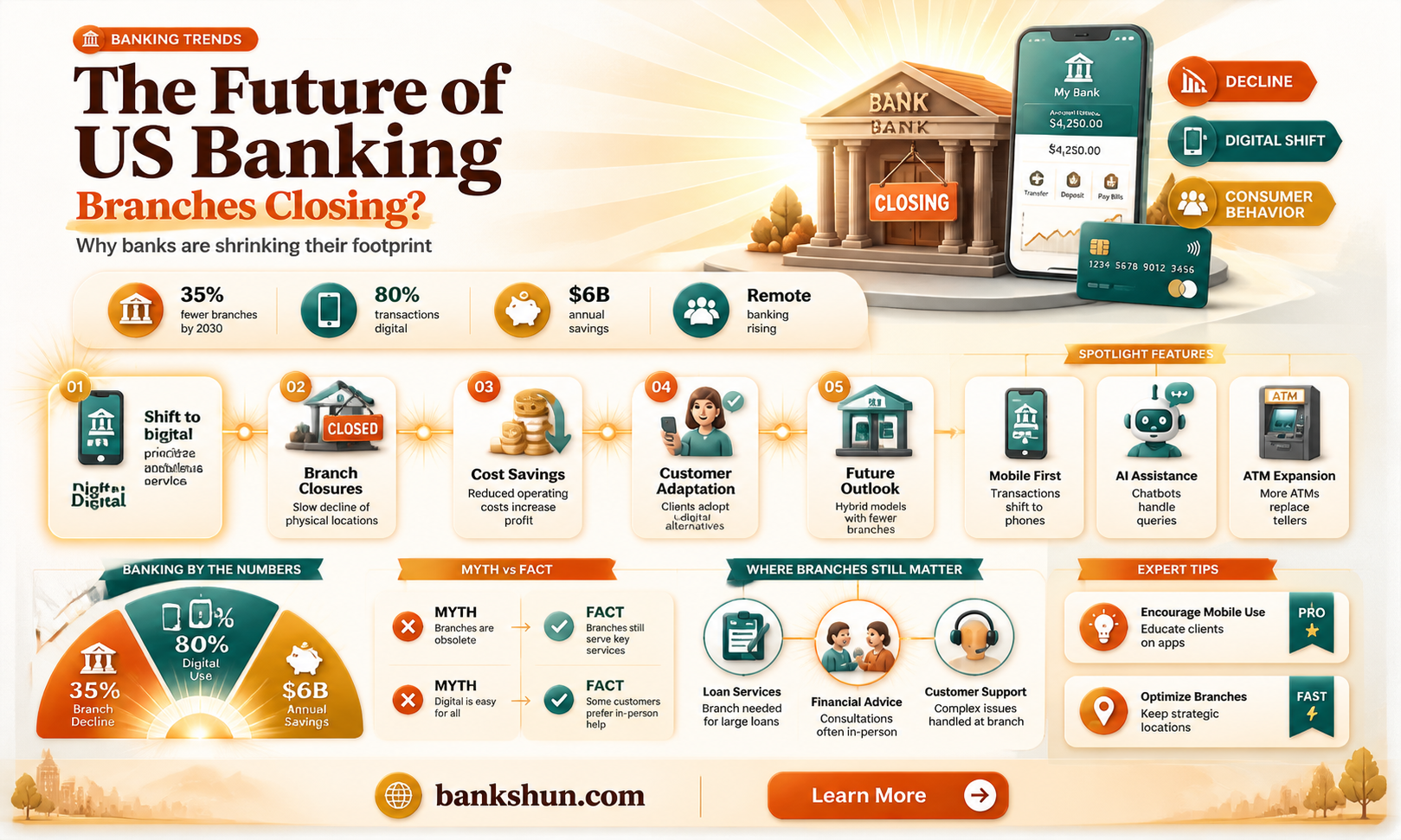

The COVID-19 pandemic has accelerated a shift towards online and mobile banking, resulting in a wave of bank branch closures across the United States. In the first 13 weeks of 2025 alone, more than 320 U.S. bank branches were marked for closure, with major institutions such as Wells Fargo, Bank of America, and JPMorgan Chase announcing the shuttering of many locations. This trend is not new, but the pandemic has doubled the rate of bank branch closures, with the majority coming from large banks, contributing to an overall 5.6% decline in total branches nationwide since 2020. While banks are not disappearing entirely, this shift towards digital banking is causing concern for those who rely on in-person services, particularly older adults, those with limited internet access, and people in rural or underserved communities.

| Characteristics | Values |

|---|---|

| Reason for bank closures | Changing consumer behavior, rise of online banking, and the COVID-19 pandemic |

| Banks closing branches | Flagstar Financial, TD Bank, Wells Fargo, Bank of America, U.S. Bank, PNC Bank, JPMorgan Chase |

| Number of closures | 32 banks closed in March 2025; 320 branches in the first 13 weeks of 2025; 40 U.S. Bank locations; 60 Flagstar branches |

| Impact | Reduced access to financial services, longer wait times, higher risk of financial exclusion, and the creation of "banking deserts" |

| States with most closures | California, Michigan, New York, Florida, and Illinois |

| Communities affected | Low-income, minority, rural, and older adults |

Explore related products

What You'll Learn

![]()

The shift to online banking

The rise of online banking has led to a reduction in branch visits and a shift in the role of physical bank locations. Banks are now repurposing their spaces to focus more on financial consultations and complex services like mortgage applications and lending, while routine transactions are increasingly carried out online. This shift has caused banks to reevaluate the necessity of maintaining a large physical presence, leading to the closure of many branches across the country.

While the move to online banking offers convenience to many, it has also raised concerns about accessibility. In-person banking remains essential for older adults, people with disabilities, those with limited internet access, and low-income communities. The closure of bank branches can result in reduced access to financial services, longer wait times, and the creation of "banking deserts", where communities are left without access to traditional banking services. This can lead to a reliance on non-traditional and high-fee lending options, exacerbating financial inequities.

To adapt to the changing landscape, banks are experimenting with alternative service models to bridge the gap left by branch closures. They are also investing in self-service kiosks and in-branch technology to enhance the online banking experience. As the trend towards digital banking continues, banks are expected to further optimize their digital platforms and services to meet the evolving needs of their customers.

Best Banks for Small Businesses: Where to Start?

You may want to see also

Explore related products

![]()

The impact of the pandemic

The COVID-19 pandemic has had a significant impact on the banking industry in the United States. While the banking sector demonstrated resilience during the initial phase of the pandemic, the long-term effects remain a concern.

During the early stages of the pandemic, U.S. commercial banks played a crucial role in supporting the economy. Between March and April 2020, commercial banks increased their lending by $700 billion, even as they had to add $100 billion to their loan and lease loss allowances. This expansion of lending occurred without raising concerns about liquidity or solvency, indicating the sector's strength and ability to withstand financial shocks.

However, the pandemic accelerated the trend of bank branch closures in the United States. Between 2017 and 2021, 9% of all branch locations closed, amounting to a loss of approximately 7,500 physical locations. The pandemic doubled the rate of closures, with more than 4,000 branches shutting down since March 2020. This has left many towns as "bank deserts," where residents face limited access to banking services and higher ATM fees. The absence of local banks can also lead to a decline in small business lending and activity, pushing individuals towards alternative financial services that may be unregulated and predatory.

The pandemic also contributed to a shift in customer behaviour, with a growing preference for digital banking services. Advances in mobile banking technology allowed customers to conduct transactions remotely while maintaining social distancing. Person-to-person payment services and mobile payment apps became increasingly popular, reducing the reliance on physical bank branches.

Additionally, the pandemic's economic fallout and the subsequent inflation surge impacted banks' capital reserves. As the Federal Reserve raised interest rates to curb inflation, bond prices declined, decreasing the market value of bank capital reserves. Some banks, such as Silicon Valley Bank, incurred losses and experienced liquidity issues, leading to a bank run in March 2023.

The pandemic also created opportunities for new intermediaries, such as hedge funds and venture capital firms, to step in as lenders. Borrowers sought alternative financing methods, and the abundance of private equity and venture capital reduced firms' exclusive reliance on bank funding.

Overall, the pandemic's impact on the banking industry in the United States has been mixed. While banks demonstrated resilience in the short term, the long-term effects, including branch closures, shifts in customer behaviour, and economic fallout, continue to shape the industry.

Wells Fargo Foreign Currency Exchange: What You Need to Know

You may want to see also

Explore related products

![]()

Bank branch closures in 2025

The COVID-19 pandemic has accelerated the shift towards online and mobile banking, resulting in a significant reduction in branch visits. This trend has continued into 2025, with more than 320 US bank branches marked for closure in the first 13 weeks of the year. Institutions such as Flagstar, TD Bank, Wells Fargo, and Bank of America are leading this transition, with some banks closing dozens of branches across the country.

The rise in bank closures is driven by a larger shift in consumer behaviour, as the use of mobile apps and online banking platforms increases. According to a study, over 200 million Americans still make transactions in branches, but the convenience and accessibility of digital banking have drawn many customers away from physical locations. This shift has been particularly prominent among younger generations, with Generation Zers visiting bank branches an average of 3.6 times per year, compared to 4.6 visits for baby boomers.

While most customers have embraced digital banking, older adults, individuals with disabilities, and those living on low incomes still depend on physical branches. This dynamic raises questions about accessibility and financial inclusion as banks reduce their physical presence. In-person banking remains vital for services like cash deposits, loan applications, and access to safety deposit boxes.

The Federal Reserve Bank of Philadelphia reported that between 2019 and 2023, the number of bank branches in the US decreased by 5.6%, and the number of Americans living in "banking deserts" increased by 760,000 to 12.3 million. This trend is expected to continue in 2025, with hundreds more bank branches slated for closure.

Some banks are adopting self-service kiosks and in-branch technology to enhance their digital offerings, while also repurposing space for financial consultations. As banks navigate changing consumer behaviour and technological advancements, the shift towards smaller locations or branch closures becomes an inevitable strategy to stay profitable.

Sasha Banks and Snoop Dogg: Family Ties?

You may want to see also

Explore related products

![]()

The changing role of bank branches

The COVID-19 pandemic and the subsequent shift in consumer behaviour have accelerated the transition to online and mobile banking, leading to a significant reduction in branch visits. Banks are closing physical stores and focusing on expanding their online presence. TD Bank, for instance, is closing its Massachusetts branches, while Flagstar Financial has announced it will close 60 branch locations and 20 private-client locations in 2025.

The shift towards online banking has resulted in banks adopting self-service kiosks and other in-branch technologies to facilitate online banking. They are also repurposing space to focus more on financial consultations and less on transaction services. This has led to banks shifting towards smaller locations and, in some cases, deciding to close branches altogether.

The closures have been criticised for creating "banking deserts", where communities, especially those in low-income and minority areas, are left without access to traditional banking services. This has resulted in residents having to travel farther to access banking services, increasing their reliance on non-traditional and high-fee lending options, and ultimately widening the wealth gap.

While the majority of customers have moved online, some consumers, especially older adults, those with disabilities, or those living on low incomes, still rely on physical branches. Banks are thus re-evaluating their physical footprints, with some banks investing in opening new branches and refurbishing their networks.

The remaining physical bank branches are evolving to focus on more complex financial services such as mortgage applications, small business lending, and personalised financial consultations, while routine banking moves online.

The Branch Manager: A Bank's Face and Leader

You may want to see also

Explore related products

![]()

The rise of banking deserts

While the shift to digital banking has been ongoing, the pandemic acted as a catalyst, causing a rapid increase in the rate of bank branch closures. Since 2020, the rate of bank branch closures in the US has doubled, with the majority of closures coming from large and very large banks. This has resulted in a 5.6% overall decline in total bank branches nationwide. In the first 13 weeks of 2025 alone, over 320 US bank branches were marked for closure, with institutions like Flagstar, TD Bank, Wells Fargo, and Bank of America leading this change.

The impact of these closures is felt disproportionately by certain communities. Low-income and majority-minority communities are more likely to be affected, as they may not have the same access to digital banking services. Additionally, older adults, people with disabilities, and those with limited internet access or living in rural communities may rely more on in-person banking services. The closure of local bank branches can result in reduced access to financial services, longer wait times, and an increased risk of financial exclusion for these communities.

The formation of "banking deserts," or communities without access to traditional banking services, has been a growing concern. Several Mid-Atlantic and New England states, including Delaware, Pennsylvania, New Jersey, and Vermont, experienced significant growth in these underserved areas between 2019 and 2023. The rise of banking deserts can lead to a higher reliance on non-traditional and high-fee lending options, such as payday loans and check-cashing services, which can widen the wealth gap and increase financial inequities.

While the trend towards digital banking is undeniable, banks are experimenting with alternative service models to bridge the gap left by branch closures. Branches that remain open are evolving to focus more on complex financial services, such as mortgage applications and financial consultations, rather than everyday transactions. Banks are also adopting self-service kiosks and in-branch technology to provide access to online banking services.

Best Banks for Instant Overdraft Access

You may want to see also

Frequently asked questions

Yes, banks are closing physical branches across the United States. In the first 13 weeks of 2025, over 320 U.S. bank branches were marked for closure.

The rise in bank closures is due to a shift in consumer behaviour. Since the pandemic, more people are choosing to bank online, reducing the need for physical branches.

Flagstar, TD Bank, Wells Fargo, Bank of America, U.S. Bank, PNC Bank, and JPMorgan Chase have all closed branches in the United States.

The shift towards online banking may pose challenges for those who rely on in-person services, including older adults, people with limited internet access, and those in rural communities. This may result in reduced access to financial services and increased financial exclusion.