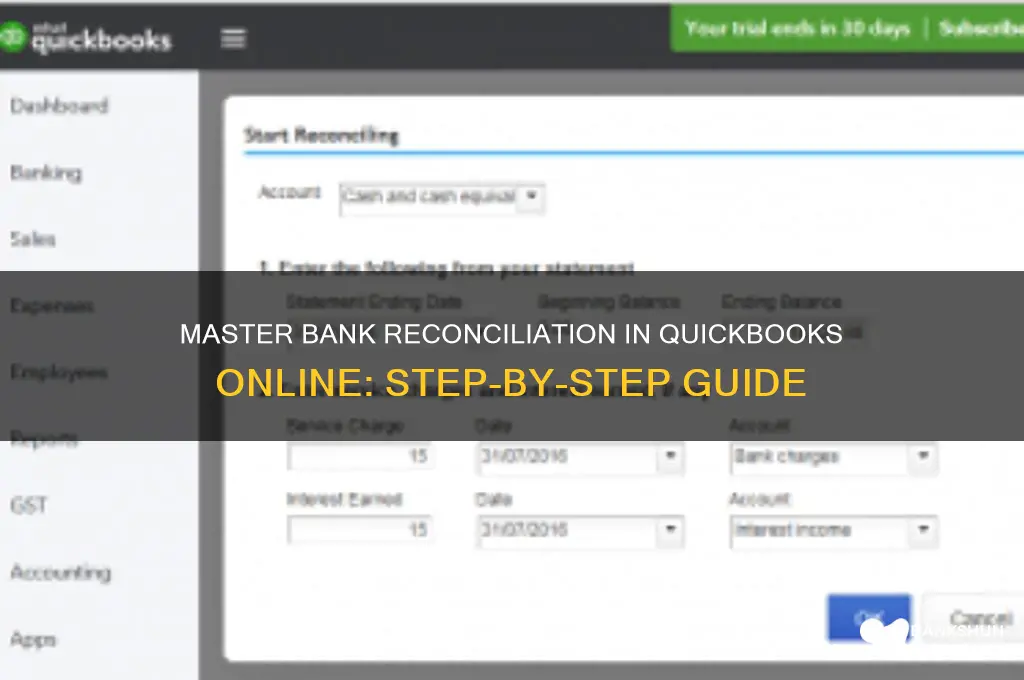

Bank reconciliation in QuickBooks Online (QBO) is a critical process for ensuring the accuracy of your financial records by comparing your business’s bank or credit card statements with the transactions recorded in QuickBooks. This process helps identify discrepancies, such as missing or uncleared transactions, and ensures that your books reflect the true financial position of your business. To perform a bank reconciliation in QBO, start by navigating to the Banking menu, selecting the account you wish to reconcile, and then clicking on the Reconcile button. Follow the prompts to enter the statement’s ending balance and date, and then match the transactions in QuickBooks with those on your bank statement. Carefully review any unmatched transactions and make necessary adjustments to resolve discrepancies. Completing this process regularly not only maintains financial accuracy but also helps in detecting errors or fraudulent activities early on.

| Characteristics | Values |

|---|---|

| Purpose | To match QuickBooks Online (QBO) transactions with bank statements. |

| Frequency | Monthly or as needed to ensure accuracy. |

| Prerequisites | Bank account connected to QBO, updated bank statement, and reconciled QBO transactions. |

| Steps | 1. Go to Accounting > Reconcile. |

| 2. Select the bank account to reconcile. | |

| 3. Enter the Ending Balance and Ending Date from the bank statement. | |

| 4. Match QBO transactions with bank statement transactions by checking the box next to each matched item. | |

| 5. Adjust for uncleared transactions or discrepancies. | |

| 6. Click Finish Now when the difference is zero. | |

| Matching Transactions | Automatically matches transactions based on date, amount, and description. |

| Manual Adjustments | Allows adding missing transactions or correcting errors during reconciliation. |

| Reconciliation Report | Generates a report showing matched and unmatched transactions. |

| Undo Reconciliation | Possible by locating the reconciliation in the Reconciliation Reports and clicking Undo. |

| Best Practices | Regularly reconcile, review uncleared transactions, and ensure accurate data entry. |

| Common Issues | Missing transactions, incorrect starting balance, or uncleared deposits/payments. |

| Tools | QBO’s built-in reconciliation tool, bank feeds for automatic transaction import. |

| Support | QBO Help Center, community forums, or QuickBooks support for assistance. |

Explore related products

What You'll Learn

- Prepare Bank Statement: Gather and organize the latest bank statement for the reconciliation period

- Match Transactions: Compare QBO transactions with bank statement entries to identify matches

- Identify Discrepancies: Locate unmatched transactions, fees, or errors in QBO or the bank statement

- Adjust QBO Records: Enter missing transactions or correct errors in QuickBooks Online

- Finalize Reconciliation: Confirm all transactions match and complete the reconciliation process in QBO

![]()

Prepare Bank Statement: Gather and organize the latest bank statement for the reconciliation period

The foundation of any bank reconciliation lies in the accuracy and completeness of your bank statement. Before diving into QuickBooks Online (QBO), ensure you have the latest statement for the period you're reconciling. This isn't just about grabbing the most recent document; it's about verifying its integrity. Check the statement's date range aligns perfectly with your reconciliation period. Even a one-day discrepancy can throw off your entire process, leading to frustrating mismatches between your records and the bank's.

Pro Tip: If your bank offers downloadable statements in formats like CSV or QBO, utilize these. They often integrate seamlessly with QBO, reducing manual data entry and minimizing errors.

Once you've secured the correct statement, organization is key. A disorganized statement is a recipe for confusion and mistakes. Start by highlighting or marking key sections: opening and closing balances, deposits, withdrawals, fees, and any other transactions. This visual breakdown makes it easier to compare line by line with your QBO records. Consider creating a simple spreadsheet to list transactions chronologically, especially if your statement is lengthy. This allows for easier sorting, filtering, and identification of potential discrepancies.

Caution: Don't rely solely on digital organization. Keep a physical copy of the statement readily available for reference during the reconciliation process.

While organizing, be vigilant for anomalies. Look for duplicate entries, unfamiliar transactions, or amounts that seem out of the ordinary. These could indicate errors, fraudulent activity, or simply transactions that haven't cleared yet. Flagging these items early allows you to investigate and address them before they become roadblocks in the reconciliation process. Remember, a thorough review at this stage saves time and headaches later.

Finally, ensure your QBO account is ready to receive the statement data. Double-check that your bank account in QBO is correctly set up and linked to the appropriate bank feed (if applicable). Verify the opening balance in QBO matches the opening balance on your bank statement. This initial alignment is crucial for a smooth reconciliation process. By taking the time to meticulously prepare your bank statement, you're setting the stage for a successful and efficient reconciliation in QBO.

Professional Tips for Addressing a Bank Manager in Your Email

You may want to see also

Explore related products

![]()

Match Transactions: Compare QBO transactions with bank statement entries to identify matches

Matching transactions is the backbone of bank reconciliation in QuickBooks Online (QBO). This process involves a meticulous comparison of your QBO-recorded transactions with those on your bank statement, ensuring every penny is accounted for. Think of it as a financial detective work, where each entry needs to be cross-referenced and verified. The goal is to identify which transactions in QBO correspond to the charges and deposits listed on your bank statement, leaving no room for discrepancies.

To begin, open your bank account in QBO and access the reconciliation tool. Here, you’ll see a list of transactions recorded in QBO alongside the ending balance from your bank statement. Start by scanning for obvious matches—transactions with identical dates, amounts, and descriptions. For instance, a $150 deposit from "Client A" on March 15th in QBO should align with the same entry on your bank statement. Mark these matches as "cleared" in QBO to indicate they’ve been verified. Be cautious, though; similar amounts or dates don’t always signify a match. Always double-check the payee or description to avoid pairing unrelated transactions.

For less obvious matches, dig deeper. Sometimes, transactions may appear different due to variations in how banks and QBO label entries. For example, a bank might list a transaction as "AMZN*Subscription" while QBO records it as "Amazon Prime." In such cases, use the transaction details to confirm the match. If a transaction in QBO is split into categories (e.g., supplies and shipping), ensure the total amount aligns with the bank statement entry. If discrepancies persist, investigate further—it could be a sign of an unrecorded transaction or an error in data entry.

A practical tip: leverage QBO’s search and filter tools to streamline the matching process. Filter transactions by date range or amount to narrow down possibilities. For recurring transactions, like monthly subscriptions, create rules in QBO to automatically categorize them, reducing manual effort. Additionally, keep an eye on uncleared transactions—those not yet matched. These could be pending transactions that haven’t cleared the bank or entries missed in QBO. Regularly reconciling your accounts monthly ensures these discrepancies are caught early, preventing compounding errors.

In conclusion, matching transactions requires precision, patience, and a keen eye for detail. By systematically comparing QBO entries with bank statement data, you not only ensure accuracy but also build a robust financial record. Remember, the goal isn’t just to balance numbers but to maintain transparency and trust in your financial reporting. With practice, this process becomes second nature, transforming a potentially daunting task into a manageable routine.

Does Renters Insurance Cover Stolen Bank Funds? What You Need to Know

You may want to see also

Explore related products

![]()

Identify Discrepancies: Locate unmatched transactions, fees, or errors in QBO or the bank statement

Unmatched transactions are the red flags of bank reconciliation in QBO. They signal potential errors, overlooked entries, or timing differences between your records and the bank's. Identifying these discrepancies is crucial for maintaining accurate financial data and preventing costly mistakes.

Start by comparing each transaction in your QBO register to the corresponding bank statement. Look for missing entries, duplicate postings, or amounts that don't align. Pay close attention to fees charged by the bank, as these are often overlooked and can throw off your balance.

A systematic approach is key. Begin with the largest transactions, as these are easier to spot and often have a bigger impact on your reconciliation. Then, move to smaller amounts, meticulously checking dates, payees, and descriptions. Utilize QBO's search and filter functions to isolate specific transactions or identify patterns. For example, filter by date range or transaction type to narrow down potential discrepancies.

Remember, not all unmatched transactions are errors. Timing differences are common, especially with outstanding checks or deposits in transit. Note these on your reconciliation worksheet and ensure they clear in subsequent statements.

Don't rely solely on visual inspection. Leverage QBO's reconciliation tools. The software can automatically match transactions based on amount and date, flagging those that don't align. However, don't blindly accept these matches. Double-check each one to ensure accuracy, as the software can sometimes make incorrect pairings.

Finally, document everything. Keep a detailed record of all discrepancies, their resolution, and any adjustments made to your QBO records. This audit trail is invaluable for future reference and ensures transparency in your financial reporting. By meticulously identifying and addressing unmatched transactions, you'll achieve a successful bank reconciliation and maintain the integrity of your financial data.

Does TC Bank Offer Notary Public Services? Find Out Here

You may want to see also

Explore related products

![]()

Adjust QBO Records: Enter missing transactions or correct errors in QuickBooks Online

Accurate financial records are the backbone of any successful business, and QuickBooks Online (QBO) is a powerful tool to maintain them. However, discrepancies between your bank statement and QBO records can occur due to missing transactions, data entry errors, or timing differences. Adjusting QBO records by entering missing transactions or correcting errors is a critical step in the bank reconciliation process, ensuring your financial data remains reliable and up-to-date.

Identifying Discrepancies: The First Step

Begin by comparing your bank statement to the transactions recorded in QBO. Look for transactions that appear on the statement but are missing in QBO, such as deposits, withdrawals, or fees. Similarly, identify any errors in existing entries, like incorrect amounts, duplicate transactions, or misclassified expenses. Use the QBO reconciliation tool to highlight these discrepancies, making it easier to pinpoint what needs adjustment. For instance, if a $500 client payment is on your bank statement but not in QBO, this is a clear missing transaction that requires immediate entry.

Entering Missing Transactions: A Methodical Approach

To add a missing transaction, navigate to the Banking menu in QBO and select the appropriate account. Click "Add" or "New Transaction" and input the details, including date, amount, and category. Ensure the transaction is categorized correctly to maintain accurate financial reporting. For example, a missing vendor payment should be tagged under the relevant expense account. If the transaction involves a transfer between accounts, use the Transfer feature to avoid double-entry errors. Always double-check the details before saving to prevent further discrepancies.

Correcting Errors: Precision is Key

When correcting errors, locate the incorrect transaction in QBO and edit it directly. Common errors include wrong amounts, incorrect payees, or mismatched categories. For instance, if a $300 office supply purchase was mistakenly entered as $30, edit the transaction to reflect the correct amount. If a transaction was duplicated, delete one instance to avoid skewing your financial data. Be cautious not to alter reconciled transactions unless absolutely necessary, as this can disrupt previous reconciliations. Instead, create a journal entry to adjust the balance if the error is historical.

Best Practices for Seamless Adjustments

To streamline the adjustment process, maintain a consistent workflow. Regularly review bank statements and reconcile accounts monthly to catch discrepancies early. Use QBO’s matching feature to link bank statement transactions to existing entries, reducing manual input. Keep detailed notes or use the memo field in QBO to document the reason for adjustments, ensuring transparency. Finally, leverage QBO’s audit trail feature to track changes, providing accountability and a reference for future reviews. By staying proactive and meticulous, you’ll ensure your QBO records remain accurate and trustworthy.

Understanding CD in Banking: What Does It Mean?

You may want to see also

Explore related products

![]()

Finalize Reconciliation: Confirm all transactions match and complete the reconciliation process in QBO

As you approach the final stage of bank reconciliation in QuickBooks Online (QBO), the goal is clear: ensure every transaction aligns perfectly between your records and the bank statement. This step is not just about ticking boxes; it’s about verifying accuracy, resolving discrepancies, and locking in financial integrity. Start by cross-referencing each transaction in QBO with the bank statement, ensuring dates, amounts, and descriptions match precisely. Use the reconciliation tool’s side-by-side view to streamline this process, flagging any unmatched items for further investigation.

Once all transactions are confirmed, address any discrepancies systematically. Unmatched items could stem from uncleared checks, pending deposits, or data entry errors. For uncleared checks, verify their issuance date and ensure they haven’t been cashed. Pending deposits may require patience, but if they’re overdue, contact the bank. Data entry errors demand immediate correction—double-check amounts, categories, and dates in QBO. If discrepancies persist, consider reaching out to your bank for clarification or reviewing previous reconciliations for patterns.

Completing the reconciliation process in QBO involves finalizing the report and marking it as reconciled. Before clicking “Finish,” review the summary for accuracy, ensuring the ending balance matches the bank statement. Once finalized, QBO locks the reconciliation period, preventing accidental edits. This step is irreversible, so treat it as a checkpoint: double-check everything, from cleared transactions to the final balance. A well-executed reconciliation not only ensures accuracy but also builds trust in your financial reporting.

Practical tips can enhance this process. For instance, use QBO’s “Reconciliation Discrepancies” report to identify unresolved issues. If you’re reconciling multiple accounts, prioritize high-activity accounts first to manage complexity. Additionally, set a recurring reminder to reconcile monthly, as consistency reduces errors and simplifies troubleshooting. By treating this step as a meticulous review rather than a formality, you transform reconciliation from a chore into a cornerstone of financial clarity.

The Ancient Persians: Banking System Pioneers

You may want to see also

Frequently asked questions

Bank reconciliation in QuickBooks Online (QBO) is the process of matching your bank statement transactions with those recorded in QBO to ensure accuracy and identify discrepancies. It’s important because it helps maintain financial integrity, detect errors, and prevent fraud, ensuring your books reflect the true financial position of your business.

To start bank reconciliation in QBO, go to the Accounting menu, select Chart of Accounts, and choose the bank account you want to reconcile. Click on the Reconcile button, enter the ending balance and ending date from your bank statement, and then match transactions between QBO and your statement.

If there are unmatched transactions, first check for errors in date ranges or missed entries. If the issue persists, investigate for missing transactions, uncleared checks, or deposits in transit. You can also create manual journal entries or adjust existing transactions to resolve discrepancies before finalizing the reconciliation.