In the world of banking, Nacha stands for the National Automated Clearing House Association. It is an independent, non-profit organisation that operates the Automated Clearing House (ACH) network, which is a centralised US financial network that enables electronic payments and money transfers between accounts at different banks. The ACH network is the technology that moves payments from one bank account to another, and Nacha is the organisation that owns, manages, and sets the rules and regulations for this network.

| Characteristics | Values |

|---|---|

| Full Form | National Automated Clearing House Association |

| Type of Organization | Non-profit association funded by U.S. financial institutions |

| Ownership | Owned by a large group of banks, credit unions, and payment processing companies |

| Function | Operates the Automated Clearing House (ACH) network, a centralized US financial network |

| ACH Network | Connects all U.S. financial institutions through a ubiquitous payment system |

| ACH Payment Types | Direct Deposits, Direct Payments, Social Security, Government benefits statements, Electronic bill payments, Person-to-person (P2P), Business-to-business (B2B) payments |

| ACH Payment Methods | Same Day ACH, Standard ACH |

| ACH Payment Time | A few hours to a few days |

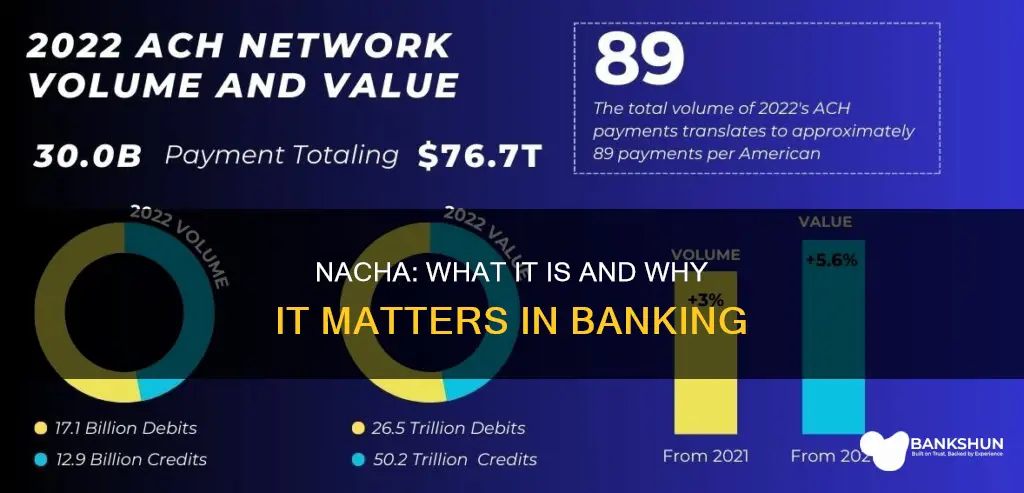

| ACH Payment Value | 33.6 billion ACH Network payments made in 2024, valued at $86.2 trillion |

| ACH Payment Security | Rules and regulations to be followed by businesses to avoid warnings, fines, and suspension |

| ACH Payment Tools | QuickBooks, Payment Automation software, AP Automation software |

| Other Functions | Provides education, accreditation, and advisory services |

| ACH Operators | Federal Reserve, Electronic Payments Network |

Explore related products

What You'll Learn

![]()

The ACH Network

Nacha develops and administers the private sector Nacha Operating Rules for ACH payments, which define the roles and responsibilities of ACH Network participants. Nacha's operating rules can change, so it is important for businesses to check the Nacha website periodically to ensure compliance.

Which NASCAR Track Boasts the Steepest Banking?

You may want to see also

![]()

Nacha's role in ACH payments

Nacha, or the National Automated Clearing House Association, is an independent organisation that operates the Automated Clearing House (ACH) network. The ACH network is a centralised US financial network that enables banks and credit unions to send and receive electronic payments and money transfers.

Nacha is responsible for the rules and standards that govern the movement of money between accounts held at various types of financial or payments companies. It develops and enforces the Nacha Operating Rules for ACH payments, which define the roles and responsibilities of ACH Network participants. These rules are extensive and are subject to change, so businesses that use the ACH network are advised to check the Nacha website periodically to ensure they remain compliant.

The ACH network is the backbone of the US financial system, connecting all US financial institutions through a single, ubiquitous payment system. It is used for a variety of transactions, including consumer purchases, bill payments, employee paychecks, tax payments, direct deposits, and business-to-business (B2B) payments. ACH payments can be processed in a matter of hours on the same business day or can be scheduled for the following day, or even up to two days later.

Nacha also provides services in education, accreditation, industry engagement with financial institutions, businesses, and government, and advocacy resources. It works closely with government agencies, including the Federal Reserve, the US Treasury, and state banking authorities, to ensure the integrity of the electronic payments systems used by US financial institutions.

Instant Bank Verification: Venmo's Quick Guide

You may want to see also

![]()

Nacha's rules and regulations

Nacha, or the National Automated Clearing House Association, is an independent organisation that operates the Automated Clearing House (ACH) network. The ACH network is a centralised US financial network that enables electronic fund transfers between accounts at different banks.

As the operator of the ACH network, Nacha is responsible for establishing and enforcing the rules and guidelines that govern the network and ACH payments. The organisation develops and administers the Nacha Operating Rules for ACH payments, which define the roles and responsibilities of ACH Network participants.

To ensure compliance with its rules, Nacha has a formal system of warnings and fines for violations. The organisation's Compliance department assists financial institutions in recouping funds lost due to rules violations through arbitration.

Nacha's rules are subject to change, and the organisation encourages businesses using the ACH network to periodically check for updates to ensure ongoing compliance.

Understanding Tax Deductions for Bank Fees as an Individual

You may want to see also

![]()

Nacha's history

Nacha, previously known as the National Automated Clearing House Association, is a non-profit association that facilitates electronic financial transactions between US bank accounts. It was created in 1974 with the merger of several regional bodies.

The history of Nacha began in 1972 with the formation of the first ACH association in California to handle electronic payments. This was the California Automated Clearing House Association (now called WesPay), which became the first operational ACH association in the United States. Over the next two years, other regional ACH associations were formed, and in 1974, they merged to create Nacha.

As the administrator of the ACH Network, Nacha develops and enforces the rules and standards for ACH transactions. It also provides education, accreditation, and advisory services. The ACH Network is a centralized US financial network that connects all US financial institutions through a ubiquitous payment system. It enables the electronic movement of money and data between bank accounts, without the use of paper checks, wire transfers, credit cards, or cash.

Nacha has been instrumental in developing and standardizing innovations such as direct payroll deposit, electronic benefits deposit, and automated credit card transactions. It also works closely with government agencies, including the Federal Reserve, to ensure the integrity of the electronic payment systems used by US financial institutions.

In 2014, Nacha formed the Payments Innovation Alliance to represent the payments industry and the ACH Network. The Alliance offers discussion, debate, education, and networking on topics such as payment system modernization, trends, standards, security, and ongoing innovation.

In 2016, Nacha introduced Same Day ACH, which allows for quicker payments of insurance claims and faster expense payments. This was followed by Phase 2 in 2017, which enabled the same-day processing of virtually any ACH payment.

International Bank of Commerce: Zelle Availability and Accessibility

You may want to see also

![]()

Nacha's file format

Nacha stands for the National Automated Clearing House Association. It is an independent organisation that operates the Automated Clearing House (ACH) network, which is a centralised US financial network. The ACH network enables electronic financial transactions between banks and payment services providers.

The ACH file format is designed to allow various levels of ACH processing. An ACH file is a fixed-width, ASCII file, with each line exactly 94 characters in length. Each line of characters is known as a "record" and is comprised of various "fields" that are at specific positions within that line. In a properly formatted file, records must follow a specific order.

ACH files contain one or more batches, which consist of one or more transactions. Each batch starts with a single "Batch Header Record", which begins with "5" and describes the type (debits and/or credits) and purpose of all transaction entries within the batch. This record identifies the company as the originator and provides a description for all the transactions in the batch.

Each file always ends with the "File Control Record", or the "9" record. This record contains various counts (number of batches, number of entries, etc.), sums (debit total and credit total), and another hash total to ensure that the file was generated correctly. ACH files have a blocking factor of 10 and are padded with lines of 9s so that the number of lines in the file is a multiple of 10.

Certain data elements are captured at different levels within the ACH format (file, batch, or transaction). As such, certain transactions will be batched together where the Standard Entry Class (SEC) Code, effective entry date, company ID, and Batch descriptor are identical, based on similar information required at the element level.

Finding Your Bank's Nearest Branch

You may want to see also

Frequently asked questions

Nacha stands for the National Automated Clearing House Association. It is an independent organization that operates the Automated Clearing House (ACH) network, which is a centralized US financial network.

The ACH network is a payment system that drives safe, smart, and fast Direct Deposits and Direct Payments with the capability to reach all US bank and credit union accounts. It is a way to directly transfer money between accounts at different banks without the use of paper checks, wire transfers, credit cards, or cash.

ACH payments can be used for a variety of transactions, including employee paychecks, tax payments, government benefits statements, electronic bill payments, person-to-person (P2P), and business-to-business (B2B) payments.