Measuring corporate governance in banks is critical for ensuring transparency, accountability, and long-term sustainability in the financial sector. Effective corporate governance frameworks help mitigate risks, protect stakeholder interests, and enhance trust in banking institutions. Key metrics for assessing governance include board composition and independence, executive compensation practices, risk management systems, regulatory compliance, and transparency in financial reporting. Tools such as governance ratings, compliance audits, and stakeholder surveys are often employed to evaluate these aspects. Additionally, adherence to international standards like the Basel Committee’s principles and local regulatory guidelines provides a benchmark for measurement. By systematically evaluating these factors, banks can identify governance gaps, implement improvements, and foster a culture of ethical and responsible management.

Explore related products

$28.89 $56.99

$9.95 $24.95

$42.74 $44.99

What You'll Learn

![]()

Board effectiveness metrics

Effective board governance in banks hinges on measurable performance, not just good intentions. Metrics like board composition diversity, meeting attendance rates, and director skill assessments provide quantifiable insights into functionality. For instance, a board with 30% female representation and 25% industry-specific expertise is more likely to foster balanced decision-making than a homogenous group. However, raw numbers alone are insufficient. Contextual analysis is crucial. A 95% attendance rate might seem impressive, but if discussions lack depth or dissent, it signals a deeper issue.

Easy Guide to Installing Simple-Banking QB-Core for Your Server

You may want to see also

Explore related products

![]()

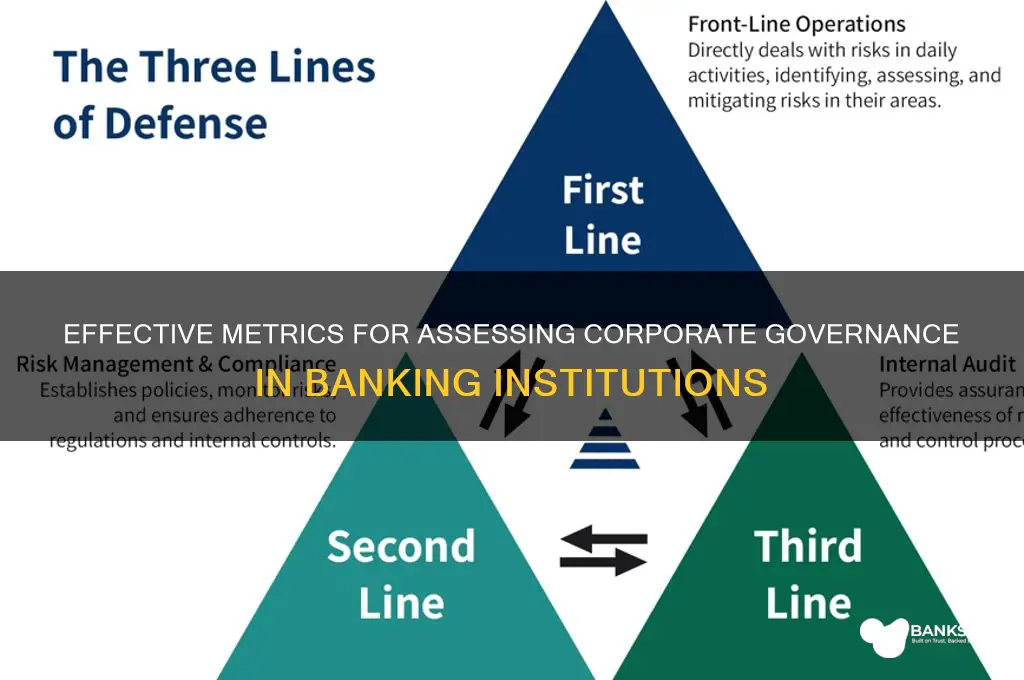

Risk management assessment tools

Effective risk management is the cornerstone of robust corporate governance in banks, and specialized assessment tools are essential for evaluating its efficacy. One widely adopted framework is the Operational Risk Management (ORM) tool, which quantifies risks across operational, credit, market, and liquidity domains. Banks use this tool to identify vulnerabilities, assign risk scores, and prioritize mitigation strategies. For instance, a bank might use ORM to assess the likelihood of a cybersecurity breach, assigning a risk score of 8 out of 10, and then allocate resources to enhance firewalls and employee training. This structured approach ensures risks are not only identified but also systematically addressed.

Another critical tool is the Risk Maturity Model (RMM), which evaluates the maturity of a bank’s risk management processes on a scale of 1 to 5. Level 1 indicates ad-hoc, reactive practices, while Level 5 signifies a fully integrated, proactive risk culture. By benchmarking against this model, banks can identify gaps in their governance frameworks. For example, a bank scoring Level 3 might lack real-time risk monitoring capabilities, prompting investment in advanced analytics tools. The RMM not only provides a diagnostic but also a roadmap for continuous improvement, aligning risk management with strategic goals.

In the realm of credit risk, Credit Risk Assessment Tools (CRATs) are indispensable. These tools use algorithms to analyze borrower creditworthiness, loan portfolio quality, and macroeconomic indicators. A practical example is the use of CRATs to stress-test loan portfolios against economic downturns, ensuring banks maintain adequate capital buffers. For instance, a bank might simulate a 20% decline in property values to assess its exposure to mortgage defaults. Such scenario-based assessments are vital for preempting crises and ensuring compliance with regulatory standards like Basel III.

While these tools are powerful, their effectiveness hinges on data quality and organizational commitment. Inaccurate or incomplete data can skew risk assessments, leading to misguided decisions. For instance, a bank relying on outdated customer financial data might underestimate credit risk, resulting in excessive lending. To mitigate this, banks should invest in data governance frameworks and regularly audit their risk models. Additionally, fostering a risk-aware culture is crucial; employees at all levels must understand their role in risk management, from frontline staff identifying red flags to executives approving mitigation strategies.

In conclusion, risk management assessment tools are not one-size-fits-all solutions but require customization to a bank’s unique context. By leveraging ORM, RMM, CRATs, and ensuring data integrity, banks can build resilient governance frameworks. The ultimate takeaway is that these tools are not just regulatory checkboxes but strategic enablers, driving long-term stability and stakeholder trust.

Step-by-Step Guide to Generating Your State Bank ATM PIN Securely

You may want to see also

Explore related products

![Compliance [Blu-ray]](https://m.media-amazon.com/images/I/712fZO6aOlL._AC_UY218_.jpg)

![Law of Governance, Risk Management and Compliance: [Connected Ebook] (Aspen Casebook)](https://m.media-amazon.com/images/I/616gNHR5shL._AC_UY218_.jpg)

![]()

Transparency and disclosure standards

To implement effective transparency and disclosure standards, banks must adopt a multi-faceted approach. First, establish a clear policy framework that defines what information should be disclosed, to whom, and how frequently. For example, quarterly financial statements, annual sustainability reports, and ad hoc disclosures of material events are standard practices. Second, leverage technology to streamline reporting processes. Tools like blockchain can enhance the integrity and traceability of disclosed data, while data analytics can identify trends and anomalies that require further scrutiny. Third, ensure that disclosures are accessible and understandable to all stakeholders, not just financial experts. Plain language summaries and visual aids can bridge the gap between complex financial data and public comprehension.

A comparative analysis reveals that banks with higher transparency scores often outperform their peers in terms of market valuation and stakeholder trust. For instance, a study by the World Bank found that banks in countries with stringent disclosure requirements had lower funding costs and higher credit ratings. Conversely, institutions that lag in transparency, such as those involved in the 2008 financial crisis, faced severe reputational damage and regulatory penalties. This underscores the direct correlation between transparency and financial stability. Banks that proactively disclose information, even when it reflects challenges, are viewed as more credible and resilient.

However, achieving optimal transparency is not without challenges. Banks must balance the need for disclosure with the protection of proprietary information and client confidentiality. Over-disclosure can expose sensitive data to competitors, while under-disclosure risks non-compliance and mistrust. To navigate this, banks should adopt a risk-based approach, prioritizing the disclosure of information that significantly impacts stakeholders’ decisions. Additionally, boards of directors play a pivotal role in overseeing transparency practices, ensuring that management adheres to both legal requirements and ethical standards. Regular audits and independent reviews can further validate the accuracy and completeness of disclosures.

In conclusion, transparency and disclosure standards are not merely regulatory checkboxes but strategic imperatives for banks. By fostering openness, banks can enhance their credibility, attract investment, and mitigate risks. Practical steps include adopting advanced reporting technologies, ensuring accessibility of disclosures, and maintaining a balance between transparency and confidentiality. As the financial landscape evolves, banks that prioritize these standards will be better positioned to navigate complexities and maintain stakeholder confidence. Transparency is not just a measure of governance—it is a testament to a bank’s commitment to integrity and accountability.

How Banks Are Helping Customers During COVID-19

You may want to see also

Explore related products

![]()

Shareholder rights evaluation methods

Evaluating shareholder rights is a critical aspect of measuring corporate governance in banks, as it directly reflects the balance of power and the protection of investor interests. One effective method is the Shareholder Rights Index (SRI), a quantitative tool developed by organizations like the OECD and the International Corporate Governance Network (ICGN). The SRI assesses the extent to which shareholders can exercise their rights, such as voting, access to information, and participation in key decisions. For instance, banks with high SRI scores often allow electronic voting, provide transparent annual reports, and ensure equal treatment of all shareholders, regardless of stake size. Implementing this index involves benchmarking a bank’s practices against global standards, making it a robust measure of governance quality.

Another practical approach is proxy voting analysis, which examines how banks handle shareholder resolutions and voting processes. This method involves reviewing the frequency and outcomes of shareholder proposals, particularly those related to governance reforms, executive compensation, and sustainability. For example, banks that consistently oppose shareholder-led initiatives or impose restrictive voting procedures may signal weak governance. Conversely, those that actively engage with shareholders and adopt their recommendations demonstrate a commitment to protecting investor rights. Conducting this analysis requires access to proxy statements and voting records, which are typically available in annual reports or through regulatory filings.

A third method is the shareholder activism assessment, which evaluates how banks respond to activist investors. This involves studying cases where shareholders have challenged management decisions or proposed structural changes. Banks with strong governance frameworks often engage constructively with activists, addressing their concerns transparently and implementing viable solutions. For instance, a bank that revises its board composition or dividend policy following shareholder pressure demonstrates responsiveness. However, caution is needed when interpreting activism data, as excessive activism may indicate underlying governance issues rather than shareholder empowerment.

Lastly, survey-based evaluations can provide qualitative insights into shareholder satisfaction and perceived rights protection. These surveys, often conducted by independent research firms or regulatory bodies, gather feedback from institutional and retail investors on their experiences with the bank’s governance practices. Questions may focus on the ease of exercising voting rights, the clarity of corporate disclosures, and the fairness of shareholder meetings. While subjective, this method complements quantitative measures by capturing the human element of governance. For banks, participating in such surveys not only aids in self-assessment but also signals a willingness to improve transparency and accountability.

In conclusion, evaluating shareholder rights requires a multi-faceted approach combining quantitative indices, procedural analyses, case studies, and stakeholder feedback. Each method offers unique insights, and their collective application provides a comprehensive view of a bank’s governance framework. By prioritizing shareholder rights, banks not only enhance their governance but also build trust with investors, which is essential for long-term sustainability and financial stability.

Reviving Foreclosed Homes: A Step-by-Step Guide to Restoring Bank-Owned Properties

You may want to see also

Explore related products

![]()

Regulatory compliance monitoring techniques

Effective regulatory compliance monitoring in banks hinges on a combination of automated tools and human oversight. Advanced technologies like AI and machine learning algorithms can analyze vast datasets to identify anomalies, flag potential violations, and predict compliance risks before they escalate. For instance, natural language processing (NLP) can scrutinize regulatory documents and internal policies to ensure alignment, while robotic process automation (RPA) can streamline repetitive compliance tasks, reducing human error. However, technology alone is insufficient; skilled compliance officers must interpret results, investigate red flags, and adapt strategies to evolving regulations. This dual approach ensures both efficiency and accuracy in monitoring.

A critical technique in regulatory compliance monitoring is the implementation of a risk-based approach. Banks must prioritize areas with the highest compliance risk, such as anti-money laundering (AML) or data privacy, by allocating resources proportionally. For example, a bank operating in multiple jurisdictions should focus on regions with stricter regulatory environments or higher historical non-compliance rates. Key performance indicators (KPIs) like the number of unresolved compliance issues, time to remediation, and frequency of regulatory breaches can help measure effectiveness. Regular risk assessments, conducted at least annually, should inform adjustments to monitoring strategies, ensuring they remain relevant and proactive.

Continuous monitoring, as opposed to periodic audits, is another essential technique. Real-time dashboards and alerts enable banks to detect and address compliance issues as they arise, rather than after they’ve caused damage. For instance, transaction monitoring systems can flag suspicious activities immediately, allowing for swift intervention. This approach not only minimizes regulatory penalties but also protects the bank’s reputation. However, continuous monitoring requires robust data infrastructure and clear protocols for escalation and resolution. Banks should invest in training staff to respond effectively to alerts, ensuring that technology complements, rather than replaces, human judgment.

Benchmarking against industry standards and peer institutions provides a comparative lens for assessing compliance monitoring effectiveness. Banks can use frameworks like the Basel Committee’s Corporate Governance Principles or the COSO model to evaluate their practices against best practices. For example, comparing the frequency of regulatory fines or the speed of compliance issue resolution with industry averages can highlight areas for improvement. Additionally, participating in industry forums or consortia allows banks to share insights and learn from others’ experiences. This external perspective can uncover blind spots and foster a culture of continuous improvement in compliance monitoring.

Finally, stress testing and scenario analysis are underutilized but powerful techniques for regulatory compliance monitoring. By simulating extreme scenarios, such as a sudden change in regulations or a cybersecurity breach, banks can assess the resilience of their compliance frameworks. For instance, a stress test might evaluate how well the bank could adapt to new AML requirements within a tight deadline. These exercises not only identify vulnerabilities but also prepare staff for real-world challenges. Incorporating stress testing into regular compliance activities ensures that banks are not just meeting current standards but are also future-proofed against emerging risks.

Understanding Bank Liquidity: A Step-by-Step Calculation Guide

You may want to see also

Frequently asked questions

Key indicators include board effectiveness, transparency in financial reporting, risk management frameworks, shareholder rights, executive compensation practices, and compliance with regulatory standards. Metrics such as board independence, frequency of audits, and adherence to codes of conduct are also commonly assessed.

Regulatory frameworks, such as Basel III, Sarbanes-Oxley Act, and local banking regulations, provide standardized guidelines and reporting requirements. Compliance with these frameworks is a critical measure of governance, ensuring banks adhere to best practices in risk management, disclosure, and accountability.

Stakeholder perception, including that of shareholders, customers, employees, and regulators, is a qualitative measure of governance. Surveys, ratings from credit agencies, and media sentiment analysis can reflect how well a bank is governed, influencing its reputation and market standing.