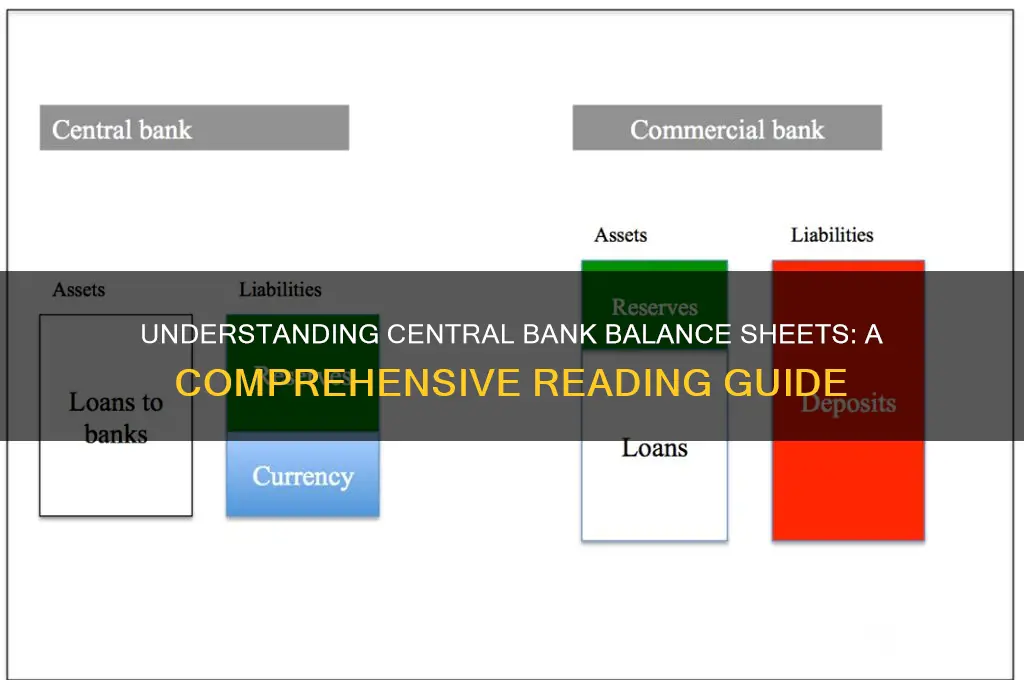

Reading a central bank's balance sheet is essential for understanding its monetary policy actions and financial health. The balance sheet typically consists of two main sections: assets and liabilities. Assets include items like foreign currency reserves, government securities, and loans to financial institutions, reflecting the central bank’s interventions in the economy. Liabilities encompass currency in circulation, deposits from commercial banks, and other obligations, highlighting the sources of its funding. Analyzing these components provides insights into the central bank’s liquidity management, inflation control strategies, and efforts to stabilize the financial system. Key metrics, such as the size of the balance sheet and the composition of assets, can indicate the central bank’s policy stance, whether it is tightening or easing monetary conditions. Mastering this skill is crucial for investors, economists, and policymakers to interpret economic signals and anticipate future policy moves.

Explore related products

What You'll Learn

- Assets Overview: Understand reserves, loans, securities, and other holdings on the asset side

- Liabilities Breakdown: Analyze deposits, currency, and debt obligations listed under liabilities

- Equity Section: Examine capital, retained earnings, and net worth in the equity portion

- Monetary Policy Impact: See how balance sheet changes reflect policy actions and goals

- Key Ratios & Metrics: Use liquidity, leverage, and solvency ratios for assessment

![]()

Assets Overview: Understand reserves, loans, securities, and other holdings on the asset side

Central bank balance sheets are a snapshot of their financial health and policy tools, with the asset side revealing how they manage liquidity, support economies, and maintain stability. Reserves, loans, securities, and other holdings each play distinct roles, reflecting both operational needs and strategic interventions. Understanding these components is crucial for interpreting a central bank’s actions and their broader economic impact.

Reserves form the backbone of a central bank’s liquidity management. These typically include foreign currency holdings, gold, and special drawing rights (SDRs). For instance, the Federal Reserve holds over $6 trillion in foreign currency reserves, primarily in U.S. Treasury securities, to stabilize the dollar and meet international obligations. Reserves act as a buffer during crises, such as the 2008 financial meltdown, when central banks swapped currencies to ease global liquidity strains. Monitoring reserve levels provides insight into a bank’s ability to respond to shocks and its confidence in domestic currency stability.

Loans represent direct credit extended to commercial banks or governments, often as a last resort during liquidity crunches. The European Central Bank’s Targeted Long-Term Refinancing Operations (TLTROs) are a prime example, offering low-interest loans to banks to encourage lending to businesses and households. Unlike reserves, loans are riskier, as they depend on borrowers’ repayment capacity. A surge in central bank lending, as seen during the COVID-19 pandemic, signals efforts to prevent credit freezes but also raises concerns about moral hazard and long-term financial stability.

Securities, primarily government bonds, dominate most central bank balance sheets. The Bank of Japan, for instance, holds over 50% of outstanding Japanese government bonds, a policy aimed at suppressing long-term interest rates and stimulating inflation. Securities serve dual purposes: they inject liquidity into the financial system through open market operations and act as a tool for monetary policy. Quantitative easing (QE) programs, where central banks purchase large volumes of securities, highlight their role in shaping economic conditions. Analyzing the composition and maturity of securities holdings reveals a bank’s stance on interest rates and inflation.

Other holdings encompass a mix of assets, from IMF positions to physical assets like property. While smaller in scale, these holdings reflect operational needs and strategic partnerships. For example, the People’s Bank of China includes renminbi-denominated assets in its portfolio to support internationalization of the currency. These miscellaneous assets, though less influential than reserves or securities, provide a fuller picture of a central bank’s global engagement and domestic priorities.

In sum, the asset side of a central bank’s balance sheet is a dynamic toolkit, with reserves ensuring liquidity, loans addressing credit shortages, securities guiding monetary policy, and other holdings supporting operational and strategic goals. By dissecting these components, observers can gauge a bank’s policy direction, risk appetite, and response to economic challenges. Practical tips include tracking changes in asset composition over time, comparing holdings across central banks, and correlating shifts with economic indicators like inflation or unemployment rates.

Risk and Compliance: Banking's Fort Knox

You may want to see also

Explore related products

![]()

Liabilities Breakdown: Analyze deposits, currency, and debt obligations listed under liabilities

Central bank balance sheets are a treasure trove of information, but the liabilities section often holds the key to understanding a nation's monetary policy and financial stability. Here, we dissect the critical components: deposits, currency in circulation, and debt obligations. These elements reveal how a central bank manages liquidity, supports the banking system, and influences the broader economy.

Deposits form a significant portion of central bank liabilities, primarily comprising reserves held by commercial banks. These reserves are crucial for maintaining the stability of the banking system, as they ensure banks have sufficient funds to meet withdrawal demands and settle transactions. For instance, during the 2008 financial crisis, central banks like the Federal Reserve expanded their balance sheets by increasing reserves, providing a liquidity backstop to prevent bank runs. Analyzing deposit levels can indicate the central bank’s stance on monetary policy—higher reserves often signal accommodative measures, while reductions may suggest tightening. Practitioners should track changes in reserve requirements and the interest paid on these reserves, as these directly impact bank lending behavior and, consequently, economic activity.

Currency in circulation represents the physical cash held by the public and is a direct liability of the central bank. This figure is a barometer of economic activity and public confidence in the financial system. In times of uncertainty, such as during the COVID-19 pandemic, currency in circulation surged as individuals and businesses hoarded cash. Conversely, a decline in currency holdings might reflect increased use of digital payments or deflationary pressures. Central banks must carefully manage currency issuance to avoid inflationary or deflationary spirals. For example, the European Central Bank closely monitors euro banknotes in circulation, adjusting production to meet demand while ensuring counterfeiting remains minimal.

Debt obligations on a central bank’s balance sheet typically include government securities and other debt instruments. These liabilities reflect the central bank’s role in financing government spending and managing public debt. For instance, the Bank of Japan holds a substantial portion of the country’s government bonds, a policy aimed at keeping long-term interest rates low to stimulate economic growth. However, excessive reliance on central bank financing of government debt can raise concerns about fiscal dominance and inflation. Analysts should scrutinize the maturity and composition of these debt obligations to assess the central bank’s ability to maintain monetary independence and financial stability.

In practice, interpreting these liabilities requires a holistic approach. For example, a central bank with high reserves and currency in circulation but low debt obligations may be prioritizing financial stability over fiscal support. Conversely, a balance sheet dominated by government debt could indicate challenges in managing public finances. To deepen your analysis, compare these figures across time and against macroeconomic indicators like inflation, GDP growth, and unemployment rates. Tools such as the money multiplier and reserve-to-deposit ratios can further illuminate the relationship between central bank liabilities and the broader financial system.

Ultimately, the liabilities section of a central bank’s balance sheet is a dynamic reflection of its policy objectives and economic conditions. By meticulously analyzing deposits, currency, and debt obligations, stakeholders can gain insights into liquidity management, monetary policy transmission, and systemic risks. Whether you’re an economist, investor, or policymaker, mastering this breakdown is essential for navigating the complexities of modern finance.

Exploring TCF Bank's ATM Network: How Extensive is Their Reach?

You may want to see also

Explore related products

$21.99 $30

![]()

Equity Section: Examine capital, retained earnings, and net worth in the equity portion

The equity section of a central bank's balance sheet is a critical window into its financial health and stability. Here, you’ll find three key components: capital, retained earnings, and net worth. Capital represents the initial funds provided by the government or other stakeholders to establish the bank, acting as a buffer against losses. Retained earnings reflect the cumulative profits or losses the bank has generated over time, minus dividends paid out. Together, these elements determine the bank’s net worth, a measure of its overall financial strength. Understanding these figures is essential for assessing the bank’s ability to absorb shocks and maintain confidence in the financial system.

To analyze the equity section effectively, start by examining the capital figure. This is often a fixed amount, but changes can indicate government injections or withdrawals, signaling policy shifts or financial distress. For instance, a sudden increase in capital might suggest a response to a crisis, while a decrease could imply a shift in the bank’s funding strategy. Next, scrutinize retained earnings, which reveal the bank’s profitability and risk management over time. Negative retained earnings could indicate persistent losses, while positive figures suggest prudent management. However, be cautious: retained earnings alone don’t tell the full story—they must be viewed in the context of the bank’s operations and economic environment.

A practical tip for interpreting these components is to compare them across time periods or against peer institutions. For example, if a central bank’s retained earnings have declined sharply over the past year while others in the region remain stable, it may warrant deeper investigation. Additionally, calculate the net worth by adding capital and retained earnings. A declining net worth could signal eroding financial stability, while a steady or growing figure reinforces the bank’s resilience. Keep in mind that central banks often operate under unique mandates, so their equity structures may differ from commercial banks.

One common misconception is that a central bank’s equity section mirrors that of a commercial bank. In reality, central banks typically have lower equity relative to their balance sheet size because their primary role is monetary policy, not profit maximization. For instance, the Federal Reserve’s capital and surplus account for less than 1% of its total assets. This doesn’t imply weakness but rather reflects its policy-driven nature. When evaluating a central bank’s equity, focus on trends rather than absolute values, and consider external factors like inflation, interest rates, and fiscal policy.

In conclusion, the equity section is a vital yet often overlooked part of a central bank’s balance sheet. By dissecting capital, retained earnings, and net worth, you can gauge the bank’s financial resilience and its capacity to fulfill its mandate. Remember, these figures are not standalone metrics but pieces of a larger puzzle. Combine them with other balance sheet items, such as assets and liabilities, to form a comprehensive view of the bank’s health. With this approach, you’ll be better equipped to interpret central bank actions and their implications for the broader economy.

River Velocity's Impact on Bank Sculpting: Erosion Dynamics Explained

You may want to see also

Explore related products

![]()

Monetary Policy Impact: See how balance sheet changes reflect policy actions and goals

Central bank balance sheets are not static documents; they are dynamic tools that reveal the pulse of monetary policy in action. Every asset and liability listed represents a deliberate choice, a lever pulled to influence the economy. To decipher the impact of monetary policy, one must learn to read these changes as a narrative of economic intervention.

A central bank's balance sheet expands when it purchases assets, injecting liquidity into the financial system. This is often a hallmark of accommodative monetary policy, aimed at stimulating economic growth during downturns. For instance, the Federal Reserve's quantitative easing programs involved massive purchases of government bonds and mortgage-backed securities, ballooning its balance sheet from $900 billion in 2007 to over $9 trillion by 2022. This influx of liquidity lowered long-term interest rates, encouraged lending, and bolstered asset prices, all in service of reviving a struggling economy.

Conversely, a shrinking balance sheet signals a tightening of monetary policy, typically employed to combat inflation. When a central bank sells assets or allows them to mature without replacement, it withdraws liquidity from the system. This can lead to higher interest rates, slower credit growth, and a cooling of economic activity. The European Central Bank's recent reduction of its asset purchase program, coupled with interest rate hikes, exemplifies this approach in response to surging inflation across the Eurozone.

Understanding the specific assets targeted by these balance sheet adjustments provides further insight into policy goals. Purchases of government bonds aim to lower long-term borrowing costs, while buying corporate bonds or asset-backed securities can directly support specific sectors. For example, the Bank of Japan's purchases of exchange-traded funds (ETFs) were designed to prop up stock prices and encourage risk-taking by investors.

Reading a central bank's balance sheet for monetary policy impact requires a keen eye for both magnitude and composition of changes. It's not just about the size of the balance sheet, but also the types of assets held and the pace of adjustments. By analyzing these dynamics, observers can discern the central bank's assessment of economic conditions and its chosen tools for achieving its mandate of price stability and sustainable growth. This understanding is crucial for investors, policymakers, and anyone seeking to navigate the complexities of the modern financial landscape.

Does M&T Bank Offer Coin Counting Machines? Find Out Here

You may want to see also

Explore related products

![]()

Key Ratios & Metrics: Use liquidity, leverage, and solvency ratios for assessment

Central bank balance sheets are complex documents that reveal much about a country's monetary policy and financial health. To decipher their implications, analysts turn to key ratios and metrics, specifically liquidity, leverage, and solvency ratios. These tools provide a quantitative lens to assess a central bank's ability to manage its assets and liabilities effectively.

Liquidity ratios, such as the reserve-to-deposit ratio, gauge a central bank's capacity to meet short-term obligations. For instance, a reserve-to-deposit ratio below 5% may indicate potential liquidity risks, whereas a ratio above 10% suggests a more comfortable liquidity position. The European Central Bank, for example, maintains a target reserve-to-deposit ratio of around 1%, reflecting its confidence in the eurozone's financial stability.

To calculate leverage ratios, analysts examine the central bank's total assets relative to its capital. A common metric is the asset-to-capital ratio, which should ideally not exceed 20:1. Central banks with higher leverage ratios may face increased vulnerability to market fluctuations. The US Federal Reserve, with an asset-to-capital ratio of approximately 15:1, demonstrates a relatively conservative approach to leverage management. When analyzing these ratios, consider the following steps: identify the relevant line items on the balance sheet, calculate the ratio, and compare it to historical data or peer institutions.

Solvency ratios, on the other hand, assess a central bank's long-term financial health. The net worth-to-total assets ratio is a critical metric, with values below 5% raising concerns about solvency. Central banks in emerging markets often exhibit lower net worth-to-total assets ratios due to higher inflation and currency risks. A comparative analysis of central banks in similar economic contexts can provide valuable insights. For example, comparing the solvency ratios of the Reserve Bank of India and the People's Bank of China reveals distinct approaches to managing foreign exchange reserves and gold holdings.

A persuasive argument can be made for the importance of stress testing these ratios under various scenarios. By simulating extreme market conditions, analysts can evaluate a central bank's resilience to shocks. Suppose a central bank's liquidity ratio drops below 3% during a hypothetical crisis. In that case, policymakers may need to reconsider their asset purchase programs or reserve requirements. Practical tips for stress testing include using historical data to inform scenario design and incorporating expert judgment to refine assumptions. By integrating liquidity, leverage, and solvency ratios into their analysis, stakeholders can make more informed decisions about a central bank's financial stability and policy effectiveness.

Does US Bank Offer Free Notary Services? What You Need to Know

You may want to see also

Frequently asked questions

A central bank balance sheet is a financial statement that shows the assets, liabilities, and capital of a central bank. It is important because it reflects the central bank’s monetary policy actions, financial stability efforts, and overall influence on the economy.

Central bank balance sheets are typically published on the official website of the respective central bank (e.g., the Federal Reserve, European Central Bank, Bank of Japan). They are often released periodically, such as weekly, monthly, or quarterly.

The key components include assets (e.g., government securities, foreign reserves, loans to banks), liabilities (e.g., currency in circulation, bank reserves), and capital (e.g., retained earnings, equity).

Quantitative easing expands the central bank’s balance sheet by increasing assets (e.g., purchasing government bonds or other securities) and liabilities (e.g., growing bank reserves or currency in circulation).

A shrinking balance sheet typically indicates that the central bank is reducing its holdings of assets (e.g., selling securities or letting them mature) and tightening monetary policy, often to control inflation or normalize financial conditions.