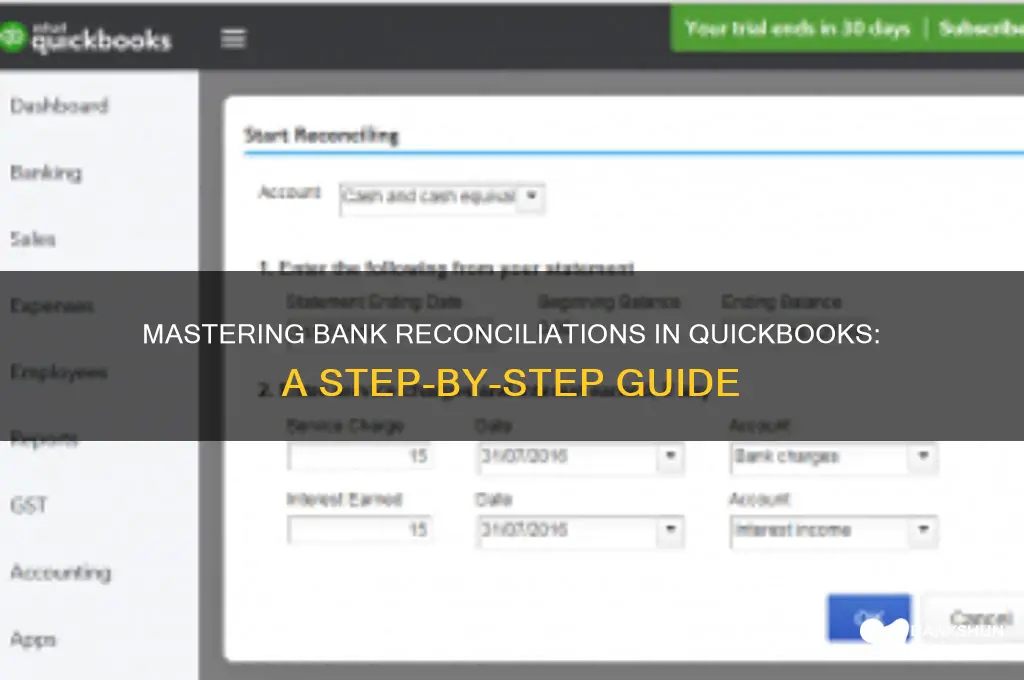

Bank reconciliations in QuickBooks are a critical process for ensuring the accuracy of your financial records by comparing your QuickBooks transactions with your bank statements. This task helps identify discrepancies, such as missing transactions, errors, or uncleared items, and ensures that your books align with your actual bank activity. In QuickBooks, the reconciliation process involves matching transactions, adjusting for timing differences, and resolving any unmatched items. By regularly performing bank reconciliations, you can maintain financial integrity, detect fraud, and make informed business decisions based on reliable data. QuickBooks simplifies this process with its user-friendly interface and automated tools, making it accessible even for those with limited accounting experience.

Explore related products

What You'll Learn

- Prepare Bank Statement: Gather and organize the latest bank statement for the reconciliation period

- Match Transactions: Compare QuickBooks transactions with bank statement entries to identify matches

- Identify Discrepancies: Locate and resolve unmatched or missing transactions in QuickBooks or the bank

- Adjust Entries: Record missing transactions, corrections, or bank fees in QuickBooks as needed

- Finalize Reconciliation: Confirm all discrepancies are resolved and mark the reconciliation as complete

![]()

Prepare Bank Statement: Gather and organize the latest bank statement for the reconciliation period

The foundation of any successful bank reconciliation in QuickBooks lies in the accuracy and organization of your bank statement. Think of it as the blueprint for the entire process. Without a clear, complete, and up-to-date statement, you're essentially navigating in the dark.

Begin by securing the latest bank statement covering the exact reconciliation period you're working on. This might seem obvious, but using an outdated or partial statement is a common pitfall. Most banks offer digital statements downloadable in PDF or CSV formats. Opt for the CSV if available, as it allows for easier import into QuickBooks, saving you from manual data entry.

Once downloaded, take a moment to review the statement for clarity. Ensure all transactions are legible and that the date range aligns perfectly with your QuickBooks reconciliation period. Highlight or flag any unusual entries, such as large deposits or withdrawals, for closer scrutiny during the reconciliation process.

Organizing the statement is equally crucial. If you’re working with a paper statement or a poorly formatted digital one, consider transferring the data into a spreadsheet. Group transactions by type (e.g., deposits, withdrawals, fees) and sort them chronologically. This not only makes the data easier to compare with QuickBooks but also helps identify discrepancies early on.

Finally, keep the original statement handy for reference. Even if you’re working with a digital copy, having the source document ensures you can verify details if questions arise. A well-prepared bank statement is your first line of defense against errors, setting the stage for a seamless reconciliation process in QuickBooks.

How Treasury Bills Impact Bank Reserves and Monetary Policy

You may want to see also

Explore related products

![]()

Match Transactions: Compare QuickBooks transactions with bank statement entries to identify matches

Matching transactions is the cornerstone of accurate bank reconciliations in QuickBooks, ensuring your financial records align with your actual bank activity. Begin by importing your bank statement into QuickBooks, either manually or through a secure bank feed. QuickBooks will automatically attempt to match transactions, but it’s your responsibility to verify these pairings for accuracy. Look for identical dates, amounts, and payees between your QuickBooks register and the bank statement. For instance, a $350 deposit from "ABC Client" on 05/10 should match precisely in both systems. Discrepancies, even minor ones, can indicate errors or unrecorded transactions.

When QuickBooks suggests a match, scrutinize it carefully. Automatic matching isn’t infallible—it may pair transactions based on amount alone, overlooking critical details like the payee or transaction type. For example, a $120 withdrawal labeled "Office Supplies" in QuickBooks might be incorrectly matched with a $120 ATM withdrawal on the bank statement. Always cross-reference additional details to confirm the match is legitimate. If unsure, leave the transaction unmatched and investigate further before finalizing the reconciliation.

Unmatched transactions require manual intervention. Start by reviewing transactions near the date in question, as timing differences (e.g., checks clearing later than expected) are common culprits. For instance, a check written on 05/01 might appear on the bank statement on 05/05. If you still can’t find a match, consider the possibility of an unrecorded transaction, such as a bank fee or interest payment. Add these to QuickBooks as needed, ensuring every entry on the bank statement has a corresponding record in your software.

Practical tips can streamline this process. Use QuickBooks’ search function to quickly locate transactions by amount or payee. For recurring transactions, create memorized entries to reduce manual input and improve accuracy. Additionally, leverage QuickBooks’ reconciliation tools, such as the "Locators" feature, which highlights discrepancies between your register and the bank statement. Finally, maintain consistency in transaction categorization—for example, always code "Utilities" under the same expense account—to avoid confusion during matching.

In conclusion, matching transactions in QuickBooks requires attention to detail, systematic verification, and proactive problem-solving. By combining QuickBooks’ automated tools with manual scrutiny, you can ensure your financial records accurately reflect your bank activity. Remember, the goal isn’t just to complete the reconciliation but to maintain a reliable, audit-ready financial ledger. Treat each unmatched transaction as an opportunity to refine your processes and improve accuracy over time.

Easy Steps to Purchase Airtime via Stanbic Bank Online

You may want to see also

Explore related products

![]()

Identify Discrepancies: Locate and resolve unmatched or missing transactions in QuickBooks or the bank

Unmatched or missing transactions are the Achilles' heel of any bank reconciliation. In QuickBooks, these discrepancies can stem from data entry errors, timing differences, or overlooked transactions. To locate them, start by comparing the "Uncleared Transactions" report in QuickBooks with your bank statement. Look for transactions that appear on one but not the other. For instance, a check you issued might not have cleared yet, or a bank fee could be missing from your QuickBooks register. Use the "Find" feature in QuickBooks to search for specific amounts or dates, narrowing down potential mismatches.

Once identified, resolving discrepancies requires a methodical approach. For missing transactions in QuickBooks, manually add them to the register, ensuring the date, amount, and payee match the bank statement. If a transaction is missing from the bank statement, verify its status—it might still be processing. For unmatched transactions, investigate further. For example, a deposit recorded in QuickBooks as $500 but appearing as $495 on the bank statement could indicate a bank service charge. Adjust the transaction in QuickBooks to reflect the correct amount and categorize the fee appropriately.

A common pitfall is assuming the bank is always correct. QuickBooks users often overlook errors in bank statements, such as duplicate charges or incorrect amounts. Cross-reference transactions with supporting documents like receipts or invoices to confirm accuracy. If a discrepancy persists, contact your bank to clarify or request a statement correction. QuickBooks’ "Reconcile" tool can help flag unresolved issues, but it’s your diligence that ensures accuracy.

To streamline this process, leverage QuickBooks’ reconciliation tools. The "Reconcile Discrepancies" window allows you to mark transactions as cleared or adjust entries directly. For recurring discrepancies, such as monthly subscription fees, set up memorized transactions to reduce manual input errors. Additionally, regularly reconcile accounts—ideally monthly—to catch issues before they compound. By treating each discrepancy as a puzzle to solve, you’ll maintain clean financial records and avoid costly mistakes.

Securely Accessing Your Hidden Bank Account: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Adjust Entries: Record missing transactions, corrections, or bank fees in QuickBooks as needed

During the bank reconciliation process in QuickBooks, discrepancies often arise due to missing transactions, errors, or unrecorded bank fees. These discrepancies can skew your financial records, leading to inaccurate reporting and decision-making. Adjusting entries is a critical step to ensure your books align with your bank statement. Start by identifying the source of the discrepancy—whether it’s an uncleared check, an unrecorded deposit, or a bank fee that hasn’t been accounted for. QuickBooks allows you to manually input these adjustments directly within the reconciliation tool, ensuring your records remain accurate and up-to-date.

To record missing transactions, navigate to the "Add" or "Adjust" button within the reconciliation window. For example, if a deposit appears on your bank statement but isn’t in QuickBooks, enter the transaction details, including the date, amount, and account affected. Similarly, if a bank fee has been deducted but isn’t reflected in your books, create an expense transaction and categorize it appropriately, such as "Bank Service Charges." Be meticulous with dates and amounts to maintain consistency between your bank statement and QuickBooks records.

Corrections are equally important, as errors in previously recorded transactions can throw off your reconciliation. Suppose a payment was entered with the wrong amount or assigned to the incorrect account. In that case, you can adjust the entry directly during reconciliation. QuickBooks allows you to modify existing transactions or create offsetting entries to correct the mistake. For instance, if a $500 payment was mistakenly recorded as $50, create an adjusting journal entry to debit the correct account for the remaining $450 and credit the bank account to balance the entry.

Practical tips can streamline this process. Always double-check the transaction details before finalizing adjustments to avoid compounding errors. Use the memo field to document the reason for the adjustment, such as "Correcting duplicate entry" or "Recording missed bank fee." Additionally, reconcile frequently—ideally monthly—to catch discrepancies early and reduce the complexity of adjustments. If you’re unsure about an entry, consult your bank statement or reach out to your financial institution for clarification before making changes.

In conclusion, adjusting entries in QuickBooks is a precise yet straightforward process that ensures your financial records remain accurate. By systematically recording missing transactions, correcting errors, and accounting for bank fees, you maintain the integrity of your reconciliation. This step not only aligns your books with your bank statement but also provides a clear financial snapshot, enabling informed business decisions. Master this process, and you’ll transform reconciliation from a daunting task into a routine practice that strengthens your financial management.

Key Bank Savings Bonds: Cashing In Made Easy or Not?

You may want to see also

Explore related products

![Quick Books Desktop Pro Plus 2024 | LIFETIME Version | USB | Only for Mac [software_key_card]](https://m.media-amazon.com/images/I/41xG2aOWLLL._AC_UL320_.jpg)

![]()

Finalize Reconciliation: Confirm all discrepancies are resolved and mark the reconciliation as complete

Before marking a bank reconciliation as complete in QuickBooks, it’s critical to ensure every discrepancy has been addressed. Unresolved differences, no matter how small, can snowball into larger financial inaccuracies. QuickBooks flags discrepancies during the reconciliation process, such as uncleared transactions or unmatched amounts. These must be investigated and corrected by either matching them to existing entries, adding missing transactions, or adjusting for errors like duplicate entries or incorrect amounts. Failing to resolve these issues can lead to misstated financial reports, which undermines the integrity of your accounting records.

The final step in QuickBooks involves reviewing the reconciliation summary report. This report provides a detailed breakdown of cleared and uncleared transactions, as well as the beginning and ending balances. Scrutinize this report to confirm that the ending balance matches your bank statement exactly. If discrepancies persist, QuickBooks allows you to make adjusting entries directly from the reconciliation screen. For instance, if a transaction was entered with the wrong date or amount, you can edit it on the spot. Once all items align, QuickBooks prompts you to mark the reconciliation as complete, ensuring the system recognizes the process as finalized.

A common pitfall at this stage is prematurely marking the reconciliation as complete without thoroughly verifying every item. To avoid this, adopt a systematic approach: cross-reference each transaction with your bank statement, double-check calculations, and ensure all adjustments are accurate. For businesses with high transaction volumes, consider using QuickBooks’ search and filter tools to isolate specific entries for review. Additionally, if discrepancies involve transactions that haven’t yet cleared, make a note in QuickBooks to follow up on them in the next reconciliation cycle. This ensures nothing slips through the cracks.

Marking the reconciliation as complete in QuickBooks isn’t just a procedural step—it’s a declaration that your books accurately reflect your bank activity. Once finalized, QuickBooks locks the reconciled transactions to prevent accidental edits, which helps maintain data integrity. However, if errors are discovered post-reconciliation, QuickBooks allows you to undo the process, make corrections, and re-reconcile. This flexibility underscores the importance of accuracy during the finalization phase. By taking the time to confirm all discrepancies are resolved, you ensure your financial records remain reliable and audit-ready.

Discover Online Banking Review: Features, Benefits, and User Experience

You may want to see also

Frequently asked questions

The first step is to access the Reconcile tool in QuickBooks. Go to the Banking menu, select the account you want to reconcile, and click Reconcile Now. Enter the ending balance and ending date from your bank statement to begin the process.

To match transactions, compare the transactions listed in QuickBooks with those on your bank statement. Check the box next to each transaction in QuickBooks that appears on the statement. Unmatched transactions may require further investigation or manual entry.

![QuickBooks Online for Beginners Bible Edition [2 Books in 1]: The Ultimate Fast Learning Guide for QBO, filled with Step-by-Step Illustrated Explanations, Practical Examples and Common Problem Solving](https://m.media-amazon.com/images/I/61WWhskpzAL._AC_UL320_.jpg)