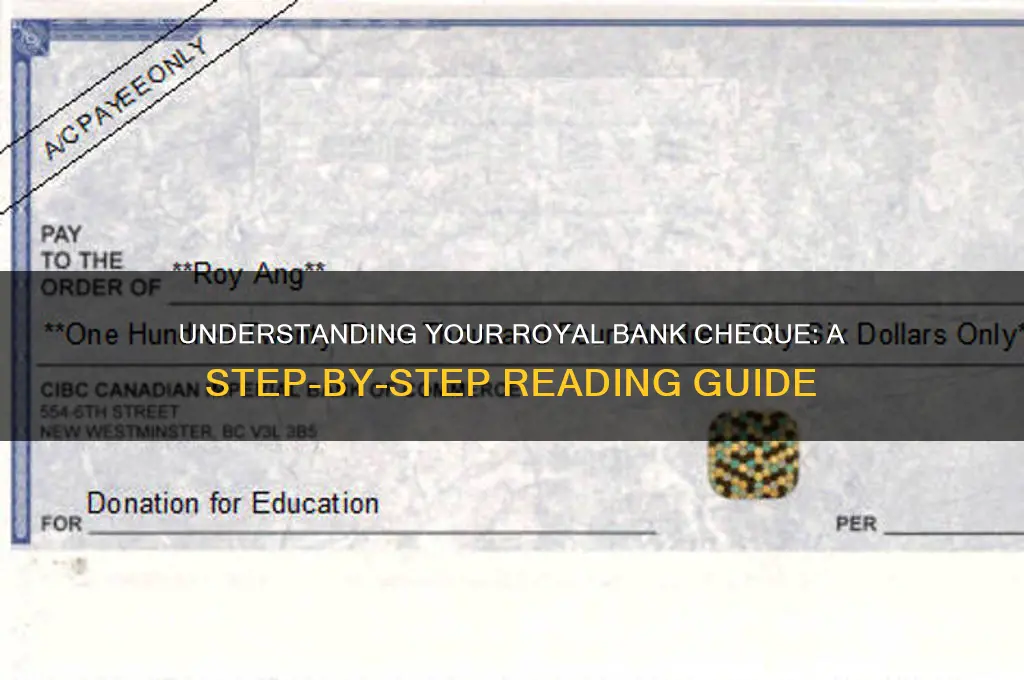

Reading a cheque from the Royal Bank requires understanding its key components to ensure accuracy and security. The cheque typically includes the bank’s name and logo at the top, followed by the account holder’s name and address. The date is written in the top right corner, and the payee’s name is clearly stated on the line provided. The numerical amount is indicated in the box on the right, while the same amount is spelled out in words on the line below to prevent fraud. The account and routing numbers are printed at the bottom, along with a signature line for authorization. Familiarizing yourself with these elements ensures you can correctly interpret and process the cheque.

| Characteristics | Values |

|---|---|

| Bank Name | Royal Bank of Canada (RBC) |

| Cheque Layout | Standardized format with sections for payer, payee, amount, and details |

| Payer Information | Account holder's name and address printed on the top left corner |

| Payee Line | "Pay to the Order of" followed by the recipient's name |

| Amount in Words | Written in words (e.g., "One Hundred and Fifty Dollars") |

| Amount in Numbers | Numerical value in the box on the right side (e.g., $150.00) |

| Date Line | Located in the top right corner; must be filled out by the payer |

| Memo/Note Line | Optional field for additional notes or references |

| MICR Code | Magnetic Ink Character Recognition (MICR) at the bottom for bank details |

| Account and Transit Number | Printed at the bottom left, includes account and transit numbers |

| Cheque Number | Unique number located at the top right corner |

| Signature Line | Must be signed by the account holder in the bottom right corner |

| Security Features | Watermarks, microprinting, and special ink to prevent fraud |

| Currency | Canadian Dollars (CAD) |

| Validity Period | Typically valid for 6 months from the date written |

| Endorsement Section | On the back for the payee to sign if depositing or cashing the cheque |

Explore related products

What You'll Learn

- Understanding Cheque Layout: Key sections and their purposes on a Royal Bank cheque

- Identifying Account Details: Locating account and transit numbers for accurate transactions

- Verifying Payee Information: Ensuring correct recipient details to avoid errors or fraud

- Checking Dates and Amounts: Validating issue dates and written/numeric amounts for correctness

- Security Features: Recognizing Royal Bank’s anti-fraud measures on cheques

![]()

Understanding Cheque Layout: Key sections and their purposes on a Royal Bank cheque

A Royal Bank cheque is a financial document with a specific layout designed to ensure clarity, security, and functionality. At first glance, the cheque appears structured yet complex, but understanding its key sections simplifies its use. The top portion typically displays the bank’s name, logo, and contact information, establishing authenticity and trust. Below this, the account holder’s details, including name, address, and account number, are prominently featured, ensuring the cheque is linked to the correct individual or entity. These elements form the foundation of the cheque’s identity, making them critical for verification and processing.

Moving downward, the date line is a small yet pivotal section. It requires the payer to specify when the cheque was written, a detail that affects its validity and legal standing. Adjacent to this is the payee line, where the recipient’s name is clearly stated. Precision here is essential, as misspelled or incomplete names can render the cheque unusable. The amount box and word line follow, both serving to indicate the cheque’s value. While the box allows for numerical input, the word line requires the amount to be written out in words, a dual-layer system that minimizes errors and fraud.

The signature line is arguably the most critical section, as it authorizes the transaction. Without a valid signature matching the account holder’s on file, the cheque is invalid. Nearby, the memo line offers optional space for notes, such as referencing an invoice or purpose of payment. While not mandatory, this field can provide context for both payer and payee, streamlining record-keeping. These functional sections collectively ensure the cheque serves its purpose efficiently.

On the lower portion of the cheque, the MICR (Magnetic Ink Character Recognition) line contains encoded account and routing information. This machine-readable strip facilitates automated processing by banks, reducing manual errors and expediting clearing times. Though not directly interacted with by users, its presence underscores the cheque’s integration with modern banking systems. Understanding these sections not only demystifies the cheque’s layout but also empowers users to handle it confidently and accurately.

Finally, the back of the cheque often includes endorsement areas and terms of use. The endorsement section requires the payee’s signature upon deposit, a security measure confirming receipt. Terms of use, though less frequently referenced, outline legal conditions governing the cheque’s acceptance and processing. Together, these elements complete the cheque’s design, balancing usability with security. By familiarizing oneself with these sections, one can navigate cheque transactions with precision and assurance.

The Banking Profit: Where Does It Come From?

You may want to see also

Explore related products

![]()

Identifying Account Details: Locating account and transit numbers for accurate transactions

Cheques may seem like relics in our digital age, but they remain a vital tool for financial transactions, especially when dealing with specific payments or transfers. Understanding how to read a cheque is crucial, and one of the most critical aspects is identifying the account and transit numbers. These numbers are the backbone of any cheque transaction, ensuring funds are directed to the correct account. Let’s break down how to locate and interpret these details on a Royal Bank cheque.

Step-by-Step Guide to Locating Account and Transit Numbers

On a Royal Bank cheque, the account and transit numbers are typically found at the bottom, printed in a series of magnetic ink characters known as MICR (Magnetic Ink Character Recognition) numbers. The transit number, a 5-digit code, identifies the specific branch where the account is held. It is usually the first set of numbers on the left. Following the transit number is the institution number, a 3-digit code unique to Royal Bank (003). Finally, the account number, which can vary in length but is typically 7 to 12 digits, appears last. For example, if the MICR line reads *12345 003 6789012*, the transit number is *12345*, the institution number is *003*, and the account number is *6789012*. Always double-check these numbers to avoid errors in transactions.

Why Accuracy Matters

Mistyping or misreading account and transit numbers can lead to costly mistakes, such as funds being deposited into the wrong account or transactions being rejected. For instance, a single digit error in the transit number could route the payment to a different branch, causing delays or financial losses. Similarly, an incorrect account number might result in the funds being credited to someone else’s account. In some cases, rectifying such errors can take days or even weeks, depending on the bank’s policies and procedures. Precision is non-negotiable when dealing with these details.

Practical Tips for Error-Free Transactions

To ensure accuracy, always cross-reference the account and transit numbers with other documents, such as bank statements or online banking records. If writing a cheque, use a pen with dark ink to ensure the MICR line is readable. When receiving a cheque, verify the numbers against the payer’s account details if possible. For digital transactions, manually input the numbers instead of relying on optical character recognition (OCR) tools, which can sometimes misinterpret characters. Finally, if in doubt, contact Royal Bank directly for assistance—it’s better to take an extra minute than to risk a financial mishap.

Comparing Cheque Formats: Royal Bank vs. Others

While the basic structure of cheques is standardized across banks, slight variations exist. For example, some banks may include additional identifiers or use different MICR line formats. Royal Bank’s cheques are consistent in their layout, making it easier to locate the transit and account numbers once you’re familiar with their design. However, if you frequently handle cheques from multiple institutions, it’s worth noting these differences. For instance, credit union cheques might place the institution number in a different position, while international cheques may include country-specific codes. Familiarizing yourself with these nuances can save time and reduce errors across all transactions.

Step-by-Step Guide to Activating UCO Bank Net Banking Easily

You may want to see also

Explore related products

![]()

Verifying Payee Information: Ensuring correct recipient details to avoid errors or fraud

A single misspelled character or transposed digit in the payee information can derail a cheque transaction, leading to delays, disputes, or even fraudulent redirection of funds. Royal Bank of Canada cheques require meticulous verification of the payee's name and account details to mitigate these risks. Start by cross-referencing the printed or handwritten payee name against any accompanying invoices, contracts, or payment authorizations. For business payments, ensure the name matches the legal entity registered with the bank, avoiding colloquial abbreviations or nicknames. Individuals should verify both first and last names, including middle initials if applicable, to prevent misidentification.

Beyond names, account numbers demand equal scrutiny. A misplaced digit can route funds to an unintended recipient, often irreversibly. When verifying account details, use the "read-aloud" method: one person reads the number from the cheque, while another confirms it against the source document. For added security, compare the account number to previous transactions with the same payee, if available. Royal Bank’s cheques often include a memo line; while optional, it can serve as a secondary verification point by noting the purpose of the payment (e.g., "Invoice #12345") to ensure alignment with the payee’s identity.

Fraudsters exploit gaps in verification processes, particularly in high-volume payment environments. To counter this, implement a dual-authorization system for cheques above a certain threshold (e.g., $1,000). This requires two designated individuals to independently confirm the payee’s details before the cheque is issued. For personal cheques, consider contacting the payee directly to verify their banking information, especially if it’s the first transaction. Royal Bank also offers digital tools, such as online banking platforms, to cross-check payee details against pre-approved vendor lists or saved beneficiaries.

Finally, maintain a verification log for all cheque transactions, recording the date, payee name, account number, and the initials of the verifier. This creates an audit trail that can resolve discrepancies and demonstrate due diligence in case of fraud. While Royal Bank’s security features, like microprinting and watermarks, protect against cheque forgery, human error remains a vulnerability. By treating payee verification as a critical control point, individuals and businesses can safeguard their finances and maintain trust in cheque-based transactions.

Mastering Bank Yield IRR Calculation: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Checking Dates and Amounts: Validating issue dates and written/numeric amounts for correctness

A cheque's issue date is more than a formality—it’s a critical timestamp that determines validity and processing order. Royal Bank cheques typically include a pre-printed date field, but the written date (e.g., "January 15, 2023") must match the numeric format (e.g., "15/01/2023") to avoid discrepancies. Discrepancies can lead to rejection, as banks rely on this consistency to verify authenticity. Always cross-reference both formats, ensuring they align with the day, month, and year the cheque was issued.

The written and numeric amounts on a cheque must correspond precisely, but errors are common. For instance, if the written amount is "One Hundred Dollars and 50/100," the numeric box should read "$100.50." Even a minor mismatch, like "$100.00," renders the cheque invalid. To prevent this, double-check the written amount by converting it to numeric form yourself, then compare. Royal Bank’s systems flag inconsistencies, delaying processing or triggering returns, so accuracy is non-negotiable.

Fraudulent alterations often target dates and amounts, making validation a security measure. Scrutinize the ink and handwriting for uniformity—sudden changes in style or ink color suggest tampering. For older cheques, verify the issue date hasn’t exceeded the 6-month validity period, as Royal Bank may refuse stale-dated cheques. If in doubt, contact the issuer to confirm details before depositing or cashing.

Practical tip: Use a magnifying glass to inspect micro-printing or security features around the date and amount fields, as these areas are harder to alter without detection. Pair this with a quick calculation to ensure the written amount matches the numeric one. For example, break down "One Thousand Two Hundred Thirty-Four and 75/100" into $1,200 + $34.75 to confirm it equals $1,234.75. This methodical approach minimizes errors and safeguards against fraud.

In summary, validating dates and amounts on a Royal Bank cheque requires attention to detail and a systematic approach. Matching formats, scrutinizing for alterations, and confirming validity periods are essential steps. By treating this process as a routine check, you ensure seamless transactions and protect yourself from potential issues. Remember, a cheque’s integrity hinges on these small but significant details.

FASB Reporting Guidelines for Bank Overdrafts: Best Practices Explained

You may want to see also

Explore related products

![Customizable 3 to a Page Business Checks with Tear Off Stubs | White, Pink, Green, and Yellow Options | Compatible with 7 Ring Binders [Printed in The USA] (American Eagle, 54)](https://m.media-amazon.com/images/I/618e1m5EVoL._AC_UL320_.jpg)

![]()

Security Features: Recognizing Royal Bank’s anti-fraud measures on cheques

Royal Bank of Canada (RBC) cheques are equipped with advanced security features to combat fraud, making it crucial for users to recognize these measures. One of the most prominent features is the holographic foil strip located along the side of the cheque. This strip contains dynamic images and text that shift when tilted, making it nearly impossible to replicate accurately. Counterfeit cheques often lack this feature or have a static, low-quality imitation, so always inspect the strip under varying angles to verify its authenticity.

Another key security element is the microprinting found in the border design and signature line. This text is so small that it appears as a solid line to the naked eye, but when magnified, it reveals detailed characters. Fraudulent cheques typically omit this feature or produce blurry, illegible microprint. To check, use a magnifying glass or high-resolution camera to ensure the tiny text is clear and consistent.

The chemically reactive paper used by RBC is designed to detect alterations made with common chemicals like bleach or solvents. If someone attempts to modify the cheque, the paper will discolor or stain, immediately signaling tampering. For instance, if the amount written in the "Pay" field appears unusually faded or discolored, it could indicate fraud. Always compare the cheque’s paper quality and color consistency with known genuine samples.

RBC also employs watermarks and invisible ink that are only visible under ultraviolet (UV) light. When exposed to a UV source, the bank’s logo and other security markings will fluoresce, confirming the cheque’s legitimacy. While not all users have access to UV lights, financial institutions and businesses often use this tool during verification. If you suspect fraud, request a UV inspection from a trusted authority.

Finally, the unique serial number and barcode on each cheque are linked to RBC’s secure database. These identifiers ensure the cheque is traceable and can be cross-referenced with the bank’s records. If the numbers appear tampered with or mismatched, it’s a red flag. Always verify the cheque’s details with RBC directly if you have doubts, as this step can prevent significant financial loss.

By familiarizing yourself with these security features, you can confidently identify genuine RBC cheques and protect yourself from fraud. Regularly updating your knowledge of these measures is essential, as banks continually enhance their security protocols to stay ahead of counterfeiters.

Pay LIC Premiums Easily: A Step-by-Step Net Banking Guide

You may want to see also

Frequently asked questions

The date is written in the top right corner of the cheque. It should be filled out in the format of month, day, and year (e.g., 01/15/2023).

The payee’s name is written on the line labeled "Pay to the Order of" or in the designated payee field. Ensure the name is spelled correctly to avoid issues.

The signature line is located at the bottom right corner of the cheque. The cheque must be signed by the account holder to be valid; unsigned cheques will not be processed.