstrating the bank’s commitment to the community’s well-being.

Another critical aspect of small banks’ relief efforts is their role in providing financial education and guidance during and after a disaster. They offer workshops and one-on-one consultations to help individuals and businesses navigate insurance claims, apply for government assistance, and manage their finances in the aftermath of a disaster. This proactive approach empowers community members to make informed decisions and avoid long-term financial hardship. Small banks also work closely with local governments and disaster recovery agencies to ensure their services align with broader relief strategies.

Small banks often establish dedicated disaster relief funds or partner with existing ones to amplify their impact. These funds are typically supported by the bank’s own contributions, matched donations from customers, and grants from larger financial institutions or corporate partners. The flexibility of these funds allows them to address specific, evolving needs, such as temporary housing, mental health services, or infrastructure repairs. By pooling resources and collaborating with other stakeholders, small banks maximize their ability to support long-term recovery efforts.

Finally, small banks prioritize communication and accessibility during natural disasters, ensuring that their customers and community members remain informed and supported. They use multiple channels, including social media, email, and local media outlets, to share updates on branch closures, available services, and relief programs. Many banks also deploy mobile units or temporary branches in affected areas to provide on-the-ground assistance. This commitment to staying connected and accessible reinforces trust and demonstrates the bank’s role as a reliable partner in times of crisis. Through these multifaceted efforts, small banks not only aid in immediate recovery but also contribute to the resilience and sustainability of the communities they serve.

Annual Bank Robbery Statistics: Uncovering the Frequency of Heists

You may want to see also

Frequently asked questions

Small banks prepare for natural disasters by developing comprehensive disaster recovery plans, backing up critical data off-site, ensuring redundant communication systems, training staff on emergency protocols, and maintaining relationships with local emergency services and vendors.

Small banks protect customer data by encrypting sensitive information, storing backups in secure, off-site locations, using cloud-based systems for redundancy, and implementing cybersecurity measures to prevent breaches during disruptions.

Small banks ensure continuity by activating backup branches or mobile units, leveraging remote work capabilities, partnering with other financial institutions for temporary support, and communicating regularly with customers about service availability.

Insurance plays a critical role by providing financial protection against property damage, business interruption, and liability claims. Small banks typically carry policies tailored to their size and risk exposure to mitigate financial losses.

Small banks support their communities by offering loan payment deferrals, providing emergency loans, waiving fees, participating in local relief efforts, and collaborating with nonprofits and government agencies to aid recovery.