The question of whether a bank is a company or an organization often arises due to the unique nature of banking institutions. At its core, a bank is indeed a company, as it operates as a business entity with the primary goal of generating profit through financial services such as lending, deposits, and investments. However, banks also function as highly regulated organizations, subject to stringent oversight by governmental and financial authorities to ensure stability, consumer protection, and compliance with legal standards. This dual nature—being both a profit-driven company and a regulated entity—distinguishes banks from typical businesses, making them a specialized type of organization within the broader corporate landscape.

| Characteristics | Values |

|---|---|

| Legal Structure | A bank is typically a company, often structured as a corporation (e.g., public or private limited company). It is a legal entity registered under specific laws, such as banking regulations and corporate laws. |

| Ownership | Banks can be owned by shareholders (in the case of public banks) or private individuals/entities (in the case of private banks). |

| Profit Motive | Banks operate with a profit motive, generating revenue through interest, fees, and financial services. |

| Regulatory Oversight | Banks are heavily regulated by financial authorities (e.g., central banks, financial regulators) to ensure stability and consumer protection. |

| Purpose | While banks are companies, their primary purpose is to provide financial services (e.g., loans, deposits, payments) to individuals and businesses, often with a focus on economic development. |

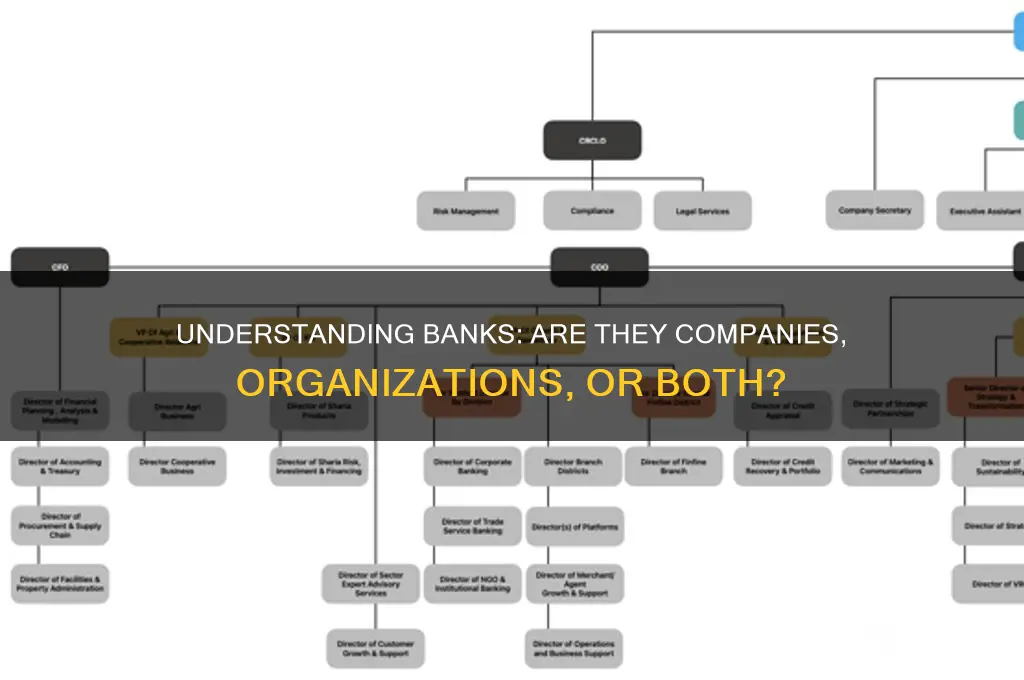

| Organizational Hierarchy | Banks have a structured organizational hierarchy, including board members, executives, and employees, similar to other companies. |

| Taxation | Banks are subject to corporate taxes and other financial levies as per the jurisdiction in which they operate. |

| Accountability | Banks are accountable to their shareholders, regulators, and customers, ensuring transparency and compliance with laws. |

| Scope of Operations | Banks operate within the financial sector, offering specialized services, but they are still considered companies in terms of their legal and operational framework. |

| Incorporation | Banks are incorporated entities, registered with a specific legal identity, distinct from their owners or founders. |

Explore related products

What You'll Learn

- Legal Structure: Banks are typically incorporated companies with a legal structure defined by regulations

- Ownership Types: They can be privately owned, publicly traded, or government-owned entities

- Regulatory Oversight: Banks operate under strict financial regulations and organizational compliance standards

- Business Model: Focused on financial services, banks function as profit-driven companies or public organizations

- Classification: Legally, banks are companies but often categorized as financial institutions or organizations

![]()

Legal Structure: Banks are typically incorporated companies with a legal structure defined by regulations

Banks, as financial institutions, are fundamentally structured as incorporated companies, a designation that carries significant legal and operational implications. This incorporation is not arbitrary but is mandated by regulatory frameworks designed to ensure stability, accountability, and consumer protection. For instance, in the United States, banks must adhere to the National Bank Act or state-specific banking laws, which outline the requirements for incorporation, including minimum capital thresholds and governance structures. Similarly, in the European Union, the Capital Requirements Directive (CRD) and the Capital Requirements Regulation (CRR) provide a harmonized framework for bank incorporation, emphasizing risk management and transparency. This legal structure is critical because it establishes banks as distinct legal entities, separate from their owners, thereby limiting personal liability and facilitating complex financial operations.

Incorporating a bank involves a series of precise steps, each governed by regulatory oversight. Prospective banks must file articles of incorporation with the relevant regulatory body, such as the Office of the Comptroller of the Currency (OCC) in the U.S. or the Prudential Regulation Authority (PRA) in the U.K. These documents detail the bank’s purpose, share structure, and governance model. Additionally, banks are required to meet stringent capital adequacy ratios, often set at a minimum of 8% of risk-weighted assets under Basel III standards. This ensures that banks maintain sufficient capital to absorb losses and protect depositors. Failure to comply with these requirements can result in penalties, operational restrictions, or even revocation of the banking license.

The regulatory-driven legal structure of banks serves multiple purposes, balancing the need for financial innovation with the imperative of systemic stability. For example, the separation of ownership and management, a hallmark of incorporated companies, allows banks to attract professional leadership while safeguarding against conflicts of interest. Moreover, regulatory bodies often impose restrictions on the types of activities banks can engage in, such as the Volcker Rule in the U.S., which limits proprietary trading. These measures are designed to prevent excessive risk-taking and protect the broader financial system. However, this structure also imposes significant compliance burdens, requiring banks to invest heavily in legal and risk management functions.

A comparative analysis reveals that while banks share the incorporated company structure with other businesses, the degree of regulatory scrutiny they face is unparalleled. Unlike a retail company or a tech startup, banks are subject to continuous monitoring, stress testing, and reporting requirements. For instance, banks must submit regular financial statements to regulators, undergo periodic audits, and maintain detailed records of all transactions. This heightened oversight is justified by the critical role banks play in the economy, particularly their function as custodians of public deposits and facilitators of credit. However, it also underscores the unique challenges banks face in balancing profitability with compliance.

In conclusion, the legal structure of banks as incorporated companies is a carefully designed framework that reflects their unique role in the economy. It is not merely a bureaucratic formality but a cornerstone of financial stability and consumer trust. By adhering to strict regulatory standards, banks are able to operate as reliable intermediaries between savers and borrowers, while also mitigating the risks inherent in financial activities. For stakeholders, understanding this structure is essential, as it provides insight into the constraints and opportunities that shape the banking industry. Whether you are an investor, a policymaker, or a customer, recognizing the regulatory underpinnings of bank incorporation is key to navigating the complexities of modern finance.

Are TIAA Bank CDs FDIC Insured? Understanding Your Deposit Protection

You may want to see also

Explore related products

![]()

Ownership Types: They can be privately owned, publicly traded, or government-owned entities

Banks, as financial institutions, exhibit a diverse range of ownership structures, each with distinct implications for their operations, governance, and public perception. Privately owned banks are typically controlled by individuals, families, or small groups of investors. This ownership type fosters agility and personalized decision-making, as seen in boutique investment banks or regional lenders. However, their limited access to capital can constrain growth and resilience during economic downturns. For instance, a family-owned bank might prioritize long-term legacy over short-term profits, offering tailored services but potentially lacking the scale to compete with larger institutions.

In contrast, publicly traded banks operate as corporations whose shares are listed on stock exchanges, making them accessible to a broad base of investors. This structure enables access to vast capital markets, facilitating expansion and innovation. Shareholder accountability, however, often pressures these banks to prioritize quarterly earnings over long-term sustainability. JPMorgan Chase and HSBC exemplify this model, balancing global reach with the demands of diverse stakeholders. Investors considering such banks should scrutinize financial reports and governance practices to assess stability and ethical standards.

Government-owned banks, on the other hand, serve as instruments of public policy, often focusing on financial inclusion, economic development, or crisis stabilization. These institutions, like Germany’s KfW or India’s State Bank of India, operate with explicit mandates to support national objectives. While they benefit from sovereign backing, they may face inefficiencies due to bureaucratic constraints or political interference. Citizens and businesses engaging with these banks should align their expectations with the institution’s public service goals rather than purely commercial outcomes.

Choosing between these ownership types requires understanding their trade-offs. Privately owned banks offer personalized service but limited scale; publicly traded banks provide access to resources but prioritize shareholder returns; government-owned banks advance public interests but may lack agility. For consumers, the decision hinges on individual needs—whether it’s tailored financial solutions, competitive rates, or alignment with societal goals. Investors, meanwhile, must weigh risk tolerance, ethical considerations, and growth potential. In essence, the ownership structure of a bank is not merely a legal detail but a defining factor in its identity and impact.

Corporation for Banking: Is It Necessary?

You may want to see also

Explore related products

![]()

Regulatory Oversight: Banks operate under strict financial regulations and organizational compliance standards

Banks are unequivocally classified as companies, typically structured as corporations or public limited companies, but their operational framework diverges sharply from other corporate entities due to the stringent regulatory oversight they face. Unlike tech startups or retail chains, banks are not merely profit-driven enterprises; they are custodians of public trust, managing trillions in assets and serving as the backbone of global economies. This dual role necessitates a regulatory environment that balances innovation with stability, ensuring banks neither collapse nor exploit their systemic importance.

Consider the Basel Accords, a series of international banking regulations that dictate capital requirements, stress testing, and risk management frameworks. Basel III, for instance, mandates that banks maintain a minimum Common Equity Tier 1 (CET1) capital ratio of 4.5%, supplemented by a capital conservation buffer of 2.5%. These aren’t mere suggestions—they’re enforceable standards backed by penalties, including fines, operational restrictions, and even license revocation. Such regulations are designed to prevent a repeat of crises like 2008, where undercapitalized banks triggered a global recession.

Compliance isn’t just about capital, though. Banks must adhere to anti-money laundering (AML) laws, such as the U.S. Bank Secrecy Act or the EU’s 5th Anti-Money Laundering Directive, which require rigorous customer due diligence and transaction monitoring. Failure to comply can result in astronomical fines—HSBC, for example, paid $1.9 billion in 2012 for AML violations. These regulations extend to data privacy, with frameworks like GDPR in Europe mandating strict protections for customer information, under threat of fines up to 4% of global turnover.

The organizational structure of banks reflects this regulatory burden. Compliance departments are no longer back-office functions but critical divisions with direct board-level oversight. Chief Compliance Officers (CCOs) wield significant authority, ensuring every product, service, and transaction aligns with legal standards. This internal governance is complemented by external auditors and regulators, such as the Federal Reserve in the U.S. or the Prudential Regulation Authority in the U.K., who conduct periodic inspections and stress tests.

For consumers and investors, this regulatory framework offers both reassurance and complexity. While it safeguards deposits (up to $250,000 in the U.S. via FDIC insurance) and promotes transparency, it also limits banks’ agility. Innovations like cryptocurrency or peer-to-peer lending often face regulatory headwinds, as banks must navigate compliance before adoption. Yet, this trade-off is intentional—regulatory oversight ensures banks remain companies with a purpose beyond profit, anchoring financial systems in accountability and public welfare.

Reporting Fraud in HDFC Bank: A Step-by-Step Guide to Protect Your Account

You may want to see also

Explore related products

![]()

Business Model: Focused on financial services, banks function as profit-driven companies or public organizations

Banks, at their core, are financial institutions that operate within a distinct business model centered on providing a range of financial services. This model is characterized by a dual nature: banks can function as either profit-driven companies or public organizations, each with its own set of objectives, structures, and regulatory frameworks. Understanding this duality is crucial for grasping how banks contribute to the economy and serve their stakeholders.

Consider the profit-driven model, where banks operate as companies focused on maximizing shareholder value. These institutions generate revenue through interest on loans, fees for services, and investment activities. For instance, commercial banks like JPMorgan Chase and HSBC exemplify this approach, offering products such as mortgages, credit cards, and wealth management services. Their success is measured by financial metrics like return on equity (ROE) and net interest margin (NIM). To thrive, these banks must balance risk and reward, often employing sophisticated risk management tools and adhering to stringent regulatory requirements like Basel III accords, which mandate minimum capital ratios (e.g., 8% for Tier 1 capital) to ensure stability.

In contrast, public or state-owned banks prioritize societal goals over profit, often focusing on financial inclusion, economic development, and stability. Examples include Germany’s KfW Bank and India’s State Bank of India. These institutions may offer subsidized loans to small businesses, farmers, or low-income households, even if such activities yield lower returns. Their funding often comes from government allocations or central bank support, allowing them to operate with a longer-term, public-interest perspective. Unlike profit-driven banks, their performance is evaluated based on metrics like outreach to underserved populations or contributions to GDP growth.

The distinction between these models is not always clear-cut. Hybrid banks, such as cooperative banks or credit unions, blend profit-driven operations with member-focused services. For example, credit unions like Navy Federal Credit Union in the U.S. return profits to members through lower fees and better interest rates, while still maintaining financial sustainability. This model highlights how banks can adapt their business structures to meet specific community needs without sacrificing stability.

In practice, the choice of model impacts how banks allocate resources, manage risks, and interact with customers. Profit-driven banks may prioritize innovation, such as investing in digital banking platforms to enhance customer experience and reduce operational costs. Public banks, on the other hand, might focus on infrastructure projects or crisis response, as seen during the 2008 financial crisis when many state-owned banks played a pivotal role in stabilizing economies. For individuals and businesses, understanding these differences can guide decisions on where to bank, invest, or seek financial support.

Ultimately, whether a bank operates as a company or a public organization, its business model is inherently tied to the broader financial ecosystem. Both models have unique strengths and challenges, and their coexistence ensures a diversified and resilient financial sector. By focusing on financial services, banks—regardless of their structure—play a critical role in facilitating economic activity, managing risk, and fostering growth.

Currency Exchange: 7 Bank's Fees and Charges Explained

You may want to see also

Explore related products

$14.38

![]()

Classification: Legally, banks are companies but often categorized as financial institutions or organizations

Banks, by legal definition, are companies—entities formed to engage in business activities with the aim of generating profit. This classification is rooted in corporate law, where banks are incorporated under specific statutes, issue shares, and operate under a board of directors. For instance, in the United States, banks are chartered under federal or state laws, such as the National Bank Act, which treats them as corporate entities subject to taxation, regulation, and shareholder accountability. This legal framework ensures banks adhere to the same corporate governance standards as other businesses, including annual reporting and fiduciary responsibilities.

However, the practical categorization of banks often diverges from their legal status. They are universally recognized as financial institutions, a label that emphasizes their role in managing money, credit, and financial services rather than their corporate structure. This classification stems from their core functions: accepting deposits, granting loans, and facilitating payments. For example, the Basel Committee on Banking Supervision regulates banks globally as financial institutions, focusing on capital adequacy and risk management, not corporate governance. This dual identity—legal company and functional institution—reflects the unique intersection of commerce and public trust that banks occupy.

The distinction between "company" and "financial institution" becomes critical in regulatory contexts. As companies, banks are subject to general business laws, such as antitrust regulations and labor standards. Yet, as financial institutions, they face additional oversight from bodies like the Federal Reserve or the European Central Bank, which monitor systemic risk and consumer protection. This layered regulation acknowledges that banks, unlike typical companies, play a pivotal role in economic stability. For instance, the 2008 financial crisis led to stricter capital requirements for banks as financial institutions, not as generic companies, underscoring their systemic importance.

From a consumer perspective, the classification of banks as organizations rather than mere companies highlights their societal role. Banks are not just profit-driven entities but also stewards of public funds and enablers of economic activity. This perception is reinforced by their involvement in government initiatives, such as small business lending programs or mortgage guarantees. For example, during the COVID-19 pandemic, banks were often categorized as essential services, operating under public health guidelines to ensure financial continuity. This organizational role distinguishes them from other companies, which may not bear the same level of public responsibility.

In conclusion, while banks are legally companies, their classification as financial institutions or organizations better captures their multifaceted nature. This dual identity shapes how they are regulated, perceived, and held accountable. Understanding this distinction is crucial for policymakers, investors, and consumers alike, as it clarifies the unique blend of commercial and public interests that banks embody. Whether viewed through a legal, regulatory, or societal lens, banks remain a special case—companies in form, but institutions in function.

Short Selling Bank Stocks in Australia: A Step-by-Step Guide

You may want to see also

Frequently asked questions

A bank is both a company and an organization. It is a financial institution that operates as a business entity (company) while also functioning as an organized structure (organization) to provide banking services.

A bank is typically classified as a financial services company, specifically operating within the banking and financial sector. It is often structured as a corporation, whether public or private.

Generally, no. Most banks are for-profit companies aimed at generating revenue and profits for shareholders. However, there are some specialized banks, like credit unions or community development banks, that may operate as non-profit organizations with a focus on serving specific communities.