Looking at old bank transactions can be a useful way to track spending habits, verify past payments, or reconcile financial records. Most banks provide access to historical statements through online banking platforms, where customers can typically view transactions dating back several months or even years, depending on the institution’s policies. For older records that are no longer available online, individuals can request archived statements directly from their bank, often for a small fee. Additionally, maintaining personal financial records, such as downloaded statements or transaction exports, can simplify the process of reviewing past activity. Understanding how to access and interpret old bank transactions is essential for financial management and ensuring accuracy in personal or business accounts.

| Characteristics | Values |

|---|---|

| Online Banking Portal | Log in to your bank's website or mobile app. |

| Statement Period Selection | Choose the desired date range or specific month/year for transactions. |

| Transaction History Section | Navigate to "Transaction History," "Statements," or similar sections. |

| Downloadable Statements | Download PDF or CSV files of past statements for offline access. |

| Search Filters | Use filters (date, amount, merchant, etc.) to locate specific transactions. |

| Paper Statements | Request physical copies of old statements from your bank (may incur fees). |

| Customer Service | Contact your bank via phone, email, or chat for assistance. |

| Archived Records | Access archived records if transactions are older than the default display period. |

| Third-Party Tools | Use budgeting apps (e.g., Mint, YNAB) linked to your account for historical data. |

| Security Measures | Ensure secure login and avoid sharing credentials to protect your data. |

| Retention Period | Banks typically retain transaction records for 5–7 years (varies by institution). |

| Fees for Old Records | Some banks charge fees for accessing or retrieving very old transactions. |

Explore related products

$189 $199.99

What You'll Learn

![]()

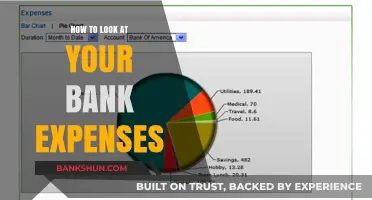

Accessing online banking archives

Online banking archives are a treasure trove of financial history, but accessing them requires navigating a maze of security protocols and interface quirks. Most banks retain transaction records for at least seven years, though some extend this to ten or more. To begin, log into your online banking account and locate the "Statements" or "Transaction History" section, typically found under "Accounts" or "Documents." If the default view only shows recent activity, look for a dropdown menu or calendar tool to specify a broader date range. Some banks limit online access to the past 12–24 months, so for older records, you may need to request archived statements. These are often downloadable as PDFs, though fees may apply for physical copies.

The process varies widely across institutions, reflecting differences in technology and policy. For instance, Chase allows users to view up to 7 years of statements online, while Bank of America provides access to 18 months by default, requiring a manual request for older records. Credit unions often have more limited digital archives, sometimes only 12 months, due to smaller IT budgets. A workaround for restricted access is to export monthly transactions into a spreadsheet periodically, creating a personal archive. This not only ensures continuity but also simplifies tax preparation and budgeting. However, be mindful of data security when storing financial files locally or in the cloud.

Persuasively, leveraging online archives is more than a convenience—it’s a financial hygiene practice. Regularly reviewing old transactions can uncover errors, unauthorized charges, or forgotten subscriptions. For example, a 2022 study found that 32% of consumers discovered discrepancies in their accounts by scrutinizing past statements. Moreover, historical data is invaluable for loan applications, where lenders often request 2–3 years of bank statements. Proactively accessing and organizing this information positions you as a prepared borrower or taxpayer, reducing stress during critical financial moments.

Comparatively, while online archives are efficient, they’re not infallible. Digital records can be lost due to system upgrades or account closures, unlike physical statements. For long-term preservation, consider printing or saving key statements annually, especially those tied to major purchases or tax deductions. Additionally, older adults or those less tech-savvy may find the process daunting, making it advisable to seek assistance from a trusted family member or banker. Balancing digital convenience with tangible backups ensures both accessibility and durability.

Descriptively, the experience of sifting through online archives can feel like time travel, each transaction a snapshot of past priorities. A $500 charge to a hardware store in 2018 might remind you of a DIY project, while recurring $30 payments to a gym highlight a forgotten membership. This narrative aspect of financial history can be both enlightening and motivating, offering insights into spending habits and life milestones. By mastering the tools to access these records, you transform raw data into a story of financial evolution, one transaction at a time.

Effective Strategies to Clear a Bank of Weeds Permanently

You may want to see also

Explore related products

![]()

Requesting historical statements from the bank

Banks typically retain transaction records for several years, but accessing historical statements often requires a formal request. This process varies by institution, so start by checking your bank’s website or mobile app. Many banks allow customers to download statements for the past 12–24 months directly from their online portal. For older records, you’ll likely need to contact customer service. Understanding these timelines and channels is the first step to retrieving your financial history efficiently.

When requesting historical statements, be prepared to provide specific details to expedite the process. Include the account number, the exact date range of the statements you need, and your preferred delivery method (e.g., email, mail, or in-person pickup). Some banks may charge a fee for this service, especially for records older than 7 years, so inquire about costs upfront. Clear communication ensures you receive the correct documents without unnecessary delays or expenses.

A comparative analysis reveals that digital-first banks often offer more seamless access to historical statements than traditional brick-and-mortar institutions. For instance, online banks like Ally or Chime frequently provide unlimited statement downloads from their platforms, while regional banks may require written requests or in-branch visits. If convenience is a priority, consider consolidating accounts with banks that prioritize digital accessibility for long-term financial management.

Persuasively, requesting historical statements isn’t just about nostalgia—it’s a practical tool for financial health. These documents are essential for tax audits, loan applications, or resolving discrepancies. For example, if you’re disputing a charge from years ago, a statement serves as irrefutable proof. Treat these records as a financial archive, storing them securely in digital or physical form for future reference. Proactive record-keeping today prevents headaches tomorrow.

Finally, a descriptive tip: if your bank’s process feels cumbersome, explore third-party solutions like budgeting apps that sync with your accounts and retain transaction history indefinitely. Tools like Mint or YNAB aggregate data across accounts, providing a centralized archive. While not official bank statements, they offer a user-friendly alternative for tracking spending patterns over time. Pairing these apps with periodic bank statement downloads creates a robust system for managing your financial past and present.

BBVA Bank's ATM Policy: Are Withdrawals Free for Customers?

You may want to see also

Explore related products

![]()

Using mobile app transaction history features

Mobile banking apps have revolutionized the way we manage our finances, offering a convenient and efficient method to access transaction history. With just a few taps, users can delve into their financial past, a feature particularly useful for those seeking to review old bank transactions. This functionality is not merely a digital luxury but a powerful tool for financial management, enabling users to track spending, identify trends, and even dispute charges.

Navigating the Transaction Timeline

Most banking apps provide a user-friendly interface to explore transaction history. Typically, users can access this feature by logging into their account and locating the 'Transactions' or 'Activity' tab. Here, a chronological list of transactions unfolds, often with customizable date ranges. For instance, users can filter transactions from the past month, quarter, or even year, allowing for a tailored review. This level of detail is invaluable for those trying to recall specific purchases or payments made months ago.

Search and Filter Functions: Uncovering Specific Transactions

The true power of mobile app transaction history lies in its search and filter capabilities. Users can often search for transactions using keywords, amounts, or merchant names. For example, searching for 'groceries' might reveal all transactions at supermarkets, helping users analyze their food spending. Some apps even allow filtering by transaction type, such as purchases, transfers, or direct deposits, providing a more nuanced view of financial activity. This level of specificity is particularly beneficial for budgeting and expense tracking.

Security and Accessibility: A Delicate Balance

While the convenience of mobile transaction history is undeniable, it raises important security considerations. Banks employ various measures to protect user data, including encryption and two-factor authentication. Users should ensure their devices are secure and be cautious when accessing sensitive information in public spaces. Additionally, regular password updates and monitoring for suspicious activity are essential practices. Despite these precautions, the accessibility of transaction history on mobile devices empowers users to take control of their financial oversight.

Practical Tips for Effective Transaction Review

To maximize the benefits of mobile transaction history, users can adopt several strategies. Firstly, regular reviews can help identify errors or fraudulent activity promptly. Setting reminders to check transactions weekly or monthly can be beneficial. Secondly, utilizing the app's categorization features can provide insights into spending habits. Many apps automatically categorize transactions, making it easier to understand where money is being spent. Lastly, exporting transaction data for further analysis in spreadsheet software can be a powerful tool for detailed financial planning. This approach is especially useful for those managing complex budgets or small business finances.

In the digital age, the ability to access and analyze old bank transactions via mobile apps is a significant advantage for personal financial management. It offers a level of detail and convenience that traditional methods cannot match, empowering users to make informed decisions about their money. By understanding and utilizing these features effectively, individuals can take a proactive approach to their financial health.

Exploring the Vast Network of Bank Offices Across the United States

You may want to see also

Explore related products

![The Wes Anderson Archive: Ten Films, Twenty-Five Years (The Criterion Collection) [4K UHD]](https://m.media-amazon.com/images/I/71mKRS+vs4L._AC_UY218_.jpg)

$249.98 $349.99

![]()

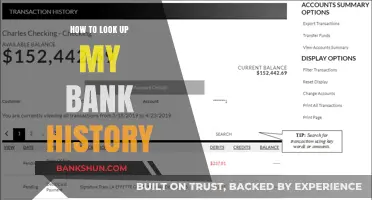

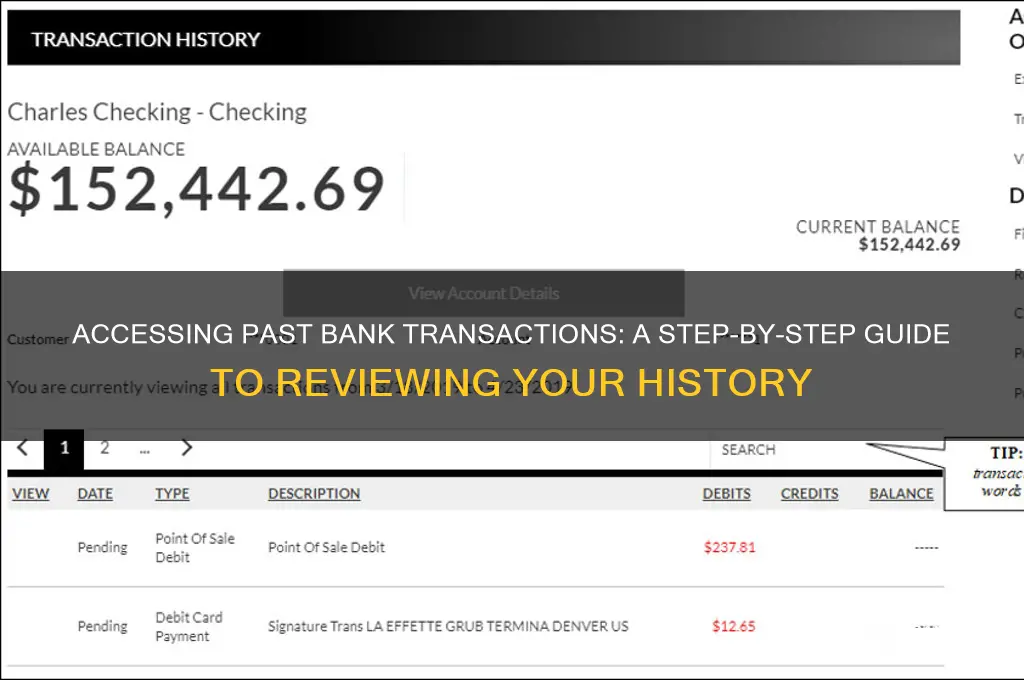

Reviewing downloaded bank statement PDFs

Bank statements are treasure troves of financial history, but downloaded PDFs can feel like cluttered maps. To navigate effectively, start by understanding the document's structure. Most statements follow a consistent layout: account summary at the top, followed by transaction details categorized by date, type, and amount. Look for headings like "Debit," "Credit," or "Description" to identify key columns. Some banks include running balances, a crucial tool for tracking your account's trajectory over time.

Recognizing these patterns transforms a jumble of numbers into a comprehensible narrative of your financial activity.

Once you've deciphered the layout, employ search functions to pinpoint specific transactions. Most PDF viewers allow keyword searches, enabling you as to locate purchases from a particular store, recurring bills, or transactions within a specific date range. This targeted approach saves time and frustration, especially when dealing with lengthy statements. For example, searching for "Amazon" will highlight all purchases made on that platform, allowing you to quickly verify their accuracy.

Beyond basic searches, consider utilizing third-party tools for deeper analysis. Software like Adobe Acrobat Pro offers advanced features like text recognition and data extraction, allowing you to export transaction data into spreadsheets for further manipulation. This is particularly useful for budgeting, tax preparation, or identifying spending patterns over time. Imagine comparing monthly grocery expenses or tracking the growth of your savings – these insights become achievable with the right tools.

While these tools require an investment, they can significantly enhance your ability to extract meaningful information from your bank statement PDFs.

Remember, reviewing old bank statements isn't just about nostalgia; it's about financial responsibility and empowerment. By mastering the art of navigating downloaded PDFs, you gain a clearer understanding of your spending habits, identify potential errors, and make informed decisions about your financial future. So, don't let those digital documents gather virtual dust – unlock their potential and take control of your financial story.

Guarantor's Bank Details: When and Why They're Needed

You may want to see also

Explore related products

![Archive [Blu-ray] [2020]](https://m.media-amazon.com/images/I/510hdvFWzPL._AC_UY218_.jpg)

![]()

Contacting customer service for old records

Banks typically retain transaction records for a minimum of five years, but accessing older statements often requires direct intervention from customer service. This is because digital archives may only store the most recent 12 to 24 months of activity, with older data archived offline or in less accessible formats. If you need records beyond this window—whether for tax purposes, legal disputes, or personal financial analysis—contacting customer service is your most reliable option. Start by gathering your account details, including the account number, period of interest, and any relevant transaction specifics, to streamline the process.

When reaching out, choose the communication channel that aligns with your urgency and the bank’s capabilities. Most banks offer phone support, which is ideal for immediate assistance, though wait times can vary. Email or secure messaging through online banking portals provide a written record of your request but may take 2–5 business days for a response. For older records, some banks may require a formal written request sent via mail, particularly for accounts closed more than a decade ago. Always confirm the bank’s preferred method and any associated fees, as some institutions charge for retrieving archived statements.

Persuasion plays a key role in expediting your request. Clearly articulate the purpose of your inquiry, whether it’s for a mortgage application, audit, or personal record-keeping. Banks are more likely to prioritize requests tied to official needs, especially if you mention deadlines. For instance, stating, “I need these records by [date] for a tax audit,” can prompt faster action. Additionally, remain polite but persistent; if initial responses are unhelpful, escalate the request to a supervisor or use the bank’s social media channels for public accountability.

Comparing this approach to self-service options highlights its advantages and drawbacks. While online banking often allows access to recent statements, older records are rarely available without customer service involvement. Mobile apps, even from major banks, typically limit viewable history to 1–2 years. In contrast, customer service can access archived data but may require more effort and time. For those with closed accounts, this method is often the only viable solution, though it may involve additional verification steps to confirm your identity and account ownership.

To maximize efficiency, prepare for potential hurdles. Banks may request photo ID, account opening documents, or proof of address, especially for accounts inactive for several years. If the records span multiple branches or account types, clarify this in your request to avoid delays. Finally, inquire about the format of the records—whether digital PDFs, physical copies, or microfilm—and any costs involved. While this process may seem cumbersome, it remains the most effective way to retrieve detailed, older bank transactions when other avenues fall short.

Understanding Bank Rolls: How Many Dimes Fit in a Standard Roll?

You may want to see also

Frequently asked questions

Log in to your bank’s online banking portal or mobile app, navigate to the transaction history or statement section, and select the desired date range to view past transactions.

Yes, contact your bank’s customer service or visit a branch to request printed or digital copies of old statements. There may be a fee for this service.

Most banks allow you to view transactions for the past 12–24 months online. For older records, you may need to request archived statements.

Viewing transactions online is usually free, but requesting printed or archived statements may incur a fee, depending on your bank’s policies.

Yes, most online banking platforms allow you to download or print transaction histories or statements in PDF or CSV format for personal records.

![Archive (2020) [ Blu-Ray, Reg.A/B/C Import - Australia ]](https://m.media-amazon.com/images/I/71SvPo86maL._AC_UY218_.jpg)