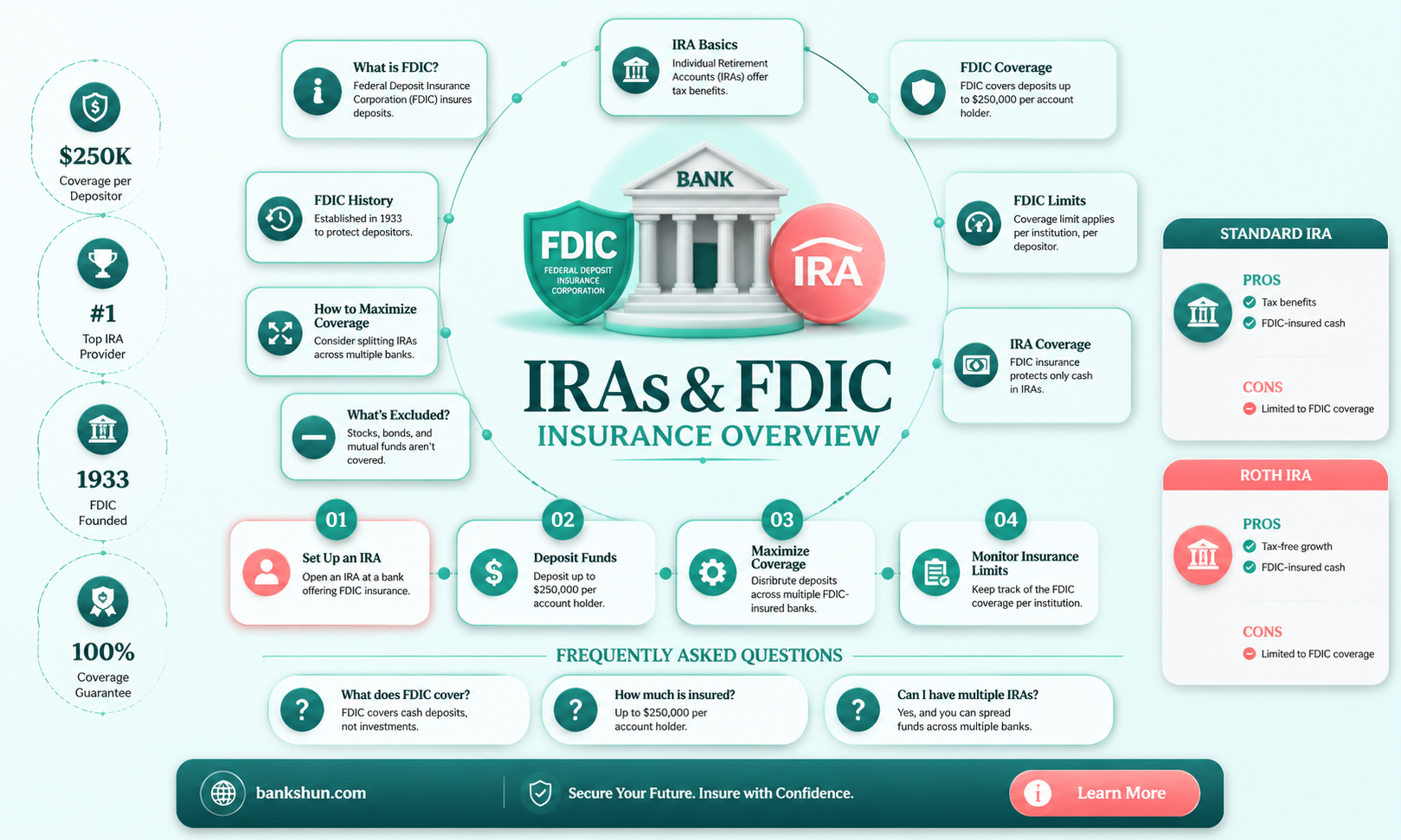

The Federal Deposit Insurance Corporation (FDIC) protects your money in deposit accounts at FDIC-insured banks in the event of a bank failure. FDIC insurance covers retirement accounts, including IRAs, but there are limits. Your IRA may be FDIC-insured if your bank is, and if you have a deposit account instead of investments like stocks or mutual funds. FDIC insurance is limited to $250,000 per person, per bank, and per account ownership category.

| Characteristics | Values |

|---|---|

| FDIC insurance limit | $250,000 per depositor, per bank, per ownership category |

| FDIC insurance coverage | Covers customer deposits at FDIC-insured banks, including those held in checking accounts, savings accounts, money market deposit accounts, and certificates of deposit (CDs) |

| IRA coverage | Traditional and Roth IRAs may be covered up to $250,000 if the bank is FDIC-insured and the account is a deposit account |

| Non-covered accounts | IRAs invested in stocks, mutual funds, bonds, annuities, or other investment products are not covered by FDIC insurance |

| Separate insurance | IRA deposits are insured separately from other deposits at the same institution and at different institutions |

| Reimbursement | FDIC reimburses lost deposits plus interest in the event of bank failure |

| Cost | FDIC insurance is free for consumers and taxpayers; banks pay for it |

| Verification | Search the FDIC website to confirm if your financial institution is FDIC-insured |

Explore related products

What You'll Learn

![]()

FDIC insurance covers retirement accounts, including IRAs

The Federal Deposit Insurance Corporation (FDIC) covers retirement accounts, including IRAs, up to $250,000 per depositor, per bank, and per ownership category. This limit applies to the total balance of all IRA deposits held by one individual at a particular bank. FDIC insurance covers customer deposits held at FDIC-insured banks or savings and loan associations, including those held in checking accounts, savings accounts, money market deposit accounts, and certificates of deposit (CDs).

The FDIC was created in 1933 to maintain stability and public confidence in the U.S. banking system following a period of rising bank failures. The FDIC's original mission was to offer peace of mind to banking customers after the 1929 stock market crash and subsequent financial disasters, including bank runs and failures. Since the FDIC introduced insurance coverage in 1934, insured depositors have not lost any deposits due to bank failure.

It's important to note that FDIC insurance does not cover all types of IRAs. Traditional IRAs and Roth IRAs are treated differently by the FDIC, depending on their type and the financial institution where they are held. For example, IRA investments held in mutual funds, exchange-traded funds (ETFs), or individual stocks are generally not covered by FDIC insurance. Additionally, if the total value of your IRA and other deposit accounts at one institution exceeds $250,000, the excess portion would not be covered by the FDIC.

To confirm if your IRA is covered by FDIC insurance, you can check with your bank or call the FDIC support line. It is important to understand the specifics of your retirement accounts and how they are protected to ensure your funds are fully covered.

Banks: Economy's Lifeline and Growth Engine

You may want to see also

Explore related products

![]()

FDIC insurance doesn't cover investments

The Federal Deposit Insurance Corporation (FDIC) is an independent federal agency that provides protection against losses if an FDIC-insured bank or savings and loan association fails. FDIC insurance covers customer deposits held at FDIC-insured banks or savings and loan associations, including assets held in IRA accounts. This includes checking and savings accounts, money market deposit accounts, and certificates of deposit.

However, it's important to note that FDIC insurance does not cover investments, securities, or any other IRA portfolios held outside of FDIC-insured banks. This includes any sections of your IRA that hold assets like stocks, bonds, funds, or U.S. treasury bills and notes. If you hold your IRA at a credit union or an investment company or brokerage, it is also not covered by FDIC insurance. These types of accounts may be insured by other entities, such as the National Credit Union Administration (NCUA) or the Securities Investors Protection Corporation (SIPC).

FDIC insurance is limited to $250,000 per depositor, per bank, per ownership category. This means that if you have more than $250,000 in total across your IRA and other deposit accounts at a single FDIC-insured bank, the excess portion would not be covered by the FDIC. To determine if your accounts are fully covered, you should know how much money you have in different accounts within one institution. You can also use the FDIC's online Electronic Deposit Insurance Estimator (EDIE) to calculate how much of your funds are covered.

While FDIC insurance does not cover investments, it is important to note that it does cover retirement accounts, including IRAs, as long as they are held at an FDIC-insured bank and meet certain criteria. Self-directed accounts, where the owner directs how the funds are invested, are eligible for FDIC insurance as long as they are held with a depository institution such as a savings bank.

In summary, FDIC insurance does not cover investments or other financial instruments. It is designed to protect customer deposits at FDIC-insured banks, up to a limit of $250,000 per depositor. Retirement accounts, including certain types of IRAs, may be covered by FDIC insurance in the event of a bank failure, but it is important to understand the specific requirements and limitations.

M&T Banks in Florida: Where Are They Located?

You may want to see also

Explore related products

![]()

FDIC insurance covers up to $250,000 per depositor, per bank

FDIC insurance covers up to $250,000 per depositor, per FDIC-insured bank, for each account ownership category. This means that if you have a single ownership account at an FDIC-insured bank, and another single ownership account in a different FDIC-insured bank, you will be insured for up to $250,000 for each account. FDIC insurance covers customer deposits held at FDIC-insured banks or savings and loan associations, including assets held in IRA accounts. This includes checking and savings accounts, money market deposit accounts, and certificates of deposit.

The FDIC was created in 1933 to maintain stability and public confidence in the U.S. banking system following a period of rising bank failures. The FDIC introduced insurance coverage in 1934, and since then, insured depositors have not lost any deposits due to bank failure. The FDIC insures deposit products, not investments and other types of financial instruments. This means that if you have an IRA that invests in stocks, bonds, or mutual funds, it is not likely to be FDIC-insured, even if your bank is.

If you have accounts at different FDIC-insured banks, the $250,000 limit applies at each bank and for each account ownership category. You can use the FDIC's Electronic Deposit Insurance Estimator (EDIE) to calculate your specific insurance coverage amount. It is important to know how much money you have in different accounts within one institution to ensure your funds are fully covered.

It is worth noting that FDIC insurance does not cover losses from theft or fraud, only losses related to bank failure. FDIC insurance is also limited to $250,000 per person, per bank, and per account ownership category. This means that if you have deposits in excess of $250,000 at one bank, the excess portion would not be covered by the FDIC.

Saint Denis Bank: Location and Services

You may want to see also

![]()

FDIC insurance covers deposit accounts at FDIC-insured institutions

The Federal Deposit Insurance Corporation (FDIC) insures deposit accounts at FDIC-insured institutions, protecting customers' money in the event of bank failure. FDIC insurance covers checking accounts, savings accounts, money market deposit accounts, and certificates of deposit (CDs). It does not cover investments, such as stocks, bonds, mutual funds, or annuities.

The FDIC insurance limit is $250,000 per depositor, per bank, per ownership category. This means that if you have multiple accounts at the same bank, the total balance across all your accounts is insured up to $250,000. For example, if you have a savings account with $200,000 and a checking account with $50,000 at the same bank, your accounts are collectively insured for $250,000, leaving $50,000 uninsured.

Retirement accounts, including traditional IRAs and Roth IRAs, can be FDIC-insured if they are held at FDIC-insured banks and fall under the deposit account category. If you have an IRA with $150,000 in CDs and a Roth IRA with $150,000 in savings at the same bank, your total deposits of $300,000 would be insured up to the FDIC's maximum coverage of $250,000.

It's important to note that not all IRAs are FDIC-insured. If your IRA is invested in stocks, mutual funds, or annuity products, it is not protected by FDIC insurance, even if your IRA is held at an FDIC-insured institution. Additionally, IRAs held at credit unions or investment companies are typically not FDIC-insured but may be insured by other entities, such as the National Credit Union Administration (NCUA) or the Securities Investors Protection Corporation (SIPC).

To confirm if your IRA is FDIC-insured, you can check if your financial institution is FDIC-insured and ensure that your IRA is in the form of a deposit account. FDIC insurance provides peace of mind and guarantees that you won't lose your insured funds in the event of a banking crisis.

The Future of Truist Bank: Will It Survive?

You may want to see also

![]()

FDIC insurance doesn't cover all IRAs

The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance coverage for institutions such as banks, in the event that the bank fails and does not have enough assets to pay off depositors. FDIC insurance covers retirement accounts, including IRAs. However, FDIC insurance does not cover all IRAs.

FDIC insurance covers customer deposits held at FDIC-insured banks or savings and loan associations, including those held in IRA accounts. The limit on FDIC insurance is $250,000 per depositor, per bank, per ownership category. This means that a single bank customer could have $250,000 in FDIC insurance coverage for their IRA account, an additional $250,000 in coverage for their individual checking and savings accounts, and a third $250,000 in coverage as the beneficiary on a trust account—all at the same bank.

However, it's important to note that FDIC insurance does not cover all types of IRAs. If your IRA is invested in stocks, mutual funds, or annuity products, it is not protected by FDIC insurance, even if your IRA is held by an FDIC-insured institution. FDIC insurance only covers deposits, and certain types of accounts, such as checking accounts, savings accounts, and certificates of deposit. It does not cover investment products, securities, or other financial instruments.

Additionally, your IRA is not FDIC-insured if you hold it at a credit union or an investment company or brokerage. These types of accounts may be insured by other entities, such as the National Credit Union Association (NCUA) or the Securities Investors Protection Corporation (SIPC).

To summarize, while FDIC insurance does cover some IRAs, it is important to understand the limitations of this coverage. FDIC insurance only applies to certain types of accounts and investments, and it is essential to carefully consider where and how you hold your IRA to ensure that it is protected.

Fifth Third Bank: Which States Have Branches?

You may want to see also

Frequently asked questions

No, bank-held IRAs are FDIC-insured in most cases. The FDIC covers customer deposits at FDIC-insured banks, including those held in checking accounts, savings accounts, money market deposit accounts, and certificates of deposit (CDs).

The FDIC insurance limit is USD 250,000 per depositor, per bank, per ownership category. This means that if you have multiple IRAs at different banks, each of your IRAs is insured separately up to USD 250,000.

Your IRA may be FDIC-insured if your bank is, and if you have a deposit account instead of investments like stocks or mutual funds. You can check if your financial institution is FDIC-insured by searching the FDIC website.