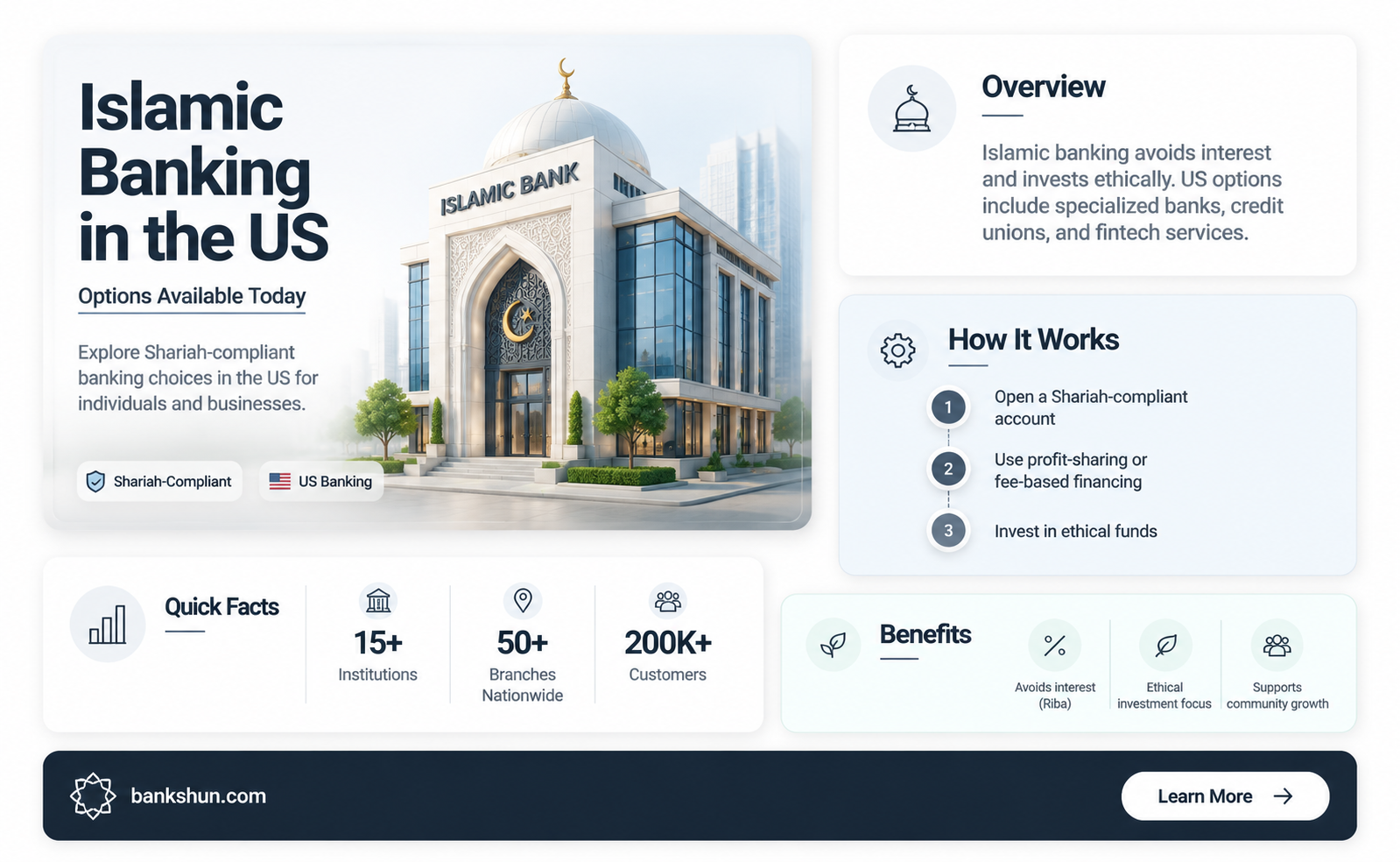

Islamic finance in the United States is a small but growing industry. While there are no fully-fledged Islamic banks in the USA, some banks offer Islamic financial products that comply with Sharia law. These include Stearns Salaam Banking, a division of Stearns Bank N.A., which offers a full suite of Islamic banking products, including checking and savings accounts, as well as financing products for consumers, businesses, and nonprofits. Maun Credit Union is another example of an Islamic financial institution in the US, offering interest-free loans. Regulatory issues pose a significant barrier to the establishment of Islamic banks in the US, as the current framework is geared towards conventional banking.

| Characteristics | Values |

|---|---|

| Nature of Islamic banks in the USA | Islamic banks in the USA are not a sprawling network of institutions explicitly branded as "Islamic banks". However, the spirit and substance of Islamic finance are very much alive and flourishing across the country. |

| Regulatory framework | There are no US laws specifically addressing Islamic banking. The regulatory framework is a hurdle for the creation of Islamic financial institutions within the existing system. |

| Islamic finance services | Islamic finance services include Sharia-compliant banking, home financing, personal financing, and investment services. |

| Islamic finance market | The Islamic finance market grew substantially in many parts of the USA. |

| Islamic banking windows | There were 207 Islamic banking windows in 2021. |

| Islamic finance transactions | Islamic finance transactions constitute only 1% of global financial assets. |

| Islamic finance in the UK | The UK has a plethora of Islamic financing services, with over 20 banks, six of which exclusively provide Sharia-compliant products. |

Explore related products

What You'll Learn

![]()

Islamic finance in the USA

Islamic finance is based on a profit and loss structure rather than a lender–borrower arrangement. This requires that a financial institution enter into a joint venture with a client to provide capital. The risk associated with the joint venture entitles the financial institution to profit from the financial transaction. While this concept is relatively new in the US, it is widely practiced in other countries. For instance, in Egypt, Indonesia, Malaysia, Sudan, and the Gulf States, Islamic banking coexists with conventional banking. In some countries, like Iran and Pakistan, Islamic banks are the only mainstream financial institutions.

There are a few financial entities that offer formal Islamic finance in the US, such as SHAPE Financial and Reba Free, which supply the market with predesigned Sharia-approved products. These are for-profit ventures that work with financial entities rather than Muslim customers. UIF Corporation, which is a faith-based subsidiary of University Bank, is another example of an Islamic financing institution in the US.

Islamic finance in the US is a small but growing industry. Experts have identified three distinct levels of observance in the Muslim community. The first third represents the most observant, who do not use conventional financing. This group represents the core market for Islamic financing arrangements. The next third consists of Muslims who currently use conventional financing but might switch to Islamic financing if it was more widely available. The final third consists of those who currently use conventional financing and may continue to do so even if a religiously compliant alternative was available.

There are some challenges to the growth of Islamic finance in the US. Regulatory issues have not yet been tested on a large scale, and the regulatory framework is geared towards conventional banking. There are regulations for reporting, the products banks can offer, and more. New regulations would likely need to be passed for an Islamic bank to exist in the US.

American Banks in Fiji: Exploring the Presence

You may want to see also

Explore related products

![]()

Islamic banking windows

The concept of Islamic banking windows provides a convenient entry point for customers seeking Sharia-compliant financial solutions. However, their growth has been relatively limited compared to dedicated Islamic financial institutions due to various challenges. Regulatory hurdles, the complexity of adapting conventional systems for Sharia compliance, and the need for ongoing Sharia board oversight are significant obstacles.

The pragmatic approach of Islamic banking windows within mainstream financial providers ensures that Islamic finance is a growing reality in the United States. It offers a powerful, ethical alternative for individuals seeking financial solutions rooted in the values of justice, transparency, and shared prosperity.

While the number of Islamic banking windows might be limited compared to dedicated institutions, their existence signifies the recognition of the demand for Sharia-compliant financial services within the mainstream financial sector in the United States.

Stadium Seating Capacity: US Bank Stadium

You may want to see also

Explore related products

![]()

Sharia-compliant products

While there are no Islamic banks in the USA, there are still Sharia-compliant products available to investors. These funds are investment funds that comply with Islamic law and are considered a type of socially responsible investing.

Sharia-compliant funds have many requirements that must be met. For example, they must exclude investments that derive the majority of their income from the sale of alcohol, pork products, pornography, gambling, military equipment, or weapons. They must also appoint a Sharia board, perform an annual Sharia audit, and purify certain prohibited types of income, such as interest, by donating them to charity.

There are several Sharia-compliant investment funds provided by Saturna Capital through its Amana series. The Amana Growth Fund (AMAGX) was launched on February 3, 1994, and seeks long-term capital growth through investments adhering to Islamic principles. This fund invests at least 80% of its assets in common stocks. Additionally, the Islamicly app is the world's first Sharia-certified app for Sharia-compliant equities, allowing users to find and monitor the halal status of stocks.

According to a source, 49.02% of total listed stocks in the USA comply with Sharia Principles. This provides Sharia-sensitive investors with multiple options to make investments in a Sharia-compliant manner.

Repossessed Cars: A Good Deal or a Money Pit?

You may want to see also

Explore related products

![]()

Regulatory hurdles

Islamic finance in the United States faces several regulatory hurdles due to the inherent differences between Sharia principles and the largely interest-based US financial regulatory framework. The financial services industry is highly regulated, and the regulatory framework is geared towards conventional banking. This poses a significant challenge for the establishment of Islamic banks, which operate according to different principles and requirements.

One of the key regulatory hurdles is the issue of interest, which is prohibited in Islam. In contrast, the US financial system is deeply intertwined with the concept of interest, affecting various aspects such as how the FDIC calculates deposit insurance, capital regulation, and loan structures. Islamic financial products, such as those offered by credit unions and cooperative funds, tend to operate on a profit-sharing model rather than interest, which requires innovative structuring to comply with regulatory requirements.

Another challenge arises from the unique features of Islamic financial products. For example, banks in the US are typically prohibited from taking on partnership or equity stakes in real estate. However, in Islamic finance, the bank assumes formal ownership through structures like ijara and murabaha mortgage products. While regulators have approved these products in some cases, finding structures that comply with both Sharia principles and US regulations can be complex and limit the availability of certain financial products.

The cost of offering new and innovative products that have little precedent in the US market is another regulatory hurdle. Financial institutions offering Islamic financial products must incur costs related to research, document creation, consultations with experts, and staff training. While some of these costs are passed on to customers, many are absorbed by the institutions themselves, impacting their profitability.

Furthermore, the smaller secondary market for Islamic financial products has made it more challenging for Islamic mortgage lenders to maintain liquidity and expand their market presence. This limited liquidity can hinder the growth of the industry and the availability of Islamic financial services in the US.

While regulatory agencies have shown interest in building their knowledge of Islamic finance, the lack of Muslim representation in government and regulatory authorities can slow down the process of accommodating Islamic banking within the existing regulatory framework.

Ecuador Bank CD Rates: A Falling Trend?

You may want to see also

Explore related products

![]()

Islamic financial institutions

Islamic finance is a rapidly expanding sector built on ethical principles derived from Islamic law. While there may not be a vast network of conventional Islamic banks in the US, the spirit and substance of Islamic finance are very much alive and flourishing across the country. There are about 15 financial institutions that operate on an "interest-free" basis, offering a wide range of Sharia-compliant products and services, including home financing, personal financing, and investment services. These Islamic financial institutions (IFIs) operate as state-chartered entities, subject to state and federal laws regulating corporate governance, banking, and insurance operations.

The US market for Islamic financial products is smaller than that of the United Kingdom, where there are US$19 billion worth of assets owned by Islamic financial institutions and more than 20 banks, six of which exclusively provide Sharia-compliant products. However, Islamic banking is the largest sector in the Islamic finance industry, contributing to 71% or US$1.72 trillion of the industry's assets. The sector is supported by commercial, wholesale, and other types of banks, with commercial banking being the main contributor to its growth. There were 505 Islamic banks in 2021, including 207 Islamic banking windows.

The growth of the Islamic finance market in the US is driven by investment opportunities in promising Islamic sectors. Trillions of dollars are expected to accelerate economic recovery, and investors are showing interest in new performance and Islamic-based ESG and sustainability-linked debt products (SLDs). Islamic finance-based SLDs are believed to create new avenues for sustainable growth that serves the markets. Additionally, initiatives in sustainable finance are gaining momentum in countries like Somalia, where efforts to tackle climate change and foster inclusive economic growth are underway.

While the regulatory framework in the US presents challenges for the establishment of Islamic banks, specialised institutions, innovative fintech solutions, and dedicated product windows within mainstream providers enable the practical application of Islamic finance in America. This evolving landscape invites individuals to explore financial paths that benefit not just their individual wealth but also their conscience, promoting values of justice, transparency, and shared prosperity.

Which Banks Offer Cash Incentives to Switch?

You may want to see also

Frequently asked questions

Yes, there are a few examples of Islamic financial institutions in the US, including Stearns Salaam Banking, Maun Credit Union, and Dubai Islamic Bank. However, it is important to note that Islamic banking in the US is a small but growing industry, with a limited number of institutions offering formal Islamic financing products.

Islamic finance is the act of providing financial products or services that conform to Islamic law. It is based on a profit and loss structure rather than a lender-borrower arrangement. This means that a financial institution enters into a joint venture with a client to provide capital. Islamic banking does not involve the payment or receipt of interest, which is prohibited under Sharia law.

One of the biggest challenges of Islamic banking in the US is the regulatory framework, which is geared solely towards conventional banking. New regulations would likely need to be passed for Islamic banking to be fully accommodated in the US. Additionally, there is a lack of Muslim representation in the government and regulatory authorities, which makes it less likely that changes will be made to accommodate Islamic banking.

Islamic banking provides an opportunity for religiously observant Muslim families to access financial products that comply with their religious beliefs. It allows Muslims who were previously unable to pay or receive interest to become homeowners and participate in the financial system while upholding their values.