Traditional banking, while a cornerstone of the financial system, comes with significant costs that impact both consumers and institutions. For individuals, these costs often include high fees for services such as account maintenance, overdrafts, wire transfers, and ATM usage, which can disproportionately affect low-income customers. Additionally, traditional banks typically offer lower interest rates on savings accounts and higher rates on loans, reducing the financial benefits for depositors and increasing borrowing expenses. For banks themselves, maintaining physical branches, extensive staff, and legacy systems incurs substantial operational expenses, which are often passed on to customers. These inefficiencies, combined with limited accessibility in underserved areas, highlight the financial and structural burdens of traditional banking, prompting a growing shift toward more cost-effective digital alternatives.

Explore related products

What You'll Learn

- High overhead costs from physical branches and large staff

- Expensive maintenance of legacy banking systems and infrastructure

- Significant fees for customers on transactions and account services

- Inefficient processes leading to higher operational and time costs

- Limited accessibility, requiring customers to incur travel and time expenses

![]()

High overhead costs from physical branches and large staff

Physical branches are the backbone of traditional banking, but they come with a hefty price tag. Rent, utilities, maintenance, and security for these locations constitute a significant portion of a bank's operational expenses. For instance, a single branch in a prime urban location can cost upwards of $500,000 annually in rent alone, not including the additional costs of staffing and technology. These fixed costs are a constant drain on resources, regardless of the volume of transactions or customer footfall.

Consider the staffing requirements of a traditional bank. Each branch typically employs tellers, customer service representatives, managers, and security personnel. The average salary for a bank teller in the United States is around $30,000 per year, and when multiplied by the number of employees across multiple branches, the labor costs escalate rapidly. Moreover, banks often invest in extensive training programs to ensure compliance with regulations and maintain service quality, adding another layer of expense. This labor-intensive model contrasts sharply with digital banking, where automation and AI handle many routine tasks at a fraction of the cost.

A comparative analysis reveals the inefficiencies of this model. While a physical branch may serve a few hundred customers daily, a digital platform can handle millions of transactions simultaneously with minimal human intervention. For example, a study by McKinsey found that traditional banks spend approximately 60% of their operating costs on branch networks and personnel, compared to just 20% for digital-first banks. This disparity highlights the unsustainable nature of relying heavily on physical infrastructure in an increasingly digital world.

To mitigate these costs, banks must adopt a hybrid approach. Reducing the number of branches and reallocating resources to digital channels can significantly lower overhead. For instance, some banks have successfully implemented "branch-lite" models, where smaller, tech-enabled locations focus on high-value interactions while directing routine transactions online. This strategy not only cuts costs but also enhances customer experience by offering flexibility and convenience. However, such transitions require careful planning to avoid alienating customers who still prefer in-person services.

In conclusion, the high overhead costs associated with physical branches and large staff are a critical challenge for traditional banks. By analyzing the financial burden of maintaining these assets and comparing them with digital alternatives, it becomes clear that a strategic shift is necessary. Banks that embrace innovation while thoughtfully reducing their physical footprint can achieve cost efficiency without compromising service quality. The key lies in balancing tradition with technology to create a sustainable and customer-centric banking model.

KeyBank CD Rates: Competitive or Not?

You may want to see also

Explore related products

![]()

Expensive maintenance of legacy banking systems and infrastructure

Legacy banking systems, often decades old, are financial institutions’ silent profit drains. Their maintenance consumes a staggering portion of IT budgets, with estimates suggesting up to 80% allocated to keeping these outdated behemoths functional. This leaves a mere fraction for innovation, hindering banks' ability to compete in a rapidly evolving digital landscape.

Imagine a car manufacturer still relying on assembly lines from the 1980s. The inefficiency and cost of maintaining such antiquated machinery would be crippling. The same principle applies to banking. Legacy systems, built on outdated programming languages and architectures, are notoriously difficult and expensive to update, patch, and secure.

The true cost extends beyond direct maintenance fees. These systems are often incompatible with modern technologies, limiting banks' ability to offer seamless digital experiences demanded by today's customers. Think clunky online banking platforms, slow transaction processing times, and limited integration with third-party financial tools. This friction leads to customer dissatisfaction, churn, and ultimately, lost revenue.

A 2022 study by McKinsey revealed that banks with modernized core systems achieve 20% higher customer satisfaction scores and 15% lower operating costs compared to their legacy-bound counterparts. This highlights the direct correlation between outdated infrastructure and financial performance.

The security risks posed by legacy systems are equally alarming. Outdated software is more vulnerable to cyberattacks, leaving customer data and financial assets exposed. The average cost of a data breach in the financial sector exceeds $5 million, a price tag that could cripple smaller institutions. Investing in modern, secure infrastructure is not just a matter of efficiency, but of survival in an increasingly hostile digital environment.

Breaking free from the legacy system shackles requires a multi-pronged approach. Banks must prioritize gradual modernization, replacing outdated components with modular, cloud-based solutions that offer scalability, flexibility, and enhanced security. While the initial investment may seem daunting, the long-term benefits – reduced costs, improved customer experience, and mitigated risks – far outweigh the upfront expense. The future of banking belongs to those who embrace innovation, leaving the costly burdens of the past behind.

Should You Switch Banks for a Rollover IRA? Pros and Cons

You may want to see also

Explore related products

![]()

Significant fees for customers on transactions and account services

Traditional banking often imposes a myriad of fees that can erode customers’ finances over time. From monthly maintenance charges to overdraft penalties, these costs add up, making it essential for account holders to scrutinize their statements regularly. For instance, a typical checking account may charge a $12 monthly fee, which equates to $144 annually—money that could otherwise be saved or invested. Understanding these fees is the first step toward minimizing their impact on your financial health.

Consider the overdraft fee, a common yet costly charge that occurs when a transaction exceeds the available balance. Banks often charge between $30 and $35 per overdraft, and some institutions allow multiple overdrafts in a single day, compounding the expense. For example, a $5 coffee purchase could result in a $35 fee, turning a small indulgence into a costly mistake. To avoid this, monitor your balance closely, set up low-balance alerts, or link your account to a savings account for automatic transfers.

Transaction fees are another area where traditional banks nickel-and-dime customers. Wire transfers, for instance, can cost anywhere from $15 to $50 domestically and even more internationally. Similarly, using out-of-network ATMs often incurs a $2 to $5 fee per transaction. While these amounts may seem insignificant individually, they can accumulate quickly, especially for those who frequently travel or rely on cash. Opting for in-network ATMs and exploring fee-free alternatives, such as online banks, can significantly reduce these expenses.

Account service fees also vary widely depending on the type of account and bank. Premium accounts may offer perks like waived fees, but they often require high minimum balances—sometimes $1,500 or more—to avoid monthly charges. Conversely, basic accounts may have lower balance requirements but come with limited features and higher fees for additional services. Evaluate your banking needs carefully: if you rarely use certain services, consider downgrading to a simpler account to save on unnecessary costs.

The cumulative effect of these fees underscores the importance of proactive financial management. By understanding the fee structure of your bank and adopting strategies to avoid unnecessary charges, you can retain more of your hard-earned money. For instance, switching to a no-fee online bank or credit union could save the average customer hundreds of dollars annually. In a world where every dollar counts, being mindful of these costs is not just prudent—it’s essential.

Locate Your Bank Branch Easily: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Inefficient processes leading to higher operational and time costs

Traditional banking systems often rely on manual, paper-based processes that are inherently inefficient. Consider the typical loan application journey: customers submit physical documents, which are then manually verified, processed, and approved by multiple departments. This not only slows down decision-making but also increases the likelihood of errors, requiring additional time for corrections. For instance, a simple mortgage application can take anywhere from 30 to 45 days to process, during which customers and bank staff alike are burdened by delays. Such inefficiencies directly translate to higher operational costs, as banks must allocate more resources—both human and material—to manage these cumbersome workflows.

To illustrate, let’s break down the steps involved in processing a check deposit. First, the customer fills out a deposit slip, which is then handed to a teller. The teller manually verifies the details, endorses the check, and updates the account balance. Next, the check is physically transported to a central processing unit, where it is scanned, cleared, and settled. Each step introduces potential bottlenecks, from human error in data entry to delays in transportation. In contrast, digital banking systems can process the same transaction in minutes, eliminating the need for physical handling and reducing operational costs by up to 50% in some cases.

Inefficient processes also impose hidden time costs on customers, eroding their satisfaction and loyalty. For example, standing in long queues at a bank branch or waiting days for a transaction to clear are common pain points. A study by McKinsey found that customers value their time at an average of $20 per hour, meaning a 30-minute wait at a branch effectively costs the customer $10—a cost indirectly borne by the bank in terms of lost goodwill. Multiply this by thousands of customers daily, and the cumulative impact on a bank’s reputation and retention rates becomes significant.

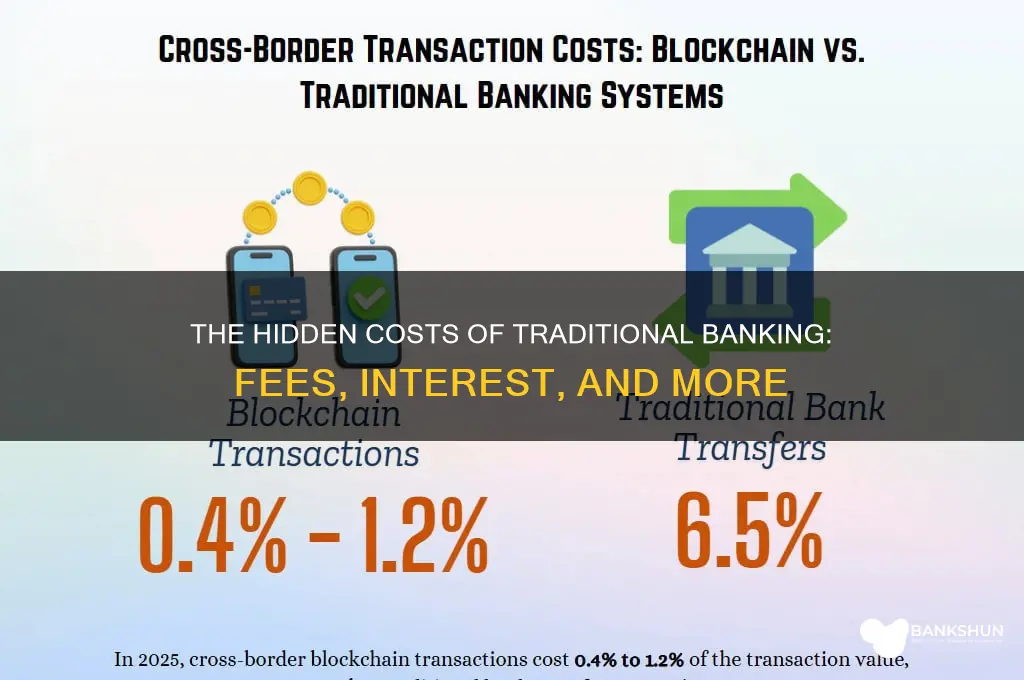

Addressing these inefficiencies requires a strategic shift toward automation and digitization. Banks can start by implementing robotic process automation (RPA) for repetitive tasks like data entry and document verification. For instance, RPA bots can process loan applications 70% faster than manual methods, reducing operational costs by up to 30%. Additionally, adopting blockchain technology for transactions can eliminate intermediaries, speeding up settlement times from days to seconds. While the initial investment in such technologies may be high, the long-term savings in operational and time costs make it a compelling proposition.

Finally, banks must prioritize customer-centric process redesign. For example, introducing mobile banking apps with features like instant fund transfers, digital document uploads, and real-time transaction tracking can drastically reduce customer wait times. A case in point is a European bank that reduced its average transaction time from 15 minutes to 2 minutes after launching a fully digital platform, resulting in a 25% increase in customer satisfaction scores. By focusing on efficiency, banks can not only cut costs but also enhance the overall customer experience, ensuring long-term competitiveness in a rapidly evolving financial landscape.

Venezuela's Central Bank: Independent or Government-Controlled?

You may want to see also

Explore related products

![]()

Limited accessibility, requiring customers to incur travel and time expenses

Traditional banking often confines customers to physical branches, a limitation that imposes tangible costs in both time and money. Consider the average commute: in urban areas, traveling to a bank can take 30 minutes to an hour, depending on traffic and public transit schedules. For rural customers, the journey might extend to two hours or more. These travel times are not trivial; they represent lost productivity, especially for working professionals or caregivers. When compounded over multiple visits—whether for routine transactions, loan consultations, or dispute resolutions—the cumulative hours become a significant burden.

The financial costs of these trips are equally noteworthy. A round trip to a bank branch can cost anywhere from $5 to $20 in fuel, parking, or public transit fares. For customers on fixed incomes or tight budgets, these expenses are not insignificant. Over a year, someone visiting a branch once a month could spend $60 to $240 solely on travel. This doesn’t account for indirect costs, such as missed work hours or the need to arrange childcare. For small business owners, the opportunity cost of time spent traveling to a bank can dwarf the direct expenses, as it diverts attention from revenue-generating activities.

Contrast this with digital banking, where accessibility is nearly instantaneous. A mobile app or online portal eliminates the need for physical travel, allowing customers to manage accounts, transfer funds, or apply for loans from anywhere. This shift not only saves time but also reduces carbon footprints, aligning with growing environmental consciousness. Traditional banks that fail to offer robust digital alternatives risk alienating tech-savvy customers, particularly younger demographics who prioritize convenience and efficiency.

To mitigate these costs, customers can adopt a hybrid approach, reserving branch visits for complex needs while leveraging digital tools for routine tasks. For instance, using ATMs for cash withdrawals or mobile apps for balance checks can minimize travel frequency. However, this solution is only viable if banks invest in seamless digital infrastructure and maintain extended customer service hours. Without such adaptations, the accessibility gap will persist, disproportionately affecting those in remote areas or with limited mobility.

Ultimately, the travel and time expenses associated with traditional banking are more than mere inconveniences—they are barriers to financial inclusion. As the world moves toward greater digital integration, banks must reevaluate their physical footprints and prioritize accessibility in all its forms. Until then, customers will continue to bear the hidden costs of a system ill-suited to modern demands.

Understanding Bank of Ghana's Monetary Policy Implementation Strategies

You may want to see also

Frequently asked questions

Traditional banking often includes fees such as monthly maintenance charges, overdraft fees, ATM fees (for out-of-network use), wire transfer fees, and paper statement fees.

Traditional banks may charge monthly maintenance fees for checking and savings accounts unless certain conditions are met, such as maintaining a minimum balance or setting up direct deposits.

While debit cards are often free to use, credit cards from traditional banks may come with annual fees, late payment fees, cash advance fees, and foreign transaction fees.

Yes, traditional banks charge fees for loan services, including origination fees, late payment fees, prepayment penalties (in some cases), and interest rates based on creditworthiness.