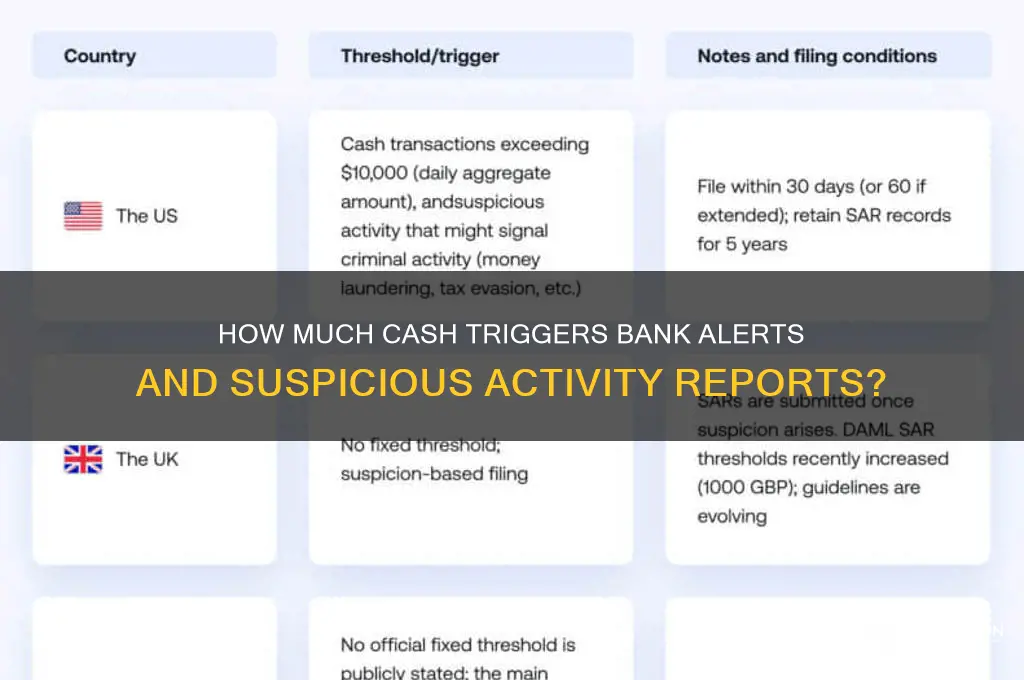

Banks employ sophisticated monitoring systems to detect and flag unusual or suspicious transactions, including cash deposits and withdrawals, as part of their anti-money laundering (AML) and fraud prevention efforts. The specific cash amount that triggers a flag varies by institution, jurisdiction, and regulatory requirements, but generally, transactions exceeding a certain threshold, often $10,000 in the United States, are subject to closer scrutiny. This threshold is based on the Bank Secrecy Act (BSA), which mandates financial institutions to report transactions involving this amount or more to the Financial Crimes Enforcement Network (FinCEN). However, banks may also flag smaller amounts if they appear inconsistent with a customer’s typical behavior, involve structured transactions designed to evade reporting, or raise other red flags. Ultimately, the goal is to identify potential illegal activities while ensuring legitimate transactions are not unnecessarily disrupted.

Explore related products

What You'll Learn

- Transaction Size Thresholds: Banks flag transactions exceeding predefined cash limits, varying by institution and account type

- Frequent Large Deposits: Repeated large cash deposits trigger alerts for potential suspicious activity monitoring

- Structuring Detection: Splitting large sums into smaller deposits to evade reporting is flagged as structuring

- Cash Withdrawal Patterns: Unusual or sudden large cash withdrawals are monitored for potential illicit purposes

- International Cash Transfers: Cross-border cash transactions above certain thresholds are flagged for regulatory compliance checks

![]()

Transaction Size Thresholds: Banks flag transactions exceeding predefined cash limits, varying by institution and account type

Banks employ transaction size thresholds as a critical tool in their anti-money laundering (AML) and fraud detection arsenals. These thresholds, often shrouded in deliberate opacity for security reasons, act as tripwires, triggering alerts when cash transactions surpass predetermined limits. While the specific figures vary depending on the bank, account type, and even geographical location, understanding the general landscape can empower individuals and businesses to navigate financial transactions with greater awareness.

Imagine depositing $10,000 in cash into your personal checking account. This seemingly innocuous act could potentially raise a red flag with your bank. Many institutions in the United States, for instance, are required by the Bank Secrecy Act to report any cash transaction exceeding $10,000 to the Financial Crimes Enforcement Network (FinCEN). This doesn't automatically imply wrongdoing, but it highlights the sensitivity surrounding large cash movements.

The rationale behind these thresholds is twofold. Firstly, they aim to deter illicit activities like money laundering, where criminals attempt to disguise the origins of illegally obtained funds. Large cash transactions can be a telltale sign of such activities. Secondly, they help banks identify potential fraud, protecting both the institution and its customers. A sudden, unusually large cash deposit or withdrawal could indicate unauthorized access to an account.

It's crucial to remember that these thresholds aren't one-size-fits-all. Business accounts, for example, often enjoy higher limits compared to personal accounts, reflecting the typically larger cash flows associated with commercial activities. Similarly, high-net-worth individuals might have customized thresholds based on their financial profiles.

Transparency is key when dealing with transactions nearing or exceeding these limits. Proactively informing your bank about the source and purpose of a large cash transaction can prevent unnecessary scrutiny and potential delays. Maintaining clear and accurate records is equally important, providing a paper trail that substantiates the legitimacy of the transaction.

Could a Modern Bank Run Threaten Financial Stability Again?

You may want to see also

Explore related products

![]()

Frequent Large Deposits: Repeated large cash deposits trigger alerts for potential suspicious activity monitoring

Banks are required by law to monitor and report transactions that may indicate money laundering, tax evasion, or other illicit activities. One red flag that often triggers their alert systems is the pattern of frequent large cash deposits. While the specific threshold varies by institution and jurisdiction, amounts exceeding $10,000 in a single transaction or a series of smaller deposits that cumulatively surpass this limit within a short period are typically scrutinized. For instance, depositing $9,000 in cash every week for several weeks could raise suspicions, even if each individual deposit falls below the reporting threshold.

The rationale behind this monitoring is straightforward: legitimate businesses and individuals rarely deal in large cash transactions repeatedly. Frequent large deposits may suggest an attempt to avoid reporting requirements, known as "structuring," or could indicate proceeds from illegal activities. Banks use sophisticated algorithms to detect such patterns, cross-referencing transaction histories, account types, and customer profiles to assess risk. For example, a small retail business might justify regular cash deposits as part of its daily operations, but an individual with no apparent source of income making similar deposits would likely face closer examination.

If you find yourself needing to deposit large amounts of cash frequently, transparency is key. Document the source of the funds and be prepared to explain the reason for the transactions to your bank. For businesses, maintaining detailed records of cash sales and expenses can help demonstrate legitimacy. Individuals inheriting cash, selling high-value items, or receiving large gifts should retain documentation such as wills, sales receipts, or gift letters. Proactive communication with your bank can prevent unnecessary scrutiny and ensure compliance with regulatory requirements.

It’s also worth noting that banks are not the only entities monitoring these transactions. Financial intelligence units and law enforcement agencies receive reports of suspicious activity, which may lead to investigations. While the intent behind frequent large deposits may be entirely lawful, the consequences of failing to address concerns can be severe, including account freezes, fines, or legal action. Understanding these thresholds and the reasoning behind them empowers individuals and businesses to navigate the financial system responsibly while minimizing the risk of unintended complications.

Exploring Huntington Bank's Presence: Is There a Branch in Nepal?

You may want to see also

Explore related products

![]()

Structuring Detection: Splitting large sums into smaller deposits to evade reporting is flagged as structuring

Banks are required by law to report cash transactions exceeding $10,000 to the Financial Crimes Enforcement Network (FinCEN) to combat money laundering and other illicit activities. However, some individuals attempt to circumvent this threshold by splitting large sums into smaller deposits, a practice known as structuring. This method involves making multiple cash deposits under $10,000 to avoid triggering the reporting requirement. While it may seem like a clever workaround, structuring is illegal and can lead to severe consequences, including fines, imprisonment, and asset forfeiture.

To detect structuring, banks employ sophisticated monitoring systems and trained personnel who analyze transaction patterns. For instance, if a customer deposits $9,000 in cash on three consecutive days, the bank’s system flags this activity as suspicious. Similarly, frequent deposits just below the reporting threshold, such as $9,500 every week, raise red flags. Banks also scrutinize transactions across multiple accounts or branches, as individuals may attempt to disperse their deposits to avoid detection. It’s crucial to understand that structuring is not just about the amount but the intent to evade reporting requirements.

From a practical standpoint, individuals should be aware of the risks associated with structuring. For example, a small business owner who regularly deposits daily cash earnings of $8,000 may unintentionally trigger suspicion if the pattern appears deliberate. To avoid this, businesses should maintain transparent records and consult with their bank about large cash transactions. If a legitimate reason exists for depositing amounts just under $10,000, documentation and communication with the bank can help prevent misunderstandings. However, deliberately structuring deposits to avoid reporting is a federal offense, regardless of the source of funds.

Comparatively, structuring differs from other suspicious activities like money laundering or terrorist financing, though it often overlaps. While money laundering involves disguising the origins of illicit funds, structuring focuses on evading reporting thresholds. For instance, a drug dealer laundering money might use structuring as one method to hide transactions, but structuring itself can occur with legal funds if the intent is to avoid reporting. This distinction is critical, as even lawful cash transactions can lead to legal trouble if structured improperly.

In conclusion, structuring detection is a key component of banks’ anti-money laundering efforts. By splitting large sums into smaller deposits, individuals may believe they can fly under the radar, but advanced monitoring systems and legal scrutiny make this a high-risk strategy. Whether dealing with personal or business finances, transparency and compliance with reporting requirements are essential. If in doubt about how to handle large cash transactions, seeking guidance from a financial advisor or legal expert is a prudent step to avoid unintended consequences.

Exploring Banks Starting with E: A Comprehensive Guide to Top Options

You may want to see also

Explore related products

![]()

Cash Withdrawal Patterns: Unusual or sudden large cash withdrawals are monitored for potential illicit purposes

Banks are required by law to monitor and report suspicious activities, including unusual cash withdrawal patterns. A single transaction exceeding $10,000 triggers a Currency Transaction Report (CTR) in the United States, but it's not just the amount that raises flags. Sudden, large withdrawals deviating from a customer's normal behavior can prompt further scrutiny, regardless of whether the threshold is met. For instance, an individual who typically withdraws $500 monthly but suddenly takes out $8,000 in cash may attract attention due to the anomaly.

Analyzing these patterns involves sophisticated algorithms and human oversight. Financial institutions employ transaction monitoring systems that use machine learning to detect deviations from established norms. These systems consider factors like frequency, amount, and purpose of withdrawals, cross-referencing them with historical data and risk profiles. A sudden cash withdrawal for a business client might be flagged if it coincides with irregular vendor payments or unusual account activity. Similarly, personal accounts exhibiting sudden large cash withdrawals, especially when coupled with international transactions or rapid fund transfers, can raise red flags for potential money laundering or terrorist financing.

To avoid unnecessary scrutiny, customers should maintain consistent withdrawal habits and provide context for unusual transactions. For example, if planning a large cash purchase, such as a car or wedding expenses, notify the bank in advance. Documentation, like invoices or contracts, can help substantiate the legitimacy of the withdrawal. For businesses, ensuring that large cash withdrawals align with operational needs and maintaining transparent financial records can mitigate the risk of being flagged.

However, it's essential to recognize that banks have a legal obligation to report suspicious activities, even if the customer's intentions are legitimate. In such cases, cooperation with the bank's investigation is crucial. Providing additional information, clarifying the purpose of the withdrawal, and demonstrating a clear audit trail can help resolve concerns promptly. Remember, while large cash withdrawals are not inherently illicit, their sudden or unusual nature can trigger monitoring mechanisms designed to protect the financial system's integrity.

In practice, understanding these monitoring processes empowers customers to navigate the system more effectively. By being aware of the thresholds, patterns, and contextual factors that banks consider, individuals and businesses can minimize the likelihood of being flagged. For instance, staggering large withdrawals over time or using alternative payment methods, like checks or electronic transfers, might be more suitable for certain transactions. Ultimately, fostering transparency and maintaining consistent financial behavior are key to avoiding unnecessary scrutiny while ensuring compliance with regulatory requirements.

Uncovering Bank Robbery Rates: A Comprehensive Guide to Finding Data

You may want to see also

Explore related products

![]()

International Cash Transfers: Cross-border cash transactions above certain thresholds are flagged for regulatory compliance checks

Cross-border cash transfers exceeding $10,000 often trigger regulatory compliance checks by banks, a measure rooted in anti-money laundering (AML) and counter-terrorist financing (CTF) laws. This threshold is not arbitrary; it aligns with international standards set by organizations like the Financial Action Task Force (FATF). When a transaction surpasses this amount, financial institutions are legally obligated to report it to regulatory bodies, such as the Financial Crimes Enforcement Network (FinCEN) in the United States. These reports, known as Currency Transaction Reports (CTRs), help authorities monitor and investigate potentially illicit activities. For individuals and businesses, understanding this threshold is crucial to avoid delays or scrutiny in legitimate transactions.

The process of flagging large international cash transfers involves multiple layers of verification. Banks employ automated systems to detect transactions above the threshold, followed by manual reviews to assess their legitimacy. Customers may be required to provide additional documentation, such as the source of funds, the purpose of the transfer, and the recipient’s identity. While this process can be time-consuming, it serves a vital purpose: preventing financial crimes that exploit cross-border transactions. For instance, a business transferring $15,000 to a supplier in another country might need to submit invoices or contracts to substantiate the transaction. Transparency and preparedness are key to navigating these checks smoothly.

Comparatively, different countries have varying thresholds for flagging international cash transfers, reflecting their unique regulatory environments. In the European Union, for example, transactions exceeding €10,000 are subject to scrutiny, while in Australia, the threshold is AUD 10,000. These differences highlight the importance of researching local regulations when conducting cross-border transactions. Travelers or businesses operating across multiple jurisdictions must remain vigilant to avoid unintentional compliance breaches. For instance, an individual transferring €12,000 from Germany to Spain would face the same level of scrutiny as someone sending $12,000 from the U.S. to Canada, despite the currency difference.

To minimize disruptions, individuals and businesses should adopt proactive strategies when dealing with large international cash transfers. First, plan ahead by initiating transactions well in advance of deadlines, as compliance checks can take several days. Second, maintain detailed records of all transactions, including invoices, contracts, and communication with recipients. Third, consider splitting large transfers into smaller amounts below the threshold, though this must be done transparently and with legitimate intent. Finally, establish a relationship with your bank to facilitate smoother reviews; financial institutions are more likely to expedite checks for trusted customers. By taking these steps, you can ensure compliance while maintaining efficiency in cross-border transactions.

In conclusion, while flagged international cash transfers may seem burdensome, they are a necessary safeguard in the global financial system. Understanding the thresholds, processes, and best practices can transform a potentially frustrating experience into a routine part of international finance. Whether you’re a business owner, expatriate, or occasional traveler, staying informed and prepared is the key to navigating cross-border transactions with confidence. After all, in a world where financial crimes know no borders, compliance checks are not just a legal requirement—they’re a shared responsibility.

Step-by-Step Guide to Adding a Beneficiary in Axis Bank

You may want to see also

Frequently asked questions

Banks often flag cash transactions exceeding $10,000 in a single day or a series of smaller transactions that cumulatively reach this threshold, as required by anti-money laundering (AML) regulations.

Yes, banks may flag smaller cash transactions (e.g., $5,000 or more) if they appear unusual or inconsistent with the account holder’s typical activity, even if they don’t meet the $10,000 reporting threshold.

When a transaction is flagged, the bank may file a Currency Transaction Report (CTR) for amounts over $10,000 or a Suspicious Activity Report (SAR) if the transaction appears suspicious, regardless of the amount. The account holder may also be contacted for additional information.