The COVID-19 pandemic and other natural disasters have caused financial hardship for many, with some banks offering to suspend or reduce mortgage payments for those impacted. This is a temporary solution for those struggling to make ends meet, but it does not address the long-term financial impact. Borrowers can also apply for forbearance, which allows them to temporarily pause or reduce mortgage payments. However, the full amount is still owed and must be repaid later. It is important to contact your lender or servicer as soon as possible to understand your options and avoid losing your home.

| Characteristics | Values |

|---|---|

| Reason | Financial hardship due to the coronavirus pandemic |

| Who is eligible? | Customers impacted by the coronavirus pandemic |

| How long will the suspension last? | As long as the public health and economic disruptions last |

| What happens after the suspension? | Borrowers will resume making payments |

| What are the alternatives? | Negotiate a loan modification, transfer the mortgage to another lender, or extend the mortgage term |

Explore related products

What You'll Learn

- Natural disaster survivors may receive mortgage relief under the Mortgage Relief for Disaster Survivors Act

- The coronavirus pandemic caused banks to suspend mortgage payments for impacted customers

- Contact your mortgage servicer to find out what payment options are available to you

- If you are unsure about your ability to make mortgage payments, consider extending your mortgage term

- If you are facing foreclosure, there may be resources to assist you through your local bar association or legal aid

![]()

Natural disaster survivors may receive mortgage relief under the Mortgage Relief for Disaster Survivors Act

Natural disasters can have devastating effects on the lives of those impacted, leaving them with the challenge of picking up the pieces and rebuilding their homes and lives. In recognition of this, the Senate has introduced a bill that seeks to provide mortgage relief for up to six months for victims of natural disasters. This bill, known as the "Mortgage Relief for Disaster Survivors Act", aims to alleviate the financial burden on homeowners as they navigate the recovery process.

Under this proposed legislation, homeowners with federally-backed loans located in areas declared as disaster zones will be eligible for a 180-day reprieve from paying their mortgages without accruing any interest or penalties. This relief measure is intended to provide survivors with the necessary breathing room to stabilize their lives and finances without the added stress of immediate mortgage payments. The legislation also allows for the possibility of applying for a 180-day extension, recognizing that the recovery process can be lengthy and unpredictable.

The Mortgage Relief for Disaster Survivors Act comes as a response to the increasing frequency of natural disasters, such as wildfires and floods, that have ravaged states like California and Colorado. These states have experienced deadly wildfires and severe flooding, destroying homes and displacing families. The bill is co-sponsored by Democratic Senators Adam Schiff of California and Michael Bennet of Colorado, who understand firsthand the challenges their constituents face in the wake of these disasters.

While the bill specifically targets federal loans, it's worth noting that nonfederal lenders are not mandated to offer payment reprieves in disaster zones. However, in the past, after incidents like the Palisades and Eaton fires, over 400 lenders voluntarily agreed to a 90-day pause without reporting missed payments to credit agencies. This demonstrates a willingness on the part of some lenders to provide relief to disaster survivors, even outside the scope of federal legislation.

The Mortgage Relief for Disaster Survivors Act is a testament to the ongoing efforts to support communities affected by natural disasters. By providing financial assistance and reducing the immediate pressure of mortgage payments, survivors can focus on recovery and rebuilding their lives without the looming threat of foreclosure or financial strain. This bill, if passed, would offer a crucial lifeline to those struggling in the aftermath of natural disasters.

PNC Bank Arts Center: Location, Events, and More

You may want to see also

Explore related products

$36.62 $27

![]()

The coronavirus pandemic caused banks to suspend mortgage payments for impacted customers

The coronavirus pandemic has had a devastating impact on the global economy, with many people losing their jobs and livelihoods. In light of this, banks have had to step in and offer some relief to impacted customers, including suspending mortgage payments.

In California, Governor Gavin Newsom announced that four of the nation's five biggest banks, including Wells Fargo, U.S. Bank, Citibank, and J.P. Morgan Chase, would be offering 90-day mortgage waivers for those impacted by COVID-19. This was a result of negotiations between the governor and the banks to provide financial relief for struggling homeowners. Over 1 million Californians filed for unemployment benefits, and the governor warned that a sudden rush of calls from homeowners to banks could overwhelm the system.

Some banks offered more than 90 days of relief. Truist Bank, for example, offered mortgage forbearance and deferral options, which could move the balloon payment to the end of the loan. US Bank offered assistance programs that allowed customers to suspend payments for up to 180 days without late fees. JP Morgan also offered a 90-day forbearance with no late fees and suspended foreclosure activity during the assistance period.

While these measures provided much-needed relief for homeowners, some customers still faced challenges. There were consumer complaints about balloon payments under JPMorgan's forbearance program, with one customer stating they lost their job during the COVID-19 crisis and were unable to pay their mortgage. This highlights the potential pitfalls of forbearance programs, where customers may struggle to make the full payment at the end of the forbearance period.

PNC Bank's Virtual Wallet: What's the Deal?

You may want to see also

Explore related products

![]()

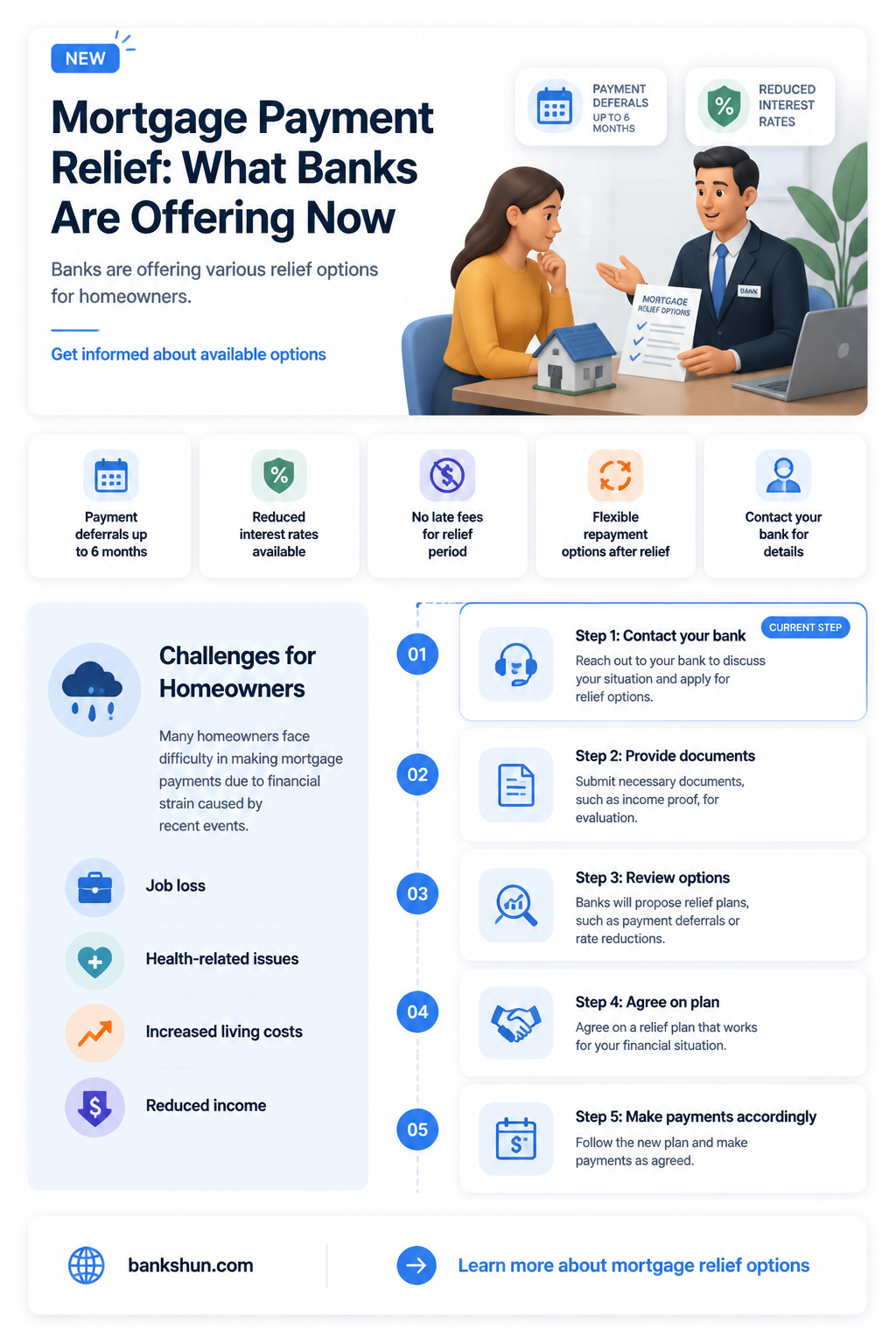

Contact your mortgage servicer to find out what payment options are available to you

If you are facing difficulty making your mortgage payments, it is important to contact your mortgage servicer as soon as possible. This process can be time-consuming and stressful, so it is best to be proactive and understand your options.

Your mortgage servicer can discuss the available payment options with you. For example, you may be offered a reduced monthly interest rate or a halt in interest payments. You may also be able to request an extension of up to 18 months of forbearance. It is important to note that this process can be expensive, so it is crucial to have all your important documents, such as your mortgage agreement, loan documents, and tax returns, readily available.

If you are unsure about your future income and are concerned about keeping up with your mortgage payments, you may want to consider extending your mortgage term. This option can provide you with the security of maintaining your homeownership status. However, it is important to note that this option is only available until your 75th birthday or retirement, whichever comes first.

Additionally, you can explore other options with your lender, such as negotiating a loan modification or transferring your mortgage to another lender. In some cases, you may need to consider filing for bankruptcy if other options are not feasible.

During times of crisis, such as the coronavirus pandemic or natural disasters, mortgage relief options may be available. Some banks and lenders may offer temporary suspension of mortgage payments or provide relief for a certain period. Staying informed about such options can help you navigate financial hardships effectively.

Coin Deposits During COVID-19: Are Banks Accepting?

You may want to see also

Explore related products

![]()

If you are unsure about your ability to make mortgage payments, consider extending your mortgage term

The COVID-19 pandemic has caused financial hardship for many, leading some banks to suspend mortgage payments for those impacted. However, this is only a temporary solution, and it's important to consider long-term financial strategies. If you're unsure about your ability to make mortgage payments, one option to consider is extending your mortgage term. This can provide short-term relief by lowering your monthly payments, but it's important to carefully weigh the advantages and disadvantages.

Extending your mortgage term can be advantageous if you have an interest-only mortgage and need more time to pay off the total loan amount. It's also a good option if you're facing new major monthly expenses or if your interest rates are set to rise, making repayments at current terms unaffordable. For example, let's consider Sarah, who took out a 25-year repayment mortgage of £200,000 at an interest rate of 3%, with monthly payments of £948. Due to rising interest rates, her lender now offers a new deal at 5%. If Sarah keeps her remaining 20-year term, her new monthly payment would increase to £1,319. However, by extending her mortgage to 30 years, she can reduce her monthly payment to £1,074, saving her £245 per month.

While extending the mortgage term provides short-term relief, it's important to understand that you will pay more in interest over the total term of your mortgage. In Sarah's case, with the extended 30-year term at 5%, she would pay a total interest of £186,511, which is £69,951 more than the original 20-year term. This highlights the trade-off between short-term savings and long-term interest costs. Additionally, if you're nearing retirement, lenders may be cautious about offering an extended mortgage term, and some may have maximum age limits or require proof of retirement income.

If you're considering extending your mortgage term, it's crucial to contact your lender and discuss your options. They may perform an affordability assessment to ensure that the extended term is suitable for your financial situation. It's important to be proactive and stay informed about the terms of your mortgage to make the best decision for your financial future.

In summary, if you're unsure about your ability to make mortgage payments, extending your mortgage term can provide short-term relief by lowering your monthly payments. However, it's important to carefully consider the long-term implications, as you will pay more in interest over the total mortgage term. Contacting your lender and seeking their guidance is a crucial step in navigating this complex financial decision.

Second Chance Banking: Who Offers a Fresh Start?

You may want to see also

Explore related products

![]()

If you are facing foreclosure, there may be resources to assist you through your local bar association or legal aid

During the coronavirus pandemic, some banks offered to suspend mortgage payments for customers who had been impacted. However, this was a short-term solution, and many people continue to struggle financially. If you are facing foreclosure, there are resources to assist you through your local bar association or legal aid.

The Washington State Bar Association, for example, offers free legal assistance to low- and moderate-income homeowners through the Home Foreclosure Legal Aid Project. This project provides legal advice and representation to those facing the possibility of losing their homes. The Northwest Justice Project's Foreclosure Prevention Unit also helps people who are threatened with home foreclosure.

If you are facing foreclosure, it is important to be proactive and stay informed about your options. You can also contact your lender to discuss a loan modification or a short-term extension. Additionally, you may consider transferring your mortgage to another lender. Legal aid services can provide you with information and support throughout this process, helping to reduce the damage and ensure your life returns to normal as smoothly as possible.

To find legal aid near you, you can visit LawHelp.org, which provides free legal aid and answers to legal questions for people with low to moderate incomes. The American Bar Association also offers a similar service, allowing low-income individuals to ask legal questions online. These services can provide you with the resources and assistance you need when facing foreclosure.

US Bank Stadium: Home of the Vikings in Minneapolis

You may want to see also

Frequently asked questions

Banks may suspend mortgage payments on a case-by-case basis. During the coronavirus pandemic, some banks offered to suspend mortgage payments for customers who had been impacted.

Contact your mortgage servicer as soon as possible to discuss your options. They may offer you a reduced monthly interest rate, a halt in interest payments, or a short-term extension.

You could consider extending your mortgage term. There is usually no age limit for extending your mortgage, but this can only be done up to your 75th birthday or retirement, whichever comes first.

It is critical that you understand the terms of the mortgage offer. Read all the information about your offer and look for a section detailing the circumstances under which it may be revoked.

There may be resources to assist you through your local bar association or legal aid. You could also negotiate a loan modification with your lender or transfer your mortgage to another lender.