APIs, or Application Programming Interfaces, have become a cornerstone of modern banking, revolutionizing how financial institutions operate and interact with customers. In the banking sector, APIs act as digital bridges, enabling seamless communication between different software systems, applications, and platforms. They allow banks to offer innovative services, such as mobile banking, real-time payments, and third-party integrations, while ensuring secure and efficient data exchange. By standardizing processes and fostering collaboration, APIs in banking enhance customer experiences, drive operational efficiency, and open new avenues for financial innovation. Understanding what API stands for in banking is essential to grasping the transformative impact of technology on the financial industry.

| Characteristics | Values |

|---|---|

| Acronym | API stands for Application Programming Interface |

| Purpose in Banking | Enables secure communication and data exchange between different software applications, including banking systems, third-party services, and customer applications. |

| Key Functions | 1. Account Information Sharing: Allows authorized third-party apps to access account data (balances, transactions) with customer consent. 2. Payment Initiation: Facilitates secure payment transactions via third-party platforms. 3. Product Comparison: Enables customers to compare banking products (loans, accounts) across providers. 4. Fraud Detection: Integrates advanced analytics tools for real-time fraud monitoring. 5. Customer Onboarding: Streamlines digital account opening processes. |

| Types in Banking | 1. Open Banking APIs: Publicly available, regulated APIs for third-party access (e.g., PSD2 in Europe). 2. Private APIs: Internal APIs for bank-specific applications. 3. Partner APIs: Shared with trusted partners for collaborative services. |

| Security Standards | 1. OAuth 2.0: For secure authorization. 2. HTTPS/TLS: Encryption for data transmission. 3. API Gateways: Manage traffic, enforce policies, and monitor usage. 4. Two-Factor Authentication (2FA): Enhances user verification. |

| Regulations | 1. PSD2 (EU): Mandates open banking APIs for payment services. 2. GDPR (EU): Ensures data privacy and consent management. 3. GLBA (US): Protects consumer financial information. |

| Benefits | 1. Enhanced Customer Experience: Personalized services and seamless integrations. 2. Innovation: Enables fintechs to build on banking infrastructure. 3. Efficiency: Automates processes and reduces manual interventions. 4. Revenue Streams: Creates opportunities for new services and partnerships. |

| Challenges | 1. Security Risks: Potential for data breaches or unauthorized access. 2. Regulatory Compliance: Navigating complex legal requirements. 3. Integration Complexity: Ensuring compatibility with legacy systems. |

| Examples | 1. Plaid: Connects financial apps to bank accounts. 2. Stripe: Facilitates payment processing via APIs. 3. Yodlee: Aggregates financial data for budgeting tools. |

Explore related products

What You'll Learn

- API Definition: Application Programming Interface enables secure data exchange between banking systems and third-party services

- Banking API Types: Open banking, payment, account information, and investment APIs streamline financial operations

- API Benefits: Enhances customer experience, enables innovation, and improves efficiency in banking services

- Security Measures: APIs use encryption, OAuth, and tokenization to protect sensitive banking data

- Regulatory Compliance: APIs must adhere to PSD2, GDPR, and other banking regulations for legality

![]()

API Definition: Application Programming Interface enables secure data exchange between banking systems and third-party services

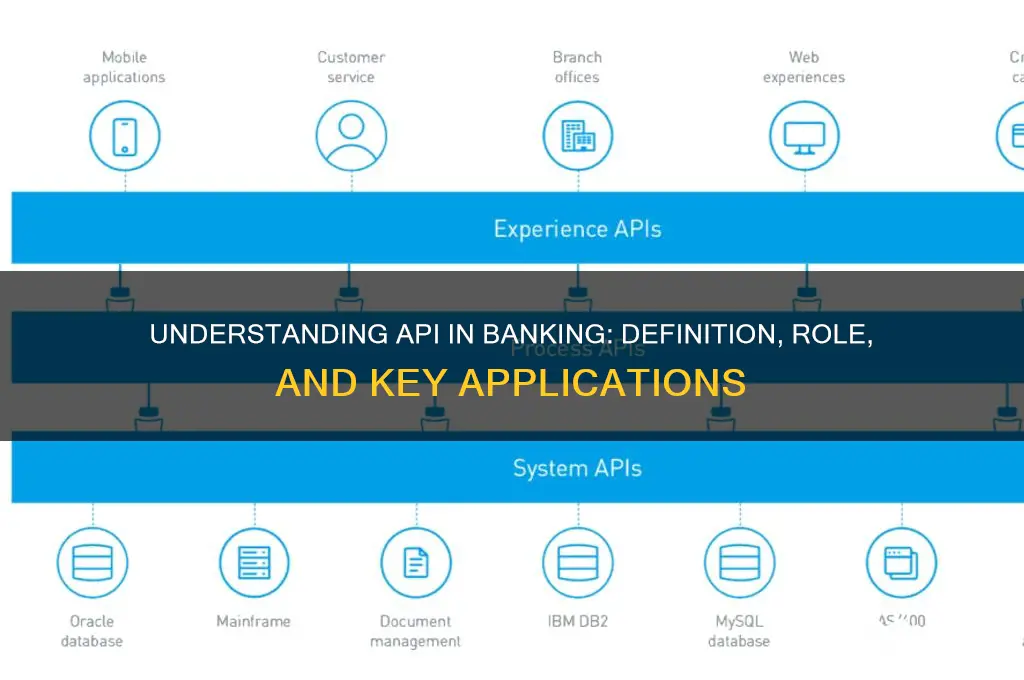

APIs, or Application Programming Interfaces, are the unsung heroes of modern banking, acting as secure bridges between banks and third-party services. Imagine a scenario where a customer wants to link their bank account to a budgeting app. Without APIs, this process would be cumbersome, requiring manual data entry and potentially compromising security. APIs streamline this interaction by allowing the app to request and receive specific financial data directly from the bank’s system, all while ensuring that sensitive information remains protected. This seamless integration not only enhances user experience but also fosters innovation by enabling developers to create new financial tools and services.

From a technical standpoint, APIs function as a set of rules and protocols that dictate how different software systems communicate. In banking, these interfaces are designed with robust security measures, such as encryption and tokenization, to safeguard customer data during transmission. For instance, when a payment gateway processes a transaction, it uses APIs to verify account details and authorize the payment without exposing the full account information to the merchant. This level of security is critical in an era where cyber threats are increasingly sophisticated, ensuring trust between banks, customers, and third-party providers.

The adoption of APIs in banking has also spurred the rise of open banking, a paradigm shift that encourages financial institutions to share customer data (with consent) through standardized APIs. This has led to the creation of innovative services like automated savings apps, loan comparison platforms, and personalized financial advisors. For example, a user can grant a loan aggregator access to their banking data via APIs, allowing the platform to analyze their financial health and recommend tailored loan options. This democratization of financial data empowers consumers to make informed decisions while driving competition and efficiency in the banking sector.

However, the implementation of APIs in banking is not without challenges. Banks must balance innovation with compliance, ensuring that API integrations adhere to regulatory standards like GDPR and PSD2. Additionally, managing API traffic and preventing misuse requires robust monitoring and governance frameworks. For instance, rate limiting can prevent excessive requests that might overload systems, while API keys and OAuth protocols ensure that only authorized parties access sensitive data. Despite these hurdles, the benefits of APIs—enhanced functionality, improved customer experience, and new revenue streams—make them indispensable in the digital banking ecosystem.

In practical terms, banks and fintech companies can maximize the potential of APIs by adopting a strategic approach. This includes investing in API management platforms that provide analytics, security, and scalability. For developers, adhering to API documentation and best practices ensures smooth integration and minimizes errors. Customers, on the other hand, should remain vigilant about granting permissions to third-party apps, understanding the scope of data shared via APIs. As APIs continue to evolve, their role in banking will only grow, shaping the future of financial services by enabling secure, efficient, and innovative data exchange.

Self-Heating Meals: A Food Bank's Friend or Foe?

You may want to see also

Explore related products

![]()

Banking API Types: Open banking, payment, account information, and investment APIs streamline financial operations

APIs, or Application Programming Interfaces, in banking are the digital bridges that connect financial institutions, third-party developers, and customers, enabling seamless data exchange and service integration. Among the myriad API types, open banking, payment, account information, and investment APIs stand out for their transformative impact on financial operations. Each serves a distinct purpose, yet together they form a cohesive ecosystem that enhances efficiency, transparency, and innovation.

Open banking APIs are the cornerstone of modern financial collaboration. By allowing third-party developers to access bank data (with customer consent), they foster competition and innovation. For instance, budgeting apps like Mint leverage these APIs to aggregate user accounts, providing a holistic view of finances. However, their power lies in their regulatory framework—in the EU, the PSD2 directive mandates banks to share data securely. This has spurred the creation of services like loan comparison platforms and automated savings tools, proving that open banking APIs are not just about compliance but about redefining customer experiences.

Payment APIs, on the other hand, are the workhorses of transactional efficiency. They enable businesses to initiate, process, and track payments in real time, reducing friction for both merchants and consumers. Stripe’s API, for example, allows e-commerce platforms to accept payments globally with minimal integration effort. Yet, their true value emerges in emerging markets, where mobile money APIs (like M-Pesa’s) have revolutionized financial inclusion. For developers, the key is to balance simplicity with security—implementing tokenization and 3D Secure protocols ensures that convenience doesn’t compromise safety.

Account information APIs serve as the financial equivalent of a dashboard, providing real-time insights into account balances, transaction histories, and spending patterns. These APIs are particularly valuable for businesses managing cash flow or individuals tracking expenses. For instance, accounting software like QuickBooks uses them to automatically sync bank data, eliminating manual entry errors. However, their effectiveness hinges on data granularity—APIs that categorize transactions (e.g., groceries, utilities) offer more actionable insights than those that merely list dates and amounts.

Finally, investment APIs democratize access to financial markets by enabling apps to offer trading, portfolio management, and robo-advisory services. Platforms like Robinhood and Betterment rely on these APIs to execute trades, analyze risk profiles, and provide personalized recommendations. A critical consideration here is latency—even milliseconds of delay can impact trade outcomes. Developers must prioritize APIs with low-latency connections to exchanges and robust error-handling mechanisms to manage market volatility.

Together, these API types form a toolkit that streamlines financial operations, from everyday transactions to long-term wealth management. Their adoption requires a strategic approach: banks must prioritize security and compliance, while developers should focus on user experience and scalability. As the financial landscape evolves, these APIs will not just adapt but lead the charge, proving that in banking, connectivity is currency.

Does the Deal or No Deal Banker Really Talk? Unveiling the Mystery

You may want to see also

Explore related products

![]()

API Benefits: Enhances customer experience, enables innovation, and improves efficiency in banking services

APIs, or Application Programming Interfaces, in banking are the unsung heroes behind seamless digital experiences. They act as bridges, allowing different software systems to communicate and share data securely. This interoperability is the cornerstone of modern banking, enabling everything from mobile payments to personalized financial advice.

APIs enhance customer experience by putting control directly in the hands of users. Imagine a customer wanting to track expenses across multiple accounts. With APIs, a budgeting app can securely access transaction data from various banks, providing a holistic view without the customer manually inputting information. This level of convenience and personalization fosters loyalty and satisfaction.

The true power of APIs lies in their ability to fuel innovation. Banks can now partner with fintech startups, leveraging their specialized services through API integrations. For instance, a bank could offer its customers access to a robo-advisor platform for investment guidance, or integrate a peer-to-peer lending service, all without developing these solutions in-house. This open ecosystem accelerates the introduction of new products and services, keeping banks competitive in a rapidly evolving landscape.

The efficiency gains from APIs are equally transformative. Manual processes like loan applications, which traditionally involved mountains of paperwork and lengthy approval times, can be streamlined through API-driven automation. Data verification, credit checks, and document processing can be completed in minutes, not days, leading to faster approvals and happier customers. This efficiency translates to cost savings for banks, allowing them to reinvest in further innovation and customer-centric initiatives.

However, reaping the full benefits of APIs requires a strategic approach. Banks must prioritize security and data privacy, implementing robust authentication and authorization mechanisms. Additionally, clear API documentation and developer support are crucial for fostering a thriving ecosystem of third-party developers. By embracing APIs responsibly, banks can unlock a new era of customer-centric, innovative, and efficient banking services.

How to Send Emails via ICICI Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Security Measures: APIs use encryption, OAuth, and tokenization to protect sensitive banking data

APIs, or Application Programming Interfaces, in banking facilitate seamless data exchange between financial systems, enabling services like mobile payments and account aggregation. However, this convenience comes with risks, as sensitive data such as account numbers and transaction details are exposed. To mitigate these risks, robust security measures are essential. Encryption, OAuth, and tokenization are the cornerstone technologies that safeguard banking APIs, ensuring data integrity and confidentiality.

Encryption: The First Line of Defense

Encryption transforms sensitive data into unreadable formats, making it indecipherable to unauthorized users. In banking APIs, TLS (Transport Layer Security) is commonly used to encrypt data in transit, ensuring secure communication between client and server. For data at rest, AES-256 encryption is often employed, providing military-grade protection. For instance, when a user initiates a fund transfer via a banking app, TLS encrypts the request, while AES-256 secures the stored transaction records. Without encryption, intercepted data would be vulnerable to exploitation, making it a non-negotiable security measure.

OAuth: Managing Access with Precision

OAuth is a protocol that allows secure authorization without exposing user credentials. It ensures that third-party applications can access banking APIs only with explicit user consent and within predefined scopes. For example, a budgeting app might request read-only access to transaction history but cannot initiate payments. OAuth 2.0, the latest version, uses access tokens with short expiration times, reducing the risk of unauthorized access. This granular control minimizes the attack surface, as even if a token is compromised, its limited scope restricts potential damage.

Tokenization: Replacing Sensitive Data with Safe Proxies

Tokenization replaces sensitive data, such as card numbers, with unique tokens that have no intrinsic value. These tokens are used for processing transactions without exposing the actual data. For instance, when a customer saves a card for recurring payments, the bank’s API tokenizes the card details, storing only the token in its systems. Even if a breach occurs, the tokens are useless to attackers. This method is particularly effective in preventing fraud in e-commerce transactions, where card details are frequently shared.

Practical Implementation and Best Practices

To maximize API security, banks must adopt a layered approach. First, enforce end-to-end encryption for all data exchanges. Second, implement OAuth 2.0 with PKCE (Proof Key for Code Exchange) for mobile and single-page applications to prevent authorization code interception. Third, integrate tokenization for payment processing and customer data storage. Regularly audit API endpoints for vulnerabilities and ensure compliance with standards like PCI DSS for payment security. Additionally, educate users on recognizing phishing attempts targeting OAuth authorization flows.

The Takeaway: Security as a Competitive Advantage

While APIs drive innovation in banking, their security is paramount. Encryption, OAuth, and tokenization are not just technical requirements but strategic investments in customer trust. By implementing these measures rigorously, banks can protect sensitive data, comply with regulations, and differentiate themselves in a competitive market. In an era where data breaches can erode trust overnight, robust API security is not optional—it’s essential.

Firearm-Friendly Banking: Where Are the Options?

You may want to see also

Explore related products

![]()

Regulatory Compliance: APIs must adhere to PSD2, GDPR, and other banking regulations for legality

APIs in banking are not just tools for innovation; they are gateways to a highly regulated environment. In this context, regulatory compliance is non-negotiable. APIs must adhere to stringent regulations such as PSD2 (Payment Services Directive 2) and GDPR (General Data Protection Regulation) to ensure legality and maintain trust in the financial ecosystem. Failure to comply can result in severe penalties, reputational damage, and loss of customer confidence.

Consider PSD2, a European regulation that mandates banks to provide third-party providers (TPPs) with secure access to customer account data via APIs. This directive aims to foster competition and innovation in the financial sector while ensuring robust security measures. For instance, APIs must implement Strong Customer Authentication (SCA), requiring multi-factor authentication for transactions. Banks and TPPs must also ensure that APIs are designed to handle dynamic linking, where transaction details are securely tied to the authentication process. Non-compliance with PSD2 can lead to fines of up to €5 million or 5% of annual global turnover, whichever is higher.

GDPR, on the other hand, focuses on data protection and privacy. APIs handling customer data must ensure data minimization, collecting only the information necessary for the intended purpose. They must also provide mechanisms for data portability and the right to be forgotten, allowing customers to access, transfer, or delete their data. For example, if a customer requests their data be erased, the API must propagate this request across all connected systems. Failure to comply with GDPR can result in fines of up to €20 million or 4% of annual global turnover, making it imperative for banks to embed compliance into their API design and operations.

Beyond PSD2 and GDPR, APIs must also align with other banking regulations such as MiFID II (Markets in Financial Instruments Directive) for investment services, AML (Anti-Money Laundering) directives, and KYC (Know Your Customer) requirements. Each regulation imposes specific obligations on API functionality, data handling, and security. For instance, AML compliance may require APIs to flag suspicious transactions in real-time, while KYC regulations mandate identity verification processes. Banks must adopt a layered compliance approach, integrating regulatory requirements into every stage of API development, from design to deployment.

To navigate this complex regulatory landscape, banks should adopt API governance frameworks that include regular audits, risk assessments, and compliance monitoring. Tools like API gateways can enforce security policies, while data encryption and tokenization ensure data protection. Additionally, collaboration with regulatory bodies and participation in industry standards initiatives, such as the Berlin Group for PSD2, can provide clarity and best practices. By prioritizing regulatory compliance, banks can leverage APIs to drive innovation while safeguarding legality and customer trust.

Does Cash App Share Bank Records with Police? Privacy Explained

You may want to see also

Frequently asked questions

API stands for Application Programming Interface in banking, a set of rules and protocols that allows different software applications to communicate and share data securely.

APIs in banking enable services like account aggregation, payment processing, fraud detection, and third-party app integrations, streamlining operations and enhancing customer experiences.

APIs improve efficiency, enable innovation, enhance customer experiences, facilitate seamless integrations, and support the development of new financial products and services.

Yes, banking APIs are designed with robust security measures, including encryption, authentication, and compliance with standards like OAuth and PSD2, to protect sensitive financial data.

An example is a payment gateway API, which allows merchants to process transactions securely by connecting their systems to banks or payment processors.