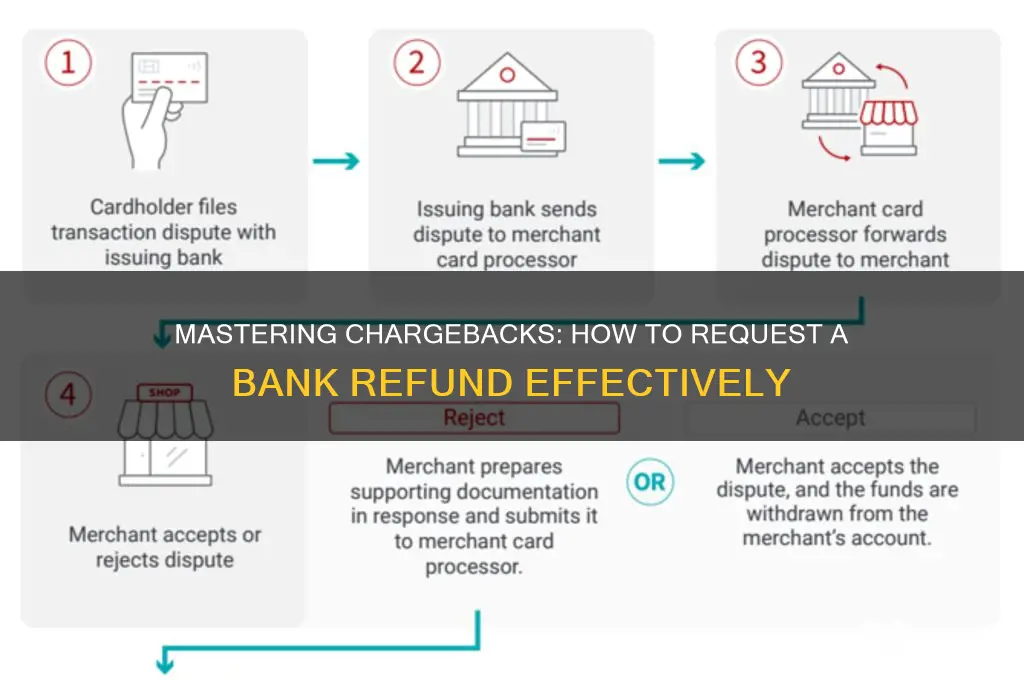

A chargeback is a powerful tool for consumers to dispute unauthorized or fraudulent transactions on their bank accounts, and understanding how to request one is essential for protecting your finances. If you notice an incorrect or unrecognized charge, the first step is to contact your bank promptly, as there are often time limits for filing a claim. You can typically initiate the process by calling your bank's customer service, visiting a local branch, or using their online banking platform. When requesting a chargeback, be prepared to provide detailed information about the transaction, including the date, amount, and merchant involved, along with any supporting documentation, such as receipts or communication with the merchant. The bank will then investigate the claim and, if valid, reverse the charge, ensuring your funds are safeguarded.

| Characteristics | Values |

|---|---|

| Definition | A chargeback is a reversal of a credit or debit card charge initiated by the cardholder. |

| Eligibility | Fraudulent charges, unauthorized transactions, or goods/services not received. |

| Timeframe | Typically within 120 days of the transaction (varies by bank and card issuer). |

| Required Documentation | Receipts, order confirmations, communication with the merchant, and transaction details. |

| Process | Contact your bank, provide necessary details, and submit a formal dispute request. |

| Contact Methods | Phone, online banking portal, email, or in-person at a branch. |

| Investigation Period | Banks usually have 30-90 days to investigate the claim. |

| Outcome | Funds may be temporarily credited during investigation; final decision based on evidence. |

| Potential Fees | Some banks may charge a fee if the dispute is unsuccessful (varies by bank). |

| Impact on Credit Score | Chargebacks do not directly affect credit scores but may impact relationships with banks. |

| Merchant Response | Merchants can dispute the chargeback, potentially reversing the reversal. |

| Prevention Tips | Monitor transactions regularly, use secure payment methods, and keep records of purchases. |

Explore related products

What You'll Learn

- Gather Evidence: Collect receipts, statements, and communication records to support your claim

- Understand Eligibility: Ensure the transaction qualifies for a chargeback under bank policies

- Contact Your Bank: Call or visit your bank to initiate the chargeback process

- Submit a Dispute: Provide all required documentation and details to file the dispute

- Follow Up: Track the status and respond promptly to any bank requests

![]()

Gather Evidence: Collect receipts, statements, and communication records to support your claim

When preparing to request a chargeback from your bank, gathering evidence is crucial to support your claim. Start by collecting all receipts related to the transaction in question. This includes physical receipts, digital receipts sent via email, or screenshots of online purchases. Ensure the receipt clearly shows the date, amount, merchant name, and details of the product or service. If the receipt is missing or incomplete, contact the merchant directly to request a copy. Without a receipt, your claim may lack the foundational proof needed to proceed.

Next, review your bank statements to identify the exact transaction and verify the amount charged. Highlight or print the relevant portion of the statement that shows the transaction date, amount, and merchant details. If the transaction appears incorrect or unauthorized, this documentation will serve as critical evidence. Additionally, check for any recurring charges or discrepancies that might strengthen your case. Your bank will need this information to trace the transaction and assess the validity of your claim.

Communication records are another vital piece of evidence. Compile all emails, chat logs, or letters exchanged with the merchant regarding the transaction. This includes any attempts to resolve the issue directly with the seller, such as requests for refunds, explanations of discrepancies, or complaints about the product or service. Organize these records chronologically to demonstrate your efforts to address the problem before involving the bank. Clear communication records show that you acted in good faith and exhausted other options before seeking a chargeback.

If the dispute involves a product or service, document its condition or failure. Take photos or videos of defective items, write down details of services not rendered, or note any discrepancies between what was promised and what was delivered. For digital purchases, save screenshots of errors or issues. This visual or written evidence can help illustrate why the charge is disputed and provide additional context to your claim. Be specific and thorough in your documentation to leave no room for ambiguity.

Finally, organize all evidence in a clear and accessible format. Create a folder, either physical or digital, to store receipts, statements, communication records, and any other supporting documents. Label each item clearly and include a brief summary of its relevance to your claim. When submitting your evidence to the bank, provide a concise explanation of why you are disputing the charge and reference the specific documents that support your case. A well-organized submission not only makes it easier for the bank to review your claim but also demonstrates your seriousness and preparedness.

US Bank Stadium: A Modern Marvel in Minneapolis

You may want to see also

Explore related products

![]()

Understand Eligibility: Ensure the transaction qualifies for a chargeback under bank policies

Understanding eligibility is the first critical step when considering a chargeback request with your bank. Not all transactions qualify for a chargeback, and banks have specific policies that dictate when they can intervene on your behalf. Start by reviewing your bank’s chargeback policy, which is typically outlined in your account terms and conditions or on their website. Common scenarios that may qualify include unauthorized transactions, where someone uses your card without permission; goods or services not received, such as paying for an item that never arrives; or goods received in a condition significantly different from what was described. Familiarize yourself with these categories to determine if your situation aligns with the bank’s criteria.

Next, verify the timing of the transaction in relation to your bank’s chargeback deadlines. Most banks require you to report the issue within a specific timeframe, often 60 to 120 days from the transaction date. Missing this window can disqualify your request, so act promptly. Additionally, ensure the transaction was made with a payment method covered by the bank’s chargeback policy, such as credit or debit cards, as certain payment types like cash or wire transfers may not be eligible.

It’s also important to confirm that you have already attempted to resolve the issue directly with the merchant. Banks typically require proof that you’ve made a good-faith effort to address the problem before initiating a chargeback. This could involve contacting the seller to request a refund, return, or resolution. Keep records of all communications, including emails, receipts, and notes from phone calls, as these will be essential when filing your claim.

Another factor to consider is whether the transaction falls under specific exclusions in your bank’s policy. For example, chargebacks may not be allowed for disputes over the quality of a service (e.g., dissatisfaction with a haircut) or for transactions where you’ve voluntarily shared your card details with someone you know. Understanding these exclusions helps you assess whether your case is likely to be approved.

Finally, be aware of the difference between a chargeback and other forms of dispute resolution, such as fraud claims or Section 75 claims (in the UK). Chargebacks are typically handled through card networks like Visa or Mastercard, while other protections may involve different processes. Ensure you’re pursuing the correct avenue based on the nature of your dispute. By thoroughly understanding these eligibility criteria, you can confidently determine whether your transaction qualifies for a chargeback under your bank’s policies.

Understanding Your Borrowing Power: How Banks Assess Your Loan Capacity

You may want to see also

Explore related products

![]()

Contact Your Bank: Call or visit your bank to initiate the chargeback process

When initiating a chargeback, the first and most crucial step is to contact your bank directly. This can be done either by calling their customer service hotline or by visiting a local branch in person. Calling is often the quickest method, as it allows you to speak with a representative immediately. Most banks have dedicated lines for dispute resolution or fraudulent charges, so ensure you select the appropriate option when prompted. If you prefer a face-to-face interaction, visiting your bank allows you to discuss the issue in detail with a banker who can guide you through the process. Whichever method you choose, be prepared to provide your account information and details about the transaction in question.

During the call or visit, clearly state your intention to request a chargeback. Explain the situation concisely, including the date of the transaction, the amount, and the reason you believe the charge is invalid. Common reasons for chargebacks include unauthorized transactions, goods or services not received, or products that were significantly different from what was advertised. The bank representative will likely ask for specific documentation, such as receipts, order confirmations, or communication with the merchant, so have these ready beforehand. If you’re unsure about what to include, ask the representative for a list of required documents to ensure your request is processed smoothly.

If you’re visiting the bank in person, bring all relevant documentation with you in physical or digital form. The banker will review your case and may ask follow-up questions to better understand the situation. Be honest and detailed in your responses, as this will help the bank assess the validity of your claim. In some cases, the banker may initiate the chargeback process immediately, while in others, they may need to escalate the request to a specialized department. Either way, make sure to obtain a reference number or confirmation of your request for future follow-ups.

When calling your bank, remain patient and polite, even if the process seems lengthy or frustrating. Chargebacks involve a formal procedure, and the representative is there to assist you, not to create obstacles. If you encounter difficulty or feel the representative is not addressing your concerns, politely ask to speak with a supervisor or a member of the disputes team. Keep a record of the date and time of your call, the name of the representative you spoke with, and any reference numbers provided. This information will be useful if you need to follow up on your request later.

After initiating the chargeback, your bank will typically investigate the claim, which may take several days to weeks depending on the complexity of the case. During this period, the disputed amount may be temporarily credited back to your account, though this varies by bank policy. Stay in touch with your bank to monitor the progress of your request and provide any additional information they may require. Remember, contacting your bank promptly and providing thorough documentation significantly increases the likelihood of a successful chargeback.

How Long Do Bank Cash Transfers Take? A Comprehensive Guide

You may want to see also

![]()

Submit a Dispute: Provide all required documentation and details to file the dispute

To successfully submit a dispute for a chargeback, you must gather and provide all necessary documentation and details to your bank. Start by collecting evidence that supports your claim, such as receipts, invoices, order confirmations, or any communication with the merchant. If the dispute involves a service, include contracts, terms of service, or proof of cancellation. For unauthorized transactions, gather any relevant information that demonstrates the charge was made without your consent, such as account statements or notifications of suspicious activity. Organizing these documents in a clear, chronological order will streamline the process and help your bank understand your case.

Next, contact your bank to initiate the dispute process. Most banks offer multiple channels for submission, including online banking portals, phone support, or in-person visits to a branch. When reaching out, have your account information and the specific transaction details ready, such as the date, amount, and merchant name. Clearly explain the reason for the dispute, whether it’s due to unauthorized charges, goods not received, defective products, or services not rendered. Be concise but thorough in your explanation to ensure the bank fully grasps the issue.

Once you’ve initiated the dispute, your bank will provide a list of required documents to formally file the claim. Carefully review this list and submit all requested materials promptly. This may include signed affidavits, copies of the evidence you’ve gathered, or additional forms specific to your bank’s process. Ensure all documentation is legible and complete to avoid delays. If any information is missing or unclear, the bank may reject your dispute, so double-check everything before submission.

After submitting your dispute, keep a record of all communications with your bank, including confirmation numbers, case IDs, and the names of representatives you speak with. This documentation will be useful if you need to follow up or escalate the issue later. Your bank will investigate the dispute, which may take several weeks, and they will notify you of the outcome. During this period, continue monitoring your account and refrain from contacting the merchant directly, as the bank handles the process on your behalf.

Finally, be aware of your bank’s specific deadlines for filing chargebacks, as these vary depending on the type of dispute and the institution’s policies. Missing these deadlines can result in the forfeiture of your right to dispute the charge. Stay proactive and responsive throughout the process, providing any additional information your bank requests promptly. By following these steps and providing all required documentation, you maximize your chances of a successful chargeback resolution.

Securely Transfer Money to Vanguard: Is It Safe?

You may want to see also

![]()

Follow Up: Track the status and respond promptly to any bank requests

After initiating a chargeback request with your bank, it's crucial to stay proactive and engaged in the process to ensure a successful resolution. The follow-up phase is just as important as the initial request, as it involves tracking the status of your claim and responding promptly to any bank inquiries. Here’s how to effectively manage this stage:

Monitor the Chargeback Status Regularly: Most banks provide an online portal or mobile app where you can track the progress of your chargeback request. Log in to your account frequently to check for updates. If your bank doesn’t offer digital tracking, call their customer service line periodically to inquire about the status. Keep a record of all communications, including dates, times, and the names of representatives you speak with. This documentation can be invaluable if there are discrepancies or delays in the process.

Respond Promptly to Bank Requests: During the chargeback investigation, your bank may require additional information or documentation to support your claim. This could include receipts, correspondence with the merchant, or proof of the disputed transaction. Respond to any requests from the bank immediately to avoid delays. If you’re unsure about what’s needed, ask for clarification. Timely responses demonstrate your commitment to resolving the issue and can expedite the process.

Understand the Timeline: Chargeback investigations typically take 30 to 90 days, depending on the complexity of the case and your bank’s policies. Be patient but persistent. If the process seems to be taking longer than expected, follow up with your bank to ensure your case hasn’t been overlooked. Politely inquire about the next steps and any additional actions you can take to assist in the investigation.

Stay Informed About the Outcome: Once the investigation is complete, your bank will notify you of the decision. If the chargeback is approved, the disputed amount will be credited back to your account. If it’s denied, ask for a detailed explanation of the reasons. You may have the option to appeal the decision or pursue other avenues, such as contacting the merchant directly or seeking assistance from regulatory bodies like the Consumer Financial Protection Bureau (CFPB).

Keep Detailed Records: Throughout the follow-up process, maintain a comprehensive file of all correspondence, documents, and notes related to your chargeback. This includes emails, letters, and any written communication with the bank or merchant. Organized records will help you address any disputes or misunderstandings that may arise and provide a clear history of your efforts to resolve the issue. By staying vigilant and responsive during the follow-up phase, you maximize your chances of a favorable outcome in the chargeback process.

Mastering Coal Fire Banking: Tips for Efficient and Safe Heat Retention

You may want to see also

Frequently asked questions

A chargeback is a reversal of a transaction initiated by your bank to return funds to your account. Request one if you were charged for a product or service you didn’t receive, if the purchase was unauthorized, or if the merchant refuses to issue a refund.

Contact your bank’s customer service via phone, online banking, or in person. Provide details of the transaction, including the date, amount, merchant name, and reason for the dispute. Your bank will guide you through their specific process.

Gather proof such as receipts, order confirmations, communication with the merchant, screenshots of unauthorized transactions, or any other documentation that supports your claim. The more evidence you provide, the stronger your case.

The process can take anywhere from a few days to several months, depending on the complexity of the case and your bank’s policies. Your bank will typically provide a temporary credit while investigating.

Yes, merchants can dispute a chargeback by providing evidence that the transaction was valid. If this happens, your bank will review both sides and make a final decision. If the merchant wins, the charge may be reinstated to your account.