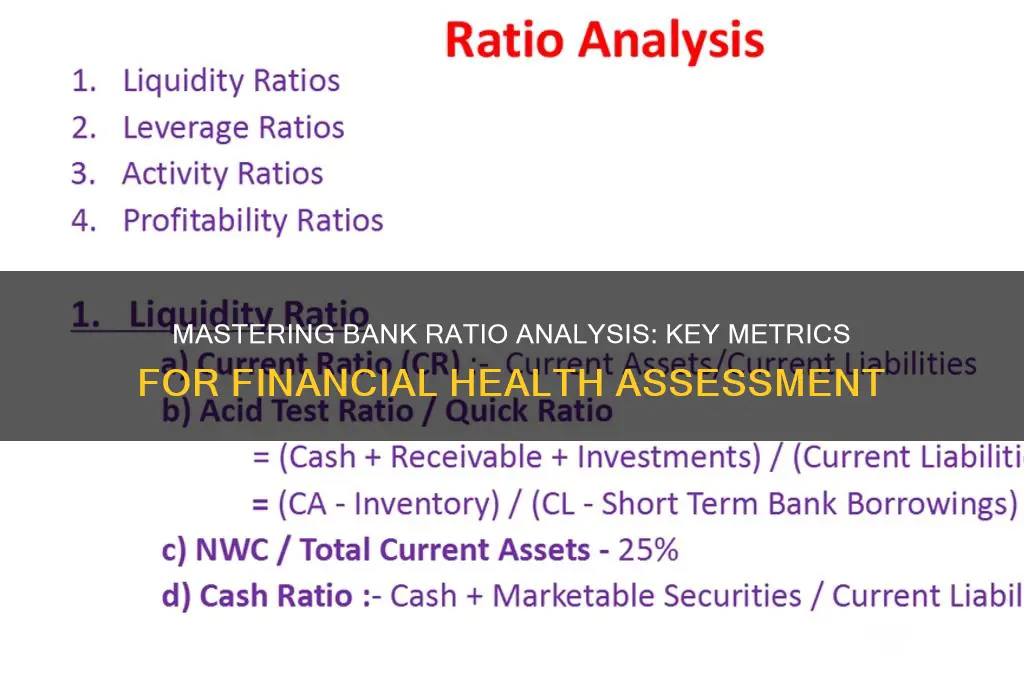

Ratio analysis is a critical tool for evaluating the financial health and performance of banks, providing insights into their liquidity, solvency, efficiency, and profitability. By examining key financial ratios such as the capital adequacy ratio, net interest margin, return on assets, and loan-to-deposit ratio, analysts can assess a bank's ability to manage risk, generate returns, and maintain stability. Understanding these ratios helps stakeholders, including investors, regulators, and management, make informed decisions by comparing a bank's performance against industry benchmarks and identifying potential areas of concern or opportunity. This analysis is particularly important in the banking sector, where financial stability and prudent risk management are paramount.

Explore related products

![The Analysis of Financial Statements, by A.M. Sakolski 1923 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

- Liquidity Ratios: Assess bank's ability to meet short-term obligations (e.g., Current Ratio, Quick Ratio)

- Solvency Ratios: Evaluate long-term financial stability (e.g., Debt-to-Equity, Equity Multiplier)

- Profitability Ratios: Measure efficiency and earnings (e.g., ROA, ROE, Net Interest Margin)

- Efficiency Ratios: Analyze operational performance (e.g., Cost-to-Income Ratio, Asset Turnover)

- Asset Quality Ratios: Assess loan portfolio health (e.g., Non-Performing Loans Ratio, Coverage Ratio)

![]()

Liquidity Ratios: Assess bank's ability to meet short-term obligations (e.g., Current Ratio, Quick Ratio)

Liquidity ratios are a critical tool for evaluating a bank's ability to honor its short-term commitments without facing financial distress. Among these, the Current Ratio and Quick Ratio stand out as key metrics. The Current Ratio, calculated by dividing current assets by current liabilities, provides a snapshot of a bank’s ability to cover short-term obligations with its most liquid assets. A ratio above 1 indicates sufficient liquidity, but in banking, where liabilities often exceed assets, the threshold is typically lower, often around 0.8 to 1.0. However, this ratio includes illiquid assets like inventory (if applicable), which may not be readily convertible to cash, making it less precise for banks.

The Quick Ratio addresses this limitation by excluding inventory and other less liquid assets, focusing solely on cash, marketable securities, and accounts receivable. It is calculated as (Cash + Marketable Securities + Receivables) / Current Liabilities. For banks, this ratio is more relevant because it reflects the immediate liquidity available to meet obligations. A Quick Ratio of 0.5 or higher is generally considered healthy, though this can vary based on the bank’s business model and regulatory environment. For instance, banks with a larger retail deposit base may operate comfortably at lower ratios due to stable funding sources.

While these ratios are essential, their interpretation requires context. A bank with a high liquidity ratio might appear stable, but it could also indicate underutilized assets or excessive cash reserves, potentially signaling inefficiency. Conversely, a low ratio might suggest operational efficiency but could also expose the bank to liquidity risk during market stress. For example, during the 2008 financial crisis, banks with seemingly adequate liquidity ratios faced severe cash shortages due to sudden deposit withdrawals and frozen credit markets. This highlights the need to complement ratio analysis with stress testing and scenario analysis.

To effectively use liquidity ratios, analysts should compare them across time periods and against industry benchmarks. A declining trend in liquidity ratios could signal emerging liquidity issues, while a sudden spike might indicate defensive positioning in anticipation of market volatility. Additionally, regulatory requirements, such as the Liquidity Coverage Ratio (LCR) mandated by Basel III, provide a standardized framework for assessing liquidity risk. Banks must maintain high-quality liquid assets sufficient to cover 30 days of net cash outflows under stress scenarios, offering a more dynamic perspective than traditional ratios alone.

In practice, liquidity ratio analysis should be part of a broader toolkit. For instance, a bank with a Quick Ratio of 0.6 might appear borderline, but if it has access to a central bank’s discount window or maintains a diversified funding base, its liquidity position could be stronger than the ratio suggests. Conversely, reliance on volatile funding sources, such as wholesale deposits, could undermine even a high liquidity ratio. By integrating liquidity ratios with qualitative factors like funding stability, asset quality, and market access, analysts can paint a more accurate picture of a bank’s short-term financial health.

Down Payments: Do Banks Still Require 20 Percent?

You may want to see also

Explore related products

![]()

Solvency Ratios: Evaluate long-term financial stability (e.g., Debt-to-Equity, Equity Multiplier)

Solvency ratios are the cornerstone of assessing a bank's ability to meet long-term obligations, offering a snapshot of its financial stability. Among these, the Debt-to-Equity (D/E) ratio stands out as a critical metric. Calculated by dividing total liabilities by shareholders’ equity, it reveals how much debt is used to finance a bank’s assets relative to equity. A D/E ratio of 3:1, for instance, indicates that for every $3 of debt, there is $1 of equity. While a lower ratio suggests a safer financial position, banks often operate with higher leverage due to their business model. However, a ratio exceeding industry benchmarks (typically 5:1 to 8:1 for banks) may signal excessive risk, especially during economic downturns.

Another vital solvency ratio is the Equity Multiplier, derived by dividing total assets by total equity. This metric highlights how much of a bank’s assets are financed by equity versus debt. For example, an equity multiplier of 5 implies that for every $1 of equity, the bank holds $5 in assets. While a higher multiplier can indicate efficient use of equity, it also amplifies financial risk, as losses are magnified for equity holders. Investors and regulators often scrutinize this ratio to gauge a bank’s capital structure and resilience against shocks.

To effectively use these ratios, compare them against industry averages and historical trends. For instance, a bank with a D/E ratio of 6:1 in a sector where the average is 7:1 may appear less risky, but if its ratio has been climbing steadily over the past three years, it could indicate growing dependency on debt. Similarly, an equity multiplier of 8, while higher than the sector average of 6, might be acceptable if the bank maintains robust profitability and liquidity. Context is key—what’s alarming in one scenario may be prudent in another.

Practical tips for analysts: Always pair solvency ratios with liquidity and profitability metrics for a holistic view. For example, a high D/E ratio paired with strong net interest margins may be sustainable, but if liquidity ratios like the Current Ratio are low, the bank could face short-term funding pressures. Additionally, consider macroeconomic factors—rising interest rates can inflate debt servicing costs, making high D/E ratios more dangerous. Tools like sensitivity analysis can help assess how solvency ratios might shift under different economic scenarios.

In conclusion, solvency ratios are not just numbers but narratives of a bank’s financial strategy and resilience. By dissecting metrics like Debt-to-Equity and Equity Multiplier, stakeholders can identify red flags or opportunities. However, their true value lies in interpretation—understanding the story behind the ratios, not just their face value. For banks, maintaining a balanced capital structure isn’t just about meeting regulatory requirements; it’s about fostering trust and ensuring long-term survival in an unpredictable financial landscape.

Do Banks Charge for Coin Rolls? Uncovering Hidden Fees

You may want to see also

Explore related products

$21.39 $22.95

![]()

Profitability Ratios: Measure efficiency and earnings (e.g., ROA, ROE, Net Interest Margin)

Bank profitability ratios are the financial world's equivalent of a report card, revealing how effectively an institution generates earnings from its assets, equity, and core operations. Among these, Return on Assets (ROA) stands as a cornerstone metric. Calculated by dividing net income by total assets, ROA expresses profitability as a percentage of a bank’s asset base. For instance, a bank with a 1.2% ROA is earning $1.20 for every $100 in assets. Benchmarking is critical here: the average ROA for U.S. banks hovers around 1%, so anything above signals superior asset utilization, while below indicates inefficiency or excessive cost structures.

While ROA focuses on asset efficiency, Return on Equity (ROE) shifts the lens to shareholder returns. Derived by dividing net income by shareholders’ equity, ROE measures how much profit a bank generates with the money shareholders have invested. A common rule of thumb is that ROE should exceed the bank’s cost of equity (typically 8–12%). However, beware of artificially inflated ROE due to excessive leverage—a DuPont analysis (breaking ROE into profit margin, asset turnover, and equity multiplier) can uncover whether high ROE stems from operational efficiency or financial risk-taking.

Net Interest Margin (NIM) drills deeper into a bank’s core revenue engine: the interest earned on loans and securities minus interest paid on deposits, relative to interest-earning assets. In a low-rate environment, NIMs often compress, squeezing profitability. For example, a bank with a 3% NIM earns $3 for every $100 in interest-earning assets. Regional banks typically target NIMs between 3–4%, while larger institutions may settle for 2–3% due to higher funding costs. Monitoring NIM trends over time reveals a bank’s ability to manage interest rate risk and pricing strategies.

To wield these ratios effectively, compare them across time periods, peer institutions, and industry benchmarks. For instance, a bank with a declining ROA paired with stable ROE may signal asset quality issues rather than equity mismanagement. Similarly, a widening NIM during a rate hike cycle could indicate strong loan repricing power. However, no single ratio tells the full story—cross-referencing profitability metrics with liquidity (e.g., loan-to-deposit ratio) and risk (e.g., non-performing loans) ratios provides a holistic view.

In practice, investors and analysts should prioritize consistency over extremes. A bank with ROA fluctuating between 0.8–1.2% is likely more stable than one jumping from 0.5% to 2%. For banks, maintaining a balanced scorecard—optimizing ROA without sacrificing NIM or ROE—is key. Tools like stress testing (e.g., how NIM would fare in a 200bps rate hike) further sharpen insights. Ultimately, profitability ratios are not just numbers but narratives of strategic choices, market positioning, and operational discipline.

New Deal's Impact: Transforming Banking Stability and Regulation

You may want to see also

Explore related products

![]()

Efficiency Ratios: Analyze operational performance (e.g., Cost-to-Income Ratio, Asset Turnover)

Efficiency ratios are the financial world's equivalent of a stopwatch, timing how swiftly and leanly a bank operates. Among these, the Cost-to-Income Ratio (CIR) stands out as a critical metric. Calculated by dividing operating expenses by operating income, it reveals how much a bank spends to earn each dollar of revenue. A CIR below 50% is often considered efficient, indicating that less than half of income is consumed by costs. For instance, if Bank A reports operating expenses of $60 million and operating income of $150 million, its CIR is 40%—a healthy sign of cost management. However, this ratio must be contextualized; investment banks, with their higher operational complexity, may naturally have a higher CIR than retail banks.

While CIR focuses on expense management, Asset Turnover Ratio shifts the lens to revenue generation from assets. It measures how efficiently a bank uses its assets to produce income, calculated as total revenue divided by average total assets. A higher ratio suggests better asset utilization. Consider Bank B, with $1 billion in assets and $200 million in revenue, yielding an asset turnover ratio of 0.2. Compared to Bank C, with similar assets but $250 million in revenue (ratio of 0.25), Bank C is more efficient in leveraging its assets. However, this ratio can be skewed in banks with low-margin, high-volume businesses, so it’s crucial to pair it with profitability metrics for a balanced view.

Analyzing these ratios in tandem provides a dual perspective on operational performance. For example, a bank with a low CIR but mediocre asset turnover might excel in cost control but underperform in revenue generation. Conversely, a bank with high asset turnover and a high CIR could be over-extending resources to chase revenue. Investors and analysts should also track trends over time; a steadily improving CIR or asset turnover signals operational discipline, while sudden spikes or drops warrant deeper investigation into underlying causes, such as mergers, technological investments, or market shifts.

Practical application of efficiency ratios requires caution. Banks often have diverse business lines, and aggregating data can mask inefficiencies in specific segments. For instance, a retail banking division might subsidize the CIR of a struggling investment arm. Additionally, accounting practices can distort these ratios—deferred expenses or revenue recognition policies may artificially inflate or deflate results. To mitigate this, analysts should scrutinize footnotes and management discussions in financial reports, ensuring apples-to-apples comparisons across institutions.

In conclusion, efficiency ratios are indispensable tools for dissecting a bank’s operational health, but they are not foolproof. By focusing on CIR and asset turnover, stakeholders can gauge cost management and asset utilization, yet these metrics must be interpreted within the bank’s strategic context and industry benchmarks. Pairing them with qualitative insights—such as technological investments or organizational restructuring—provides a more holistic view. Ultimately, efficiency ratios are not just numbers; they are narratives of how well a bank balances frugality with growth, offering actionable intelligence for decision-makers.

How Hackers Steal Your Bank Information: Tactics and Prevention Tips

You may want to see also

Explore related products

![]()

Asset Quality Ratios: Assess loan portfolio health (e.g., Non-Performing Loans Ratio, Coverage Ratio)

Asset quality ratios are the pulse check of a bank's loan portfolio, revealing the health of its lending practices and the potential risks lurking beneath the surface. Among these, the Non-Performing Loans (NPL) Ratio stands out as a critical indicator. Calculated by dividing the total non-performing loans by the total gross loans, this ratio highlights the percentage of loans that are in default or close to it. A high NPL ratio, say above 3%, often signals poor credit risk management or economic distress, while a lower ratio, around 1-2%, suggests a more robust and prudent lending strategy. For instance, during the 2008 financial crisis, banks with NPL ratios exceeding 5% faced severe liquidity issues, underscoring the ratio's predictive power.

While the NPL ratio diagnoses the problem, the Coverage Ratio prescribes the solution. This metric, derived by dividing loan loss reserves by non-performing loans, measures a bank's preparedness to absorb potential losses. A coverage ratio below 100% indicates insufficient reserves, leaving the bank vulnerable to loan defaults. Conversely, a ratio above 120% reflects a conservative approach, ensuring the bank can weather unexpected defaults. For example, a bank with a coverage ratio of 150% is better positioned to handle a sudden rise in NPLs compared to one with a 70% ratio. However, excessively high reserves can tie up capital, limiting lending opportunities and profitability.

To effectively use these ratios, analysts must consider industry benchmarks and economic conditions. For instance, banks operating in emerging markets often exhibit higher NPL ratios due to volatile economic environments, while those in stable economies maintain lower ratios. Pairing these ratios with stress testing can provide a more dynamic assessment, simulating how the portfolio might perform under adverse scenarios. For practical application, start by benchmarking the bank's NPL and coverage ratios against peers and historical data. If the NPL ratio is rising, investigate the sectors or regions contributing to the increase. Simultaneously, ensure the coverage ratio aligns with the risk profile, adjusting reserves if necessary.

A common pitfall is focusing solely on these ratios without examining underlying trends. For example, a declining NPL ratio might seem positive but could mask aggressive loan restructuring or write-offs. Cross-referencing with other metrics, such as loan growth rates and provisioning trends, provides a more holistic view. Additionally, regulatory changes, like Basel III, have tightened provisioning requirements, making historical comparisons less straightforward. Analysts should stay updated on such changes to interpret ratios accurately.

In conclusion, asset quality ratios are indispensable tools for assessing a bank's loan portfolio health. By meticulously analyzing the NPL and coverage ratios, stakeholders can identify risks, evaluate preparedness, and make informed decisions. However, these ratios are not standalone metrics; they require context, benchmarking, and complementary analysis to paint a complete picture. Whether you're an investor, regulator, or bank executive, mastering these ratios ensures a clearer understanding of the bank's financial stability and resilience.

Corporate Finance Strategies: Boosting Bank Performance and Stability

You may want to see also

Frequently asked questions

Ratio analysis is a financial tool used to evaluate a bank's performance, liquidity, solvency, and efficiency by comparing key financial metrics. It is important because it helps stakeholders assess the bank's financial health, risk management, and profitability, enabling informed decision-making.

Key liquidity ratios include the Current Ratio (Current Assets / Current Liabilities) and the Liquid Assets to Deposits Ratio (Liquid Assets / Total Deposits). These ratios measure a bank's ability to meet short-term obligations and manage deposit outflows.

Profitability ratios such as Return on Assets (ROA) (Net Income / Total Assets) and Return on Equity (ROE) (Net Income / Shareholders' Equity) are used to evaluate how effectively a bank generates profits from its assets and equity.

Solvency and capital adequacy are assessed using ratios like the Debt-to-Equity Ratio (Total Liabilities / Shareholders' Equity) and the Capital Adequacy Ratio (CAR) (Tier 1 + Tier 2 Capital / Risk-Weighted Assets). CAR is particularly critical as it ensures the bank meets regulatory requirements.

Efficiency ratios like the Cost-to-Income Ratio (Operating Expenses / Operating Income) and the Non-Interest Expense to Total Assets Ratio measure how well a bank manages its costs relative to its revenue and assets. Lower ratios indicate better operational efficiency.