Recent rumors and market speculation have sparked discussions about a potential acquisition of Huntington Bank by U.S. Bank. While neither institution has confirmed these reports, analysts suggest that such a merger could significantly reshape the banking landscape, particularly in the Midwest region. U.S. Bank, already a major player in the industry, could expand its footprint and enhance its market share by acquiring Huntington, known for its strong regional presence and customer-focused services. However, regulatory hurdles and the complexities of integrating two large financial institutions remain key considerations. As investors and industry observers await official statements, the potential deal underscores broader trends of consolidation in the banking sector.

| Characteristics | Values |

|---|---|

| Current Status | No official confirmation or announcement from U.S. Bank or Huntington Bank regarding a potential acquisition as of October 2023. |

| Rumor Source | Speculations primarily stem from industry analysts and financial news outlets, not official statements. |

| Market Context | Banking sector consolidation is ongoing, with recent mergers (e.g., PNC-BBVA USA) fueling speculation about potential deals. |

| Strategic Rationale | A merger could expand U.S. Bank's Midwest presence and enhance its retail and commercial banking footprint. |

| Financial Metrics | Huntington Bank (HBAN) market cap: ~$18 billion (as of Oct 2023); U.S. Bank (USB) market cap: ~$75 billion. |

| Regulatory Hurdles | Likely scrutiny from regulators due to combined market share in key regions, particularly Ohio and the Midwest. |

| Recent Developments | No public filings (e.g., SEC) or press releases indicating negotiations or due diligence. |

| Industry Sentiment | Analysts remain divided; some view it as plausible, while others cite U.S. Bank's focus on organic growth post-MUFG Union Bank acquisition (2022). |

| Huntington's Position | Huntington has emphasized its standalone growth strategy in recent earnings calls, with no mention of merger talks. |

| Last Verified Update | As of October 2023, no credible sources confirm active negotiations or a pending deal. |

Explore related products

What You'll Learn

- US Bank's Acquisition Strategy: Recent trends and potential targets in the banking sector

- Huntington Bank's Financial Health: Current assets, liabilities, and market position analysis

- Regulatory Hurdles: Potential challenges from federal and state banking authorities

- Market Reactions: Investor and stakeholder responses to merger rumors

- Synergy Opportunities: Possible benefits of combining US Bank and Huntington Bank operations

![]()

US Bank's Acquisition Strategy: Recent trends and potential targets in the banking sector

As of recent developments, U.S. Bank has been strategically expanding its footprint through acquisitions, with a notable focus on regional banks that enhance its market presence and technological capabilities. While there is no definitive evidence that U.S. Bank is actively pursuing Huntington Bank, the broader trend of consolidation in the banking sector suggests that such a move could align with U.S. Bank’s growth strategy. Huntington Bank, with its strong Midwest presence and digital banking innovations, would complement U.S. Bank’s existing operations, particularly in markets where U.S. Bank seeks to deepen its customer base. This hypothetical acquisition would mirror recent industry trends, such as PNC’s purchase of BBVA USA, which aimed to bolster regional dominance and digital offerings.

Analyzing U.S. Bank’s recent acquisitions reveals a pattern of targeting institutions that offer geographic expansion or technological synergies. For instance, its 2021 acquisition of MUFG Union Bank added $100 billion in assets and strengthened its West Coast presence. If U.S. Bank were to consider Huntington Bank, the rationale would likely center on Huntington’s robust commercial banking platform and its digital tools, such as The Hub, which caters to small businesses. Such a move would not only expand U.S. Bank’s commercial banking capabilities but also position it as a leader in digital financial services, a critical differentiator in today’s competitive landscape.

From a strategic standpoint, acquiring Huntington Bank would require careful regulatory navigation, as the Biden administration has tightened scrutiny on bank mergers to prevent market concentration. U.S. Bank would need to demonstrate how the merger benefits consumers, such as through expanded access to financial services or improved product offerings. Additionally, integrating Huntington’s culture and systems into U.S. Bank’s framework would be a significant operational challenge, requiring a phased approach to ensure minimal disruption to customers and employees.

Comparatively, other potential targets for U.S. Bank include regional banks like Fifth Third Bancorp or KeyCorp, which also offer geographic and product synergies. However, Huntington Bank stands out due to its scale ($175 billion in assets) and its focus on digital transformation, aligning with U.S. Bank’s long-term vision. While no acquisition is without risk, the potential rewards—increased market share, enhanced digital capabilities, and diversified revenue streams—make Huntington Bank a compelling candidate for U.S. Bank’s consideration.

In conclusion, while there is no confirmed interest from U.S. Bank in acquiring Huntington Bank, the strategic fit and industry trends suggest it could be a logical next step. For investors and industry observers, monitoring U.S. Bank’s acquisition strategy and regulatory environment will provide insights into its future moves. As the banking sector continues to consolidate, institutions like Huntington Bank that offer both scale and innovation will remain attractive targets for larger players seeking to stay competitive in a rapidly evolving market.

PNC Bank Wire Transfer Fees: What You Need to Know

You may want to see also

Explore related products

![]()

Huntington Bank's Financial Health: Current assets, liabilities, and market position analysis

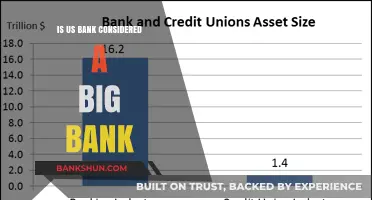

As of the latest financial reports, Huntington Bank's asset composition reveals a robust foundation, with total assets exceeding $175 billion. This figure is a critical indicator of the bank's financial health, showcasing its capacity to manage operations, invest in growth, and withstand economic fluctuations. Current assets, including cash, cash equivalents, and short-term investments, account for approximately 15% of the total, providing liquidity to meet immediate obligations. However, a deeper analysis of these assets’ quality and diversification is essential to gauge their true value in a potential acquisition scenario.

Liabilities, on the other hand, paint a more nuanced picture. Huntington’s total liabilities stand at around $155 billion, with customer deposits representing the largest portion. While this reflects strong customer trust, the bank’s loan-to-deposit ratio of 85% suggests a reliance on deposit funding for lending activities. A closer examination of long-term debt and contingent liabilities is crucial, as these could impact the bank’s attractiveness to a buyer like U.S. Bank. For instance, if Huntington’s debt obligations are structured with high interest rates or near-term maturities, it could pose integration challenges for a potential acquirer.

Market position analysis highlights Huntington’s stronghold in the Midwest, particularly in Ohio, Michigan, and Indiana. This regional dominance is both an asset and a liability. While it provides a stable customer base and operational efficiency, it limits geographic diversification—a factor U.S. Bank might consider if expansion into these markets is a strategic priority. Huntington’s market share in commercial and retail banking, coupled with its digital transformation initiatives, positions it as a competitive player, but its relatively smaller scale compared to U.S. Bank could make it an appealing target for consolidation.

To assess Huntington’s financial health comprehensively, investors and analysts should focus on key metrics such as the efficiency ratio (currently around 60%), return on assets (ROA) of approximately 1.2%, and capital adequacy ratios exceeding regulatory requirements. These indicators suggest operational efficiency and profitability, though they also highlight areas for improvement, such as reducing non-interest expenses. For U.S. Bank, these metrics provide a benchmark to evaluate synergies and potential cost savings post-acquisition.

In conclusion, Huntington Bank’s financial health is characterized by a solid asset base, manageable liabilities, and a strong regional market position. While its Midwest focus and asset quality make it an attractive target, potential acquirers must carefully evaluate its liabilities and growth prospects. For U.S. Bank, the decision to acquire Huntington would hinge on strategic alignment, financial synergies, and the ability to leverage Huntington’s strengths while mitigating its limitations.

Master SBI Bank Exam Preparation: Strategies, Tips, and Study Plan

You may want to see also

Explore related products

![]()

Regulatory Hurdles: Potential challenges from federal and state banking authorities

A merger between U.S. Bank and Huntington Bank would create a financial institution with a significant footprint, potentially triggering intense scrutiny from federal and state regulators. The primary concern for authorities would be the impact on market competition, particularly in regions where both banks have a strong presence. The Department of Justice (DOJ) and the Federal Reserve would likely examine whether the combined entity would dominate local markets, leading to reduced consumer choice and potentially higher fees. For instance, in the Midwest, where both banks operate extensively, a merger could result in a substantial market share, raising antitrust concerns.

One of the key regulatory challenges would be obtaining approval from the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC). These agencies would assess the financial stability of the merged entity and its compliance with banking laws. Given the size of the transaction, regulators would scrutinize the banks' capital adequacy, risk management practices, and potential systemic risks. Any perceived weaknesses in these areas could delay or even derail the merger. For example, if the combined bank’s leverage ratio falls below regulatory thresholds, authorities might require divestitures or additional capital injections before approving the deal.

State banking regulators would also play a critical role, particularly in states where the merger could significantly alter the competitive landscape. In Ohio, where Huntington Bank is headquartered, state authorities would likely evaluate the impact on local communities, including access to credit and banking services. Similarly, in Minnesota, U.S. Bank’s home state, regulators would assess whether the merger aligns with state-specific banking regulations. Disparities in state laws could complicate the approval process, as the banks would need to navigate varying requirements across multiple jurisdictions.

Another potential hurdle is the Community Reinvestment Act (CRA), which requires banks to meet the credit needs of the communities they serve. Regulators would examine whether the merged entity would continue to provide adequate lending and services in underserved areas. If the merger is perceived to disproportionately benefit wealthier regions at the expense of low-income communities, it could face opposition from both regulators and advocacy groups. To mitigate this risk, the banks might need to commit to specific community investment programs, such as affordable housing initiatives or small business lending, as part of their merger proposal.

Finally, political and public sentiment could influence regulatory decisions. High-profile bank mergers often attract scrutiny from lawmakers and consumer advocacy groups, who may pressure regulators to take a tougher stance. In the current climate, where concerns about financial consolidation are heightened, U.S. Bank and Huntington Bank would need to proactively address these concerns through transparent communication and demonstrable benefits to consumers. Without a compelling case for how the merger would enhance competition and serve the public interest, regulatory approval could remain elusive.

Unlock SBI Corporate Net Banking: A Step-by-Step Guide for Businesses

You may want to see also

Explore related products

![]()

Market Reactions: Investor and stakeholder responses to merger rumors

Merger rumors between U.S. Bank and Huntington Bank sent shockwaves through the financial sector, triggering a cascade of reactions from investors and stakeholders. Stock prices of both institutions experienced immediate volatility, with Huntington shares surging on the prospect of a premium acquisition price, while U.S. Bank shares dipped slightly as investors weighed the potential costs and integration challenges. This knee-jerk reaction underscores the market's inherent sensitivity to M&A speculation, particularly in a consolidating banking landscape.

Analysts scrutinized the strategic rationale behind the rumored merger, debating the potential synergies and cultural fit between the two Midwest-based banks. U.S. Bank's desire to expand its regional footprint and Huntington's strong commercial lending portfolio emerged as key talking points. However, concerns about regulatory hurdles and potential job cuts also surfaced, highlighting the complex web of factors influencing stakeholder sentiment.

Beyond the initial stock price fluctuations, investor and stakeholder responses revealed a spectrum of emotions and strategic considerations. Institutional investors, driven by short-term gains, engaged in speculative trading, amplifying market volatility. Long-term investors, however, adopted a wait-and-see approach, seeking clarity on the deal's financial implications and long-term growth prospects. Employees of both banks, understandably anxious about potential job security, sought reassurance from management, while community groups voiced concerns about the impact on local banking services.

This diverse range of reactions underscores the multifaceted nature of market responses to merger rumors. It's not merely about stock prices; it's about the intricate interplay of financial, strategic, and human factors that shape stakeholder perceptions and ultimately influence the trajectory of the deal.

How to Verify Banks in Flagstar Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Synergy Opportunities: Possible benefits of combining US Bank and Huntington Bank operations

A merger between US Bank and Huntington Bank could unlock significant synergy opportunities, particularly in the realm of operational efficiency and cost reduction. By consolidating overlapping functions such as back-office operations, IT infrastructure, and branch networks, the combined entity could eliminate redundancies and streamline processes. For instance, US Bank’s robust digital banking platform could be integrated with Huntington’s strong regional presence, reducing technology maintenance costs while expanding service reach. Estimates suggest such mergers often achieve cost savings of 10-15% within the first year, primarily through workforce optimization and system integration. This efficiency not only boosts profitability but also frees up resources for reinvestment in customer-facing innovations.

From a market expansion perspective, the merger would create a more geographically diverse and competitive banking powerhouse. US Bank’s dominance in the Midwest and West Coast would complement Huntington’s stronghold in the Rust Belt and Southeast, providing a more balanced national footprint. This expanded reach could enable cross-selling opportunities, such as offering US Bank’s commercial lending expertise to Huntington’s small business clients or introducing Huntington’s specialized mortgage products to US Bank’s customer base. A combined entity would also gain greater negotiating power with vendors and suppliers, further enhancing cost efficiency and service quality.

Another critical synergy lies in leveraging combined data and technology capabilities to enhance customer experience. Huntington’s focus on digital tools for small businesses, such as its business checking accounts with built-in cash flow management, could be integrated into US Bank’s broader suite of financial services. Simultaneously, US Bank’s advanced analytics and AI-driven personalization could elevate Huntington’s customer engagement strategies. For example, the merged entity could deploy predictive analytics to offer tailored financial products, such as auto loans or credit cards, based on individual spending patterns. This data-driven approach would not only increase customer satisfaction but also drive revenue growth through higher product adoption rates.

Finally, the merger could strengthen the combined bank’s risk management and regulatory compliance frameworks. Both institutions have distinct strengths in this area—US Bank in enterprise risk management and Huntington in community banking compliance. By pooling expertise, the merged entity could develop a more robust risk assessment model, better equipped to navigate economic uncertainties and regulatory changes. For instance, Huntington’s localized risk assessment tools could be scaled nationally through US Bank’s infrastructure, while US Bank’s stress testing methodologies could enhance Huntington’s resilience. This synergy would not only protect the bank’s financial health but also position it as a leader in industry best practices.

In conclusion, the potential merger of US Bank and Huntington Bank presents a compelling case for synergy, offering operational efficiencies, market expansion, technological innovation, and strengthened risk management. While challenges such as cultural integration and regulatory approval remain, the strategic benefits of combining these institutions could create a more resilient, customer-centric, and competitive banking entity. As the financial landscape continues to evolve, such synergies may become essential for sustaining long-term growth and relevance.

Does the Bank of England Buy Gilts? Understanding Quantitative Easing

You may want to see also

Frequently asked questions

As of the latest publicly available information, there is no official confirmation or announcement from US Bank or Huntington Bank regarding a potential acquisition.

Rumors and speculations about US Bank acquiring Huntington Bank have circulated in financial circles, but neither bank has confirmed these claims, and they remain unverified.

If a merger were to occur, customers could expect changes in branch locations, account terms, and services. However, since there is no confirmed deal, any potential impact remains speculative.