ARP, in the context of banking, stands for Automated Reconciliation Process, a critical tool used to streamline and automate the matching of financial transactions across different systems. This process ensures accuracy, reduces manual errors, and enhances efficiency by reconciling accounts, payments, and other financial activities in real-time or at regular intervals. ARP is widely adopted in banking to maintain compliance, detect discrepancies, and improve overall financial integrity.

Explore related products

What You'll Learn

- Address Resolution Protocol Basics: ARP resolves IP addresses to physical MAC addresses in banking networks

- ARP in Secure Transactions: Ensures secure data transmission by verifying device identities in banking systems

- ARP Spoofing Risks: Protects banks from ARP spoofing attacks that redirect traffic maliciously

- ARP in Network Monitoring: Helps banks monitor network devices and detect unauthorized access attempts

- ARP Role in Compliance: Supports regulatory compliance by maintaining accurate device identification in banking networks

![]()

Address Resolution Protocol Basics: ARP resolves IP addresses to physical MAC addresses in banking networks

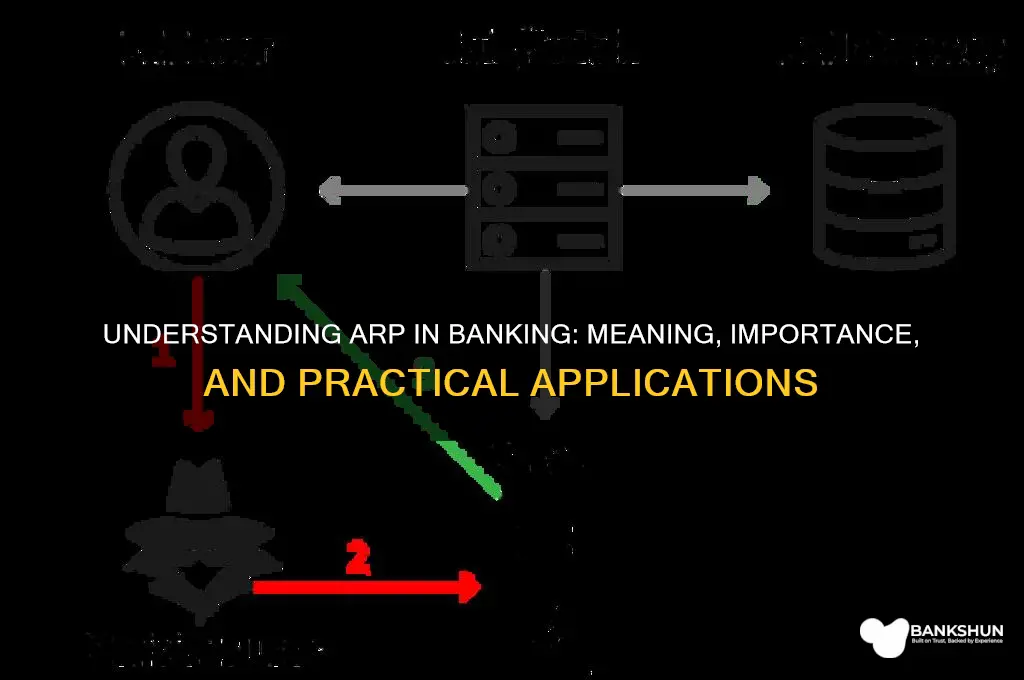

In banking networks, where secure and efficient communication is paramount, the Address Resolution Protocol (ARP) plays a critical role. ARP is the bridge between the logical world of IP addresses and the physical realm of MAC addresses, ensuring that data packets reach their intended destinations within the network. Without ARP, devices would struggle to communicate, leading to inefficiencies and potential security vulnerabilities.

Consider a scenario where a bank’s ATM requests transaction data from a central server. The ATM knows the server’s IP address but lacks its physical MAC address, which is essential for data transmission over the local network. Here, ARP steps in by broadcasting a request: “Who has this IP address? Tell me your MAC address.” The server responds with its MAC address, allowing the ATM to establish a direct connection. This process, though seamless to the end-user, is fundamental to maintaining the integrity and speed of banking operations.

While ARP is indispensable, it’s not without risks. Malicious actors can exploit ARP to launch attacks, such as ARP spoofing, where an attacker links their MAC address to a legitimate IP address, intercepting sensitive data. Banking networks must implement safeguards like ARP inspection and static ARP entries to mitigate these threats. For instance, a bank might configure its network devices to validate ARP requests against a trusted table of IP-to-MAC mappings, ensuring only authorized devices communicate.

Understanding ARP’s mechanics is crucial for IT professionals in banking. For example, during network troubleshooting, analyzing ARP tables can reveal IP-MAC conflicts or unauthorized devices. Tools like Wireshark can capture ARP traffic, providing insights into network behavior. Additionally, segmenting the network into VLANs reduces ARP broadcast traffic, enhancing performance and security. By mastering ARP basics, banking IT teams can optimize network efficiency and fortify defenses against cyber threats.

In summary, ARP is the unsung hero of banking networks, translating IP addresses into MAC addresses to enable seamless communication. Its role is both critical and vulnerable, demanding proactive security measures. By leveraging ARP’s capabilities and addressing its risks, banks can ensure their networks remain robust, secure, and ready to support the demands of modern financial transactions.

Citizens Bank: Can You Cash US Savings Bonds Here?

You may want to see also

Explore related products

![]()

ARP in Secure Transactions: Ensures secure data transmission by verifying device identities in banking systems

ARP, or Address Resolution Protocol, plays a pivotal role in banking systems by ensuring secure data transmission through device identity verification. In a typical banking transaction, data travels across networks, making it vulnerable to interception or manipulation. ARP acts as a gatekeeper, mapping IP addresses to physical device identifiers (MAC addresses) to confirm that data is sent to the correct, authenticated device. Without this verification, malicious actors could impersonate legitimate devices, compromising sensitive financial information.

Consider a scenario where a customer initiates an online payment. The bank’s system uses ARP to cross-reference the IP address of the customer’s device with its unique MAC address. If the addresses don’t match or if the device is unrecognized, the transaction is flagged or blocked. This process prevents man-in-the-middle attacks, where hackers intercept data by posing as a trusted device. By validating device identities at the network level, ARP provides a foundational layer of security that complements encryption and other advanced protocols.

However, ARP is not without limitations. It operates at the data link layer and can be susceptible to spoofing attacks if not properly secured. For instance, an attacker could flood the network with fake ARP responses, redirecting traffic to their device. To mitigate this, banks often implement ARP spoofing detection tools and use secure versions of the protocol, such as Dynamic ARP Inspection (DAI). DAI verifies ARP packets against a trusted database, ensuring only legitimate devices participate in network communication.

In practice, ARP’s role in secure transactions extends beyond individual devices to entire banking infrastructures. Automated Teller Machines (ATMs), point-of-sale (POS) terminals, and internal servers all rely on ARP to maintain secure communication channels. For example, when an ATM processes a withdrawal, ARP ensures the request is routed to the bank’s authenticated server, not a fraudulent device. This seamless verification happens in milliseconds, safeguarding transactions without disrupting user experience.

To maximize ARP’s effectiveness, banks should adopt a multi-layered security approach. Pairing ARP with IP address management (IPAM) systems, network segmentation, and regular security audits can create a robust defense against cyber threats. Additionally, educating employees and customers about the importance of secure device connections can further reduce risks. While ARP is a technical protocol, its impact on secure banking transactions is profoundly practical, ensuring trust in every digital interaction.

Step-by-Step Guide to Filling Karur Vysya Bank Cheques Correctly

You may want to see also

Explore related products

![]()

ARP Spoofing Risks: Protects banks from ARP spoofing attacks that redirect traffic maliciously

ARP, in banking, stands for Address Resolution Protocol, a critical component of network communication that maps IP addresses to physical MAC addresses. While essential for data transmission, ARP is vulnerable to exploitation, particularly through ARP spoofing. This attack involves a malicious actor sending falsified ARP messages over a local network, linking their MAC address with the IP address of a legitimate device—often a bank’s server or router. The result? Network traffic intended for the legitimate device is redirected to the attacker, enabling interception, modification, or theft of sensitive data. For banks, this poses a grave risk, as financial transactions, customer credentials, and proprietary information could be compromised.

To illustrate, consider a scenario where an attacker targets a bank’s internal network. By spoofing the ARP table of a bank employee’s computer, the attacker could redirect traffic meant for the bank’s secure server to their own machine. This allows them to eavesdrop on communications, inject malicious data, or even launch man-in-the-middle attacks. For instance, a customer initiating an online transfer could unknowingly send their login credentials and transaction details directly to the attacker, who could then drain the account or alter the transaction. Such breaches not only result in financial losses but also erode customer trust, a cornerstone of banking operations.

Protecting against ARP spoofing requires a multi-layered approach. Network segmentation is a foundational step, isolating critical systems like payment gateways or customer databases from less secure parts of the network. Implementing ARP spoofing detection tools, such as software that monitors ARP traffic for anomalies, can alert administrators to potential attacks in real time. Static ARP entries can also be configured for critical devices, ensuring their MAC-to-IP mappings cannot be altered. Additionally, encryption protocols like TLS/SSL should be enforced for all communications, rendering intercepted data unreadable to attackers.

Banks must also prioritize employee training and awareness. Phishing attacks often serve as the entry point for ARP spoofing, as attackers gain initial access to the network through compromised credentials. Regular security audits and penetration testing can identify vulnerabilities before they’re exploited. For instance, a bank could simulate an ARP spoofing attack to assess its network’s resilience and refine its defenses. By combining technical safeguards with proactive measures, banks can significantly reduce the risk of ARP spoofing and safeguard their operations.

In conclusion, while ARP is a fundamental protocol in banking networks, its vulnerabilities demand vigilant protection. ARP spoofing attacks pose a direct threat to financial integrity and customer trust, but with the right strategies—from network segmentation to employee training—banks can fortify their defenses. As cyber threats evolve, staying ahead requires not just reactive measures but a proactive, holistic approach to network security.

The Birth of the World Bank: A Historical Overview

You may want to see also

![]()

ARP in Network Monitoring: Helps banks monitor network devices and detect unauthorized access attempts

ARP, or Address Resolution Protocol, is a critical component in network monitoring, especially within the banking sector. It operates at the data link layer, translating IP addresses into physical MAC addresses, enabling devices to communicate effectively. For banks, this protocol is not just a technical necessity but a cornerstone of network security. By leveraging ARP, financial institutions can meticulously monitor network devices, ensuring that every packet of data travels between authorized endpoints. This granular oversight is essential in an environment where unauthorized access attempts can lead to significant financial and reputational damage.

In the context of network monitoring, ARP plays a dual role: it facilitates communication and acts as a sentinel. Banks deploy ARP monitoring tools to track all ARP requests and replies across their networks. These tools log every instance where a device attempts to map an IP address to a MAC address, creating a detailed record of network activity. For instance, if an unauthorized device tries to join the network, it must send an ARP request to communicate with other devices. This request is immediately flagged by the monitoring system, allowing security teams to investigate and mitigate the threat before any harm occurs.

One practical example of ARP in action is its use in detecting ARP spoofing attacks, a common tactic employed by cybercriminals. In such attacks, malicious actors send falsified ARP messages over a local area network, linking their MAC address with the IP address of a legitimate device. This allows them to intercept, modify, or stop data intended for the victim device. By continuously monitoring ARP traffic, banks can identify anomalies, such as multiple MAC addresses associated with a single IP address, and take immediate corrective action. This proactive approach not only prevents data breaches but also ensures compliance with stringent regulatory requirements.

Implementing ARP monitoring requires a strategic blend of technology and policy. Banks should invest in advanced network monitoring solutions that offer real-time ARP traffic analysis, coupled with automated alerts for suspicious activity. Additionally, regular audits of ARP tables can help identify discrepancies early. Training IT staff to recognize the signs of ARP-related threats and establishing clear protocols for response are equally important. For instance, if an unauthorized device is detected, the network should be configured to automatically isolate the device and notify administrators.

In conclusion, ARP in network monitoring is a powerful tool for banks to safeguard their digital infrastructure. Its ability to provide visibility into network communications and detect unauthorized access attempts makes it indispensable in the fight against cyber threats. By integrating ARP monitoring into their cybersecurity strategy, banks can not only protect sensitive financial data but also maintain the trust of their customers in an increasingly interconnected world.

Efficiently Mass Move Pokémon in Poké Bank: A Step-by-Step Guide

You may want to see also

![]()

ARP Role in Compliance: Supports regulatory compliance by maintaining accurate device identification in banking networks

In banking networks, ARP (Address Resolution Protocol) plays a pivotal role in ensuring regulatory compliance by maintaining accurate device identification. This protocol translates IP addresses into physical MAC addresses, enabling devices to communicate effectively within a network. For banks, this process is critical because it ensures that every device connected to the network is correctly identified, which is a foundational requirement for compliance with regulations like GDPR, PCI DSS, and others. Without accurate device identification, banks risk unauthorized access, data breaches, and regulatory penalties.

Consider the operational complexity of a modern banking network, which includes ATMs, employee workstations, servers, and IoT devices. ARP ensures that each of these devices is uniquely identified, preventing IP conflicts and unauthorized devices from infiltrating the network. For instance, if an unauthorized device attempts to connect, ARP can flag the discrepancy between its IP and MAC addresses, triggering security protocols. This real-time verification is essential for meeting regulatory standards that mandate continuous monitoring and control over network access.

However, ARP’s role in compliance isn’t without challenges. One significant issue is ARP spoofing, where attackers manipulate ARP tables to redirect traffic, potentially intercepting sensitive data. To mitigate this, banks must implement ARP inspection tools and regularly audit ARP tables. For example, deploying network monitoring solutions like Cisco’s Dynamic ARP Inspection (DAI) can automatically detect and block malicious ARP entries. Additionally, segmenting networks and using VLANs can limit the scope of potential ARP attacks, further strengthening compliance efforts.

A practical takeaway for banking IT teams is to integrate ARP monitoring into their broader compliance strategy. Start by conducting regular ARP table audits to identify anomalies. Pair this with employee training on recognizing ARP spoofing attempts, such as unexpected network slowdowns or unauthorized access alerts. Finally, invest in automated tools that provide real-time ARP monitoring and alerts, ensuring immediate response to potential threats. By treating ARP as a cornerstone of network security, banks can not only maintain compliance but also enhance overall cybersecurity posture.

Easy Steps to Access Your Synchrony Bank Account: A Login Guide

You may want to see also

Frequently asked questions

ARP stands for Automated Reconciliation Process in banking, which refers to the automated matching and verification of financial transactions to ensure accuracy and consistency in records.

ARP streamlines banking operations by reducing manual effort, minimizing errors, and ensuring timely reconciliation of accounts, thereby improving efficiency and compliance with regulatory standards.

No, ARP (Automated Reconciliation Process) is different from APR (Annual Percentage Rate), which is the cost of borrowing expressed as a yearly interest rate. ARP focuses on transaction reconciliation, while APR relates to loan or credit costs.