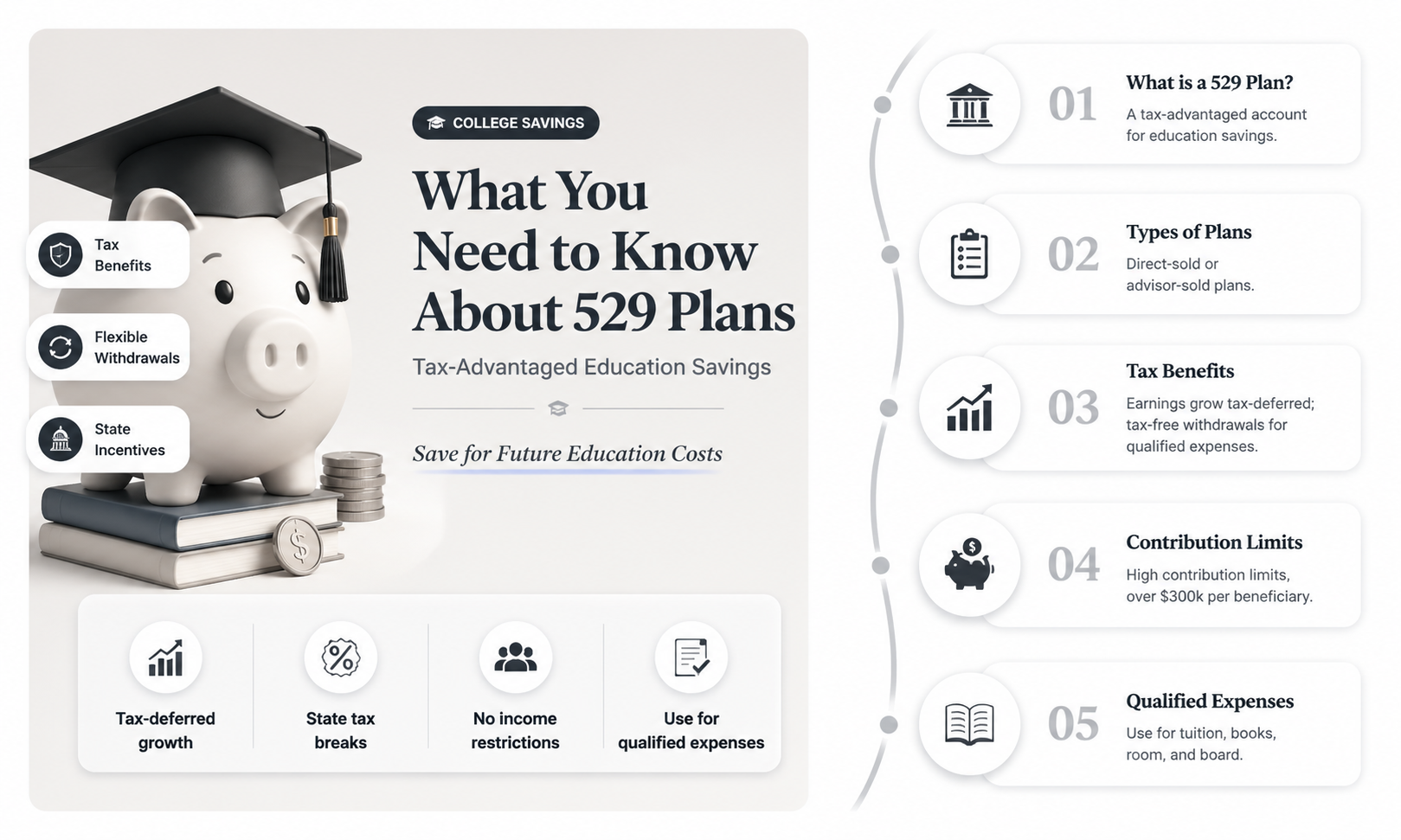

A 529 plan is a tax-advantaged investment account designed to help pay for education-related expenses. It is named after Section 529 of the Internal Revenue Code (IRC). While all 529 plans offer tax advantages, they are not all the same. Each state's 529 plan may have different minimum contribution amounts, and there are a variety of investment options available. For example, Ohio's plan offers savers a mix of investment plans based on age and risk tolerance, while New York's plan offers low-cost investment options.

| Characteristics | Values |

|---|---|

| Purpose | Saving for children's education |

| Type of account | Tax-advantaged investment account |

| Eligibility | Anyone can open a 529 plan; no state residency requirements |

| Contributions | Flexible; no minimum contribution amounts; anyone can contribute |

| Beneficiaries | One beneficiary at a time; can be changed multiple times to qualified individuals |

| Investment options | Age-based, static, and individual options; low-cost options available |

| Tax implications | Tax-free withdrawals for qualified education expenses; earnings not subject to federal tax |

| Rollovers | Allowed to another plan for the same beneficiary or a family member without penalty |

| Use of funds | Qualified expenses include tuition, fees, books, room and board, textbooks, computers, and related equipment |

| Prepaid plans | Offered by some states and higher education institutions; lock in tuition at current rates |

| Investment return | Not guaranteed; may need to consider alternative options or consult a financial planner |

Explore related products

What You'll Learn

![]()

529 plans are tax-advantaged

There are two main types of 529 plans: educational savings plans and prepaid tuition plans. Prepaid tuition plans allow account owners to lock in current tuition rates for future attendance at selected colleges and universities, which can save money as tuition costs tend to increase over time. The specific tax advantages of 529 plans can vary by state, and some states offer additional benefits such as state tax deductions or exemptions on contributions or withdrawals. For example, Kansas taxpayers may be able to deduct up to $3,000 (or $6,000 for married couples filing jointly) from their taxable income for contributions per child.

It is important to note that contributions to 529 plans are typically made with after-tax dollars and are not federally tax-deductible. However, some states may offer state income tax deductions or exemptions on contributions or withdrawals. Additionally, there may be gift tax considerations when contributing large sums to a 529 plan, but accelerated gifting allows individuals to contribute up to five years' worth of annual gift tax exclusions in a single year without triggering gift tax consequences.

Overall, the tax advantages of 529 plans can provide significant benefits for those saving for education expenses, but it is important to carefully consider the specific rules and fees associated with each plan, as they can vary from state to state.

Bank Teller: Who Are They and What Do They Do?

You may want to see also

Explore related products

![]()

Prepaid tuition plans

A 529 plan is a tax-advantaged investment account designed specifically for education expenses. It is named after Section 529 of the Internal Revenue Code (IRC) and is sponsored by a state or financial institution. While all 529 plans offer tax advantages, they are not all the same. There are two types of 529 plans: prepaid tuition plans and savings plans.

However, prepaid tuition plans may limit the colleges they can be used for, and certain plans only allow beneficiaries to attend in-state institutions. Additionally, most state prepaid tuition plans require either the purchaser or the beneficiary to be a resident of the state offering the plan when applying.

Coin Machines: Citizens Bank's Offerings

You may want to see also

Explore related products

![]()

Eligibility and plan options

Eligibility for a 529 plan depends on the type of plan and the state offering it. Every state offers a 529 plan, and while there are no state residency requirements, some states offer tax deductions or other benefits exclusive to residents. For example, Illinois and New York offer tax deductions, while Ohio's plan offers up to $4,000 in state tax deductions per beneficiary for Ohio residents.

There are two main types of 529 plans: 529 college savings plans and 529 prepaid plans. The former is the most common type and is considered the most flexible option. The latter lets you prepay part or all of an in-state public tuition, locking in the tuition rate at the time of payment. A few states and some higher education institutions offer prepaid tuition plans, which may limit the colleges they can be used for.

There are no minimum contribution requirements for opening a 529 plan, but some plans may require minimum contribution amounts depending on the funding method. Each state imposes its own cumulative contribution limit. You can contribute to a 529 plan through a one-time electronic funds transfer, mailing a check, scheduling recurring payments from your bank account, or through payroll deductions.

A 529 plan can have only one beneficiary at a time, but you can change the beneficiary multiple times to a number of qualified individuals. This means that you can use the same plan for different children, but it requires planning to avoid violating the plan's rules and restrictions.

There are age-based, static, and individual options for 529 plans. Age-based options automatically adjust the asset allocation as the beneficiary approaches college age, while static options are based on risk tolerance and US stocks and bonds. Individual options are offered by firms like T. Rowe Price and Vanguard.

Joseph A. Bank Suit Sale: Dates and Deals Revealed

You may want to see also

![]()

Investment options

There are several types of 529 plans, including college savings plans and prepaid tuition plans. College savings plans are the most common type and are generally considered the most flexible option. Investments in these plans grow tax-free and can be withdrawn tax-free for educational expenses. Prepaid tuition plans, on the other hand, allow residents to lock in tuition rates at current prices for future attendance. While these plans grow in value over time, they do not cover room and board costs, and there may be limitations on which colleges they can be used for.

When choosing a 529 plan, it is important to consider the investment options available. Some plans offer age-based investing options that automatically adjust the asset allocation as the beneficiary approaches college age, while others offer static options based on risk tolerance and U.S. stocks and bonds. There are also customizable options that allow investors to choose from various mutual funds, interest income funds, and FDIC-insured accounts.

It is worth noting that participation in a 529 plan does not guarantee a return on investment that will cover future tuition and other expenses. Additionally, while distributions from a 529 plan are generally not taxable, withdrawals for non-qualified expenses may be subject to income tax and a penalty. Therefore, it is important to carefully consider the investment options and potential risks before selecting a 529 plan.

Banking Experts: Who to See and When

You may want to see also

![]()

Pros and cons

529 plans are tax-advantaged investment accounts designed to help pay for education expenses. They are named after Section 529 of the Internal Revenue Code (IRC). While they were originally designed to cover postsecondary education costs, their scope has expanded to cover K–12 education, apprenticeship programs, and student loan repayment.

Pros

529 plans have a range of tax benefits. They offer tax-deferred growth, and withdrawals are generally tax-free when used for qualified education expenses. These include college tuition and fees, books and supplies, room and board costs, and up to $10,000 in K-12 tuition per year. Additionally, 529 plans have no annual contribution limits and offer high aggregate limits. They also offer flexibility in terms of ownership and contributions, and anyone can contribute to the plan. Prepaid tuition plans, a type of 529 plan, allow account owners to lock in current tuition rates for future attendance, which can result in locking in lower prices for college later on.

Cons

The rules and fees of 529 plans differ from state to state, and there may be limitations on the educational institutions that accept them. Prepaid tuition plans, for example, may restrict the colleges they can be used for and do not cover room and board. Additionally, participation in a 529 plan does not guarantee that the investment return will be adequate to cover future tuition and other expenses. While 529 plans offer tax advantages, contributions to them are not deductible. Finally, while 529 plans have no annual contribution limits, the maximum aggregate limit varies by state, ranging from $235,000 to over $500,000.

Disconnecting Your Bank from Plaid: A Step-by-Step Guide

You may want to see also

Frequently asked questions

A 529 plan is a tax-advantaged investment account designed to help pay for education-related expenses.

The main benefit of a 529 plan is the tax advantage. Investments grow tax-free and can be withdrawn tax-free for educational expenses. There is also flexibility in terms of ownership and contributions.

You can choose any plan you like, so it's worth comparing your options. You may want to consider consulting a trusted tax professional or financial planner.

529 plans are not for everyone. There is no guarantee that investment returns will be adequate to cover future tuition and other expenses. There may also be underlying and administrative fees associated with the account.