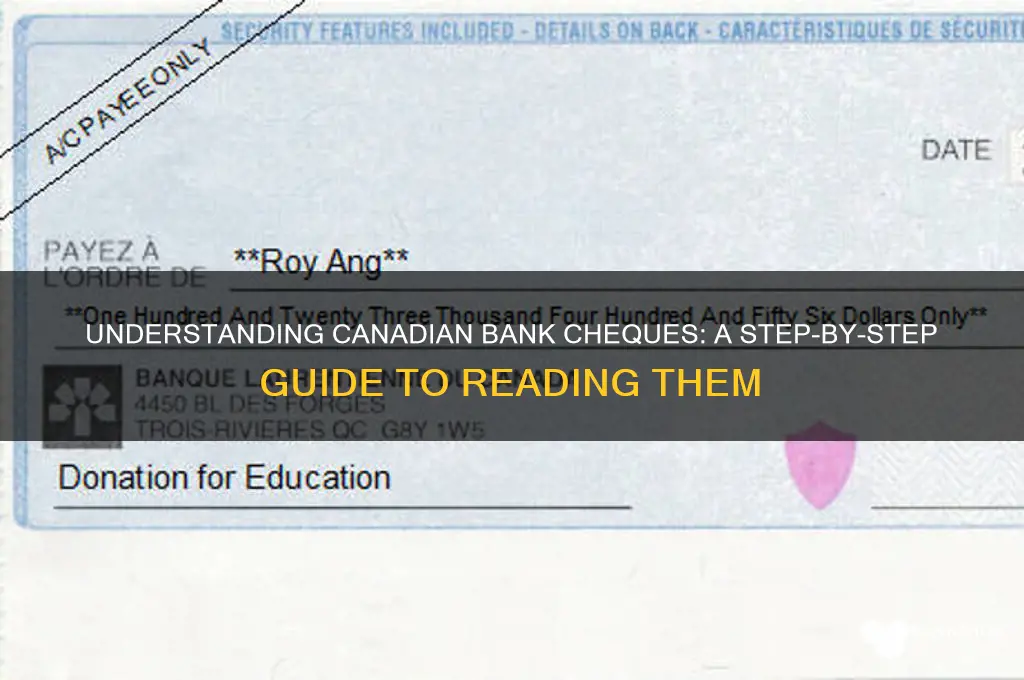

Reading a Canadian bank cheque is essential for understanding its components and ensuring accurate processing. A standard cheque typically includes the payer’s name and address in the top left corner, followed by the cheque number in the top right. The bank’s logo and contact information are usually centered at the top, while the date is written in the top right corner. Below this, the payee’s name is clearly stated, followed by the amount in both numerical and written forms to prevent fraud. The bottom of the cheque contains the magnetic ink character recognition (MICR) line, which includes the bank’s transit number, account number, and cheque number, along with a signature line for authorization. Familiarizing yourself with these elements ensures you can correctly interpret and handle a Canadian cheque.

| Characteristics | Values |

|---|---|

| Cheque Number | Located in the top right corner; unique number for tracking. |

| Date | Written by the payer in the top right corner; indicates when the cheque was issued. |

| Payee Line | Located below the date; specifies the name of the person or entity to be paid. |

| Amount in Numbers | Printed in the box on the right side; numerical representation of the amount. |

| Amount in Words | Written on the line below the payee; textual representation of the amount. |

| Bank Name | Printed at the top center or left side; identifies the issuing bank. |

| Transit Number | Five-digit number at the bottom left; identifies the bank branch. |

| Institution Number | Three-digit number at the bottom left; identifies the financial institution. |

| Account Number | Located at the bottom left, between the transit and institution numbers; unique to the account holder. |

| MICR Line | Magnetic ink characters at the bottom; includes transit, institution, and account numbers for machine reading. |

| Signature Line | Located at the bottom right; requires the payer’s signature for validity. |

| Memo Line | Optional field in the bottom left; used for notes or references. |

| Security Features | Includes watermarks, microprinting, and special inks to prevent fraud. |

| Currency | Canadian dollars (CAD) by default; may specify if in another currency. |

| Void Indicator | If "VOID" is printed across the cheque, it cannot be cashed or deposited. |

Explore related products

What You'll Learn

- Understanding Cheque Layout: Identify key sections like payee, amount, date, signature, and bank details

- Verifying Security Features: Check holograms, watermarks, and microprinting to ensure authenticity

- Reading Amounts Clearly: Understand both numerical and written amounts to avoid discrepancies

- Decoding Transit & Institution Numbers: Locate and interpret routing details for accurate processing

- Handling Post-Dated Cheques: Know rules for cheques with future dates and legal implications

![]()

Understanding Cheque Layout: Identify key sections like payee, amount, date, signature, and bank details

A Canadian bank cheque is a structured document, and understanding its layout is crucial for accurate processing and to prevent errors or fraud. The cheque is divided into several key sections, each serving a specific purpose. Let’s break down these sections: payee, amount, date, signature, and bank details, and explore their significance.

Payee Line: Who Receives the Funds?

Located at the top center of the cheque, the payee line is where the recipient’s name is written. This field is critical because it legally designates who can deposit or cash the cheque. For example, if the cheque is made out to "John Doe," only John Doe can endorse it. Be precise here—misspellings or incomplete names can render the cheque invalid. A practical tip: always double-check the payee’s name against their government-issued ID to avoid discrepancies.

Amount Fields: Numbers and Words Must Match

The amount section appears in two places: a numerical box and a written line. The numerical box is straightforward, but the written line requires the amount in words, followed by the word "and" before the cents (e.g., "One hundred and 50/100"). This dual format acts as a security measure—if the numbers and words don’t match, the bank may reject the cheque. For instance, writing "$150.00" in the box and "One hundred fifty" on the line is incorrect; it should be "One hundred fifty and 00/100."

Date Line: Timing Matters

The date line is typically found in the top right corner. It indicates when the cheque was written and when it becomes valid for deposit. Canadian cheques are generally valid for six months from the date written, though some banks may have shorter periods. Postdating a cheque (writing a future date) doesn’t prevent it from being cashed immediately, so be cautious. Conversely, an expired cheque may require reissuance.

Signature Panel: The Final Authorization

The signature panel is located at the bottom right. This is where the account holder signs to authorize the transaction. Without a signature, the cheque is incomplete and cannot be processed. The signature must match the one on file with the bank; discrepancies can lead to rejection. If the cheque is signed by a representative of a business, their name and title should be included below the signature for clarity.

Bank Details: Routing the Transaction

The bottom of the cheque contains pre-printed bank details, including the institution number, transit number, and account number. These are encoded in the MICR (Magnetic Ink Character Recognition) line, which helps banks process cheques electronically. While you don’t need to manually input these numbers, understanding their purpose highlights the cheque’s role in the banking system. For instance, the transit number identifies the specific branch, ensuring funds are routed correctly.

In summary, each section of a Canadian bank cheque serves a distinct function, from identifying the recipient to authorizing the payment. By familiarizing yourself with these key areas, you can ensure accuracy, prevent errors, and protect against fraud. Whether you’re writing or receiving a cheque, attention to detail in these sections is essential.

How to Add a Beneficiary to Your Standard Bank Account Easily

You may want to see also

Explore related products

![]()

Verifying Security Features: Check holograms, watermarks, and microprinting to ensure authenticity

Canadian bank cheques are equipped with sophisticated security features designed to thwart fraud, and verifying these elements is crucial for ensuring authenticity. Holograms, watermarks, and microprinting are among the primary tools used to protect against counterfeiting. Each of these features serves a unique purpose, and understanding how to identify them can safeguard both individuals and businesses from financial loss.

Holograms are one of the most visible security features on a Canadian cheque. Typically located in the top right corner, these 3D images shift appearance when tilted, displaying intricate patterns or logos. To verify a hologram, hold the cheque under a light source and observe the movement and depth of the image. Counterfeit cheques often lack this dynamic quality, appearing flat or poorly replicated. If the hologram seems static or lacks detail, it may indicate tampering.

Watermarks are another critical security feature, embedded directly into the cheque paper. These faint, translucent designs are visible when held up to light and typically depict the cheque issuer’s logo or a specific pattern. To check for a watermark, place the cheque on a flat surface and hold it up to a bright light source. Authentic watermarks are sharply defined and consistent, while fraudulent ones may appear blurry, incomplete, or absent. This step requires careful scrutiny, as subtle discrepancies can reveal a counterfeit.

Microprinting involves tiny, nearly invisible text that is difficult to replicate without specialized equipment. On a Canadian cheque, microprinting is often found along borders or within specific fields, such as the signature line. To inspect microprinting, use a magnifying glass to examine the text. Authentic microprinting will appear crisp and uniform, while counterfeit attempts may show uneven lines, smudging, or illegibility. This feature is particularly effective because its small scale makes it challenging for fraudsters to reproduce accurately.

When verifying these security features, it’s essential to approach the process methodically. Start with a known authentic cheque for comparison, if available, to familiarize yourself with genuine characteristics. Use proper lighting and tools, such as a magnifying glass or UV light if applicable, to enhance visibility. If any feature appears suspicious, refrain from accepting the cheque and report it to the issuing bank immediately. By mastering these verification techniques, you can confidently assess the legitimacy of a Canadian bank cheque and protect yourself from potential fraud.

Buying Gold Through RBC Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Reading Amounts Clearly: Understand both numerical and written amounts to avoid discrepancies

A single discrepancy between the numerical and written amounts on a Canadian bank cheque can render it invalid, leading to delays, fees, or even rejection. This critical detail demands meticulous attention, as even a minor error—such as writing "fifty" instead of "fifteen" beside the number 15—can trigger complications. Financial institutions rely on both formats to verify accuracy, making it essential to ensure they match precisely.

To avoid errors, start by writing the numerical amount in the designated box, using clear, legible digits. For example, write "$123.45" without crowding or ambiguity. Next, express the same amount in words on the line below, following a structured format: "One hundred twenty-three and 45/100." Note the use of "and" to separate dollars from cents, and ensure the fraction format ("xx/100") is consistent. This dual representation acts as a cross-check, reducing the risk of misinterpretation.

Consider a scenario where the numerical amount reads "$567.89," but the written form incorrectly states "Five hundred sixty-seven and 80/100." Such a discrepancy would immediately flag the cheque for review, potentially causing delays in processing. To prevent this, double-check both amounts before finalizing the cheque. If using pre-printed cheque-writing software, verify the alignment of both formats to ensure accuracy.

Practical tips include using a pen with dark, permanent ink to avoid smudging or fading, which could obscure the amounts. If making corrections, draw a single line through the error and write the accurate amount nearby, ensuring clarity. For large amounts, such as "$1,500.00," write "One thousand five hundred and 00/100" to maintain consistency. By mastering this dual-format approach, you minimize the risk of discrepancies and ensure smooth transaction processing.

Understanding Food Banks: How They Work and What They Provide

You may want to see also

Explore related products

![]()

Decoding Transit & Institution Numbers: Locate and interpret routing details for accurate processing

At the heart of every Canadian bank cheque lies a cryptic yet crucial sequence: the transit and institution numbers. These digits, often grouped together, form the routing details essential for accurate processing. Located at the bottom left corner of the cheque, this string typically begins with a prefix like "0" or "1," followed by a 4-digit institution number, a 5-digit transit number, and a checksum digit. For instance, "01234 56789 0" breaks down into institution number "1234," transit number "56789," and checksum "0." Understanding this structure is the first step in decoding the cheque’s routing information.

The institution number serves as the bank’s unique identifier, akin to a fingerprint in the financial system. Each Canadian financial institution is assigned a specific 4-digit code by the Canadian Payments Association. For example, Royal Bank of Canada (RBC) uses "003," while Toronto-Dominion Bank (TD) uses "004." This number ensures the cheque is routed to the correct bank. Meanwhile, the transit number pinpoints the exact branch where the account is held. Unlike institution numbers, transit numbers are not standardized across banks and can vary widely, even within the same city. Cross-referencing these numbers with official bank records or online databases can prevent errors in cheque processing.

Interpreting these numbers requires attention to detail, especially when dealing with handwritten or faded cheques. The checksum digit, though often overlooked, is critical for validating the sequence. It is calculated using a specific algorithm applied to the institution and transit numbers. For instance, if the checksum is incorrect, the cheque may be rejected by automated systems. Practical tips include using a magnifying glass for clarity and double-checking against the account holder’s bank statement. Additionally, many banks now offer mobile apps that allow users to verify these numbers instantly, reducing the risk of manual errors.

While the transit and institution numbers are primarily for internal banking processes, their accuracy directly impacts the cheque’s clearance time. Errors can lead to delays, returned cheques, or even financial penalties. For businesses processing large volumes of cheques, investing in automated systems that scan and validate these numbers can save time and resources. Individuals, on the other hand, should familiarize themselves with their own bank’s routing details to ensure seamless transactions. In an era of digital payments, mastering this analogue skill remains surprisingly relevant, bridging the gap between traditional and modern banking practices.

Securing Off-Grid Land: Bank-Free Strategies for Independent Ownership

You may want to see also

Explore related products

![]()

Handling Post-Dated Cheques: Know rules for cheques with future dates and legal implications

Post-dated cheques, those bearing a future date, present unique challenges and legal considerations in Canadian banking. While it might seem like a simple solution to delay payment, the rules surrounding these cheques are nuanced. Understanding these rules is crucial for both the payer and payee to avoid potential disputes and legal complications.

Unlike their American counterparts, Canadian post-dated cheques are generally not considered legal instruments until the date written on them. This means banks are not obligated to honor them before the specified date. Presenting a post-dated cheque before its date can result in it being returned unpaid, potentially incurring fees for both parties.

The key legal principle governing post-dated cheques in Canada is the negotiable instruments act. This act states that a cheque is a promise to pay on demand, but a post-dated cheque modifies this promise by specifying a future date. This distinction is vital: while a bank may choose to process a post-dated cheque early, they are under no legal obligation to do so.

Important Note: Writing "not valid before [date]" on a cheque does not guarantee it won't be processed early. Banks rely on the date written in the designated date box.

Despite the legal framework, practical considerations exist. Some businesses may accept post-dated cheques as a form of payment arrangement, but they should clearly communicate their policies and potential fees for early presentation. Payees should be aware that depositing a post-dated cheque before its date could lead to it being returned, causing inconvenience and potential damage to their relationship with the payer.

Practical Tip: If you need to issue a post-dated cheque, consider using alternative payment methods like online bill payments or pre-authorized debits, which offer more control over payment timing.

In conclusion, while post-dated cheques can be a useful tool in specific circumstances, they require careful handling. Understanding the legal implications and potential risks is essential for both parties involved. Clear communication and exploring alternative payment methods can help mitigate potential issues and ensure smooth financial transactions.

Optimal Record Retention: How Long Should Blood Banks Store Data?

You may want to see also

Frequently asked questions

The front of a Canadian bank cheque includes the cheque number, date line, payee line, amount box, amount line, signature line, and the bank’s information, such as the institution number, transit number, and account number.

These numbers are found at the bottom of the cheque. The institution number (3 digits) is on the left, followed by the transit number (5 digits), and then the account number (variable length). They are also printed in magnetic ink for machine readability.

The MICR line contains the institution number, transit number, and account number in magnetic ink. It allows banks to process cheques electronically, ensuring faster and more accurate transactions.

Yes, Canadian cheques can be written in either English or French, as both languages are officially recognized. Ensure the payee’s name, date, and amount are clear and consistent in the chosen language.