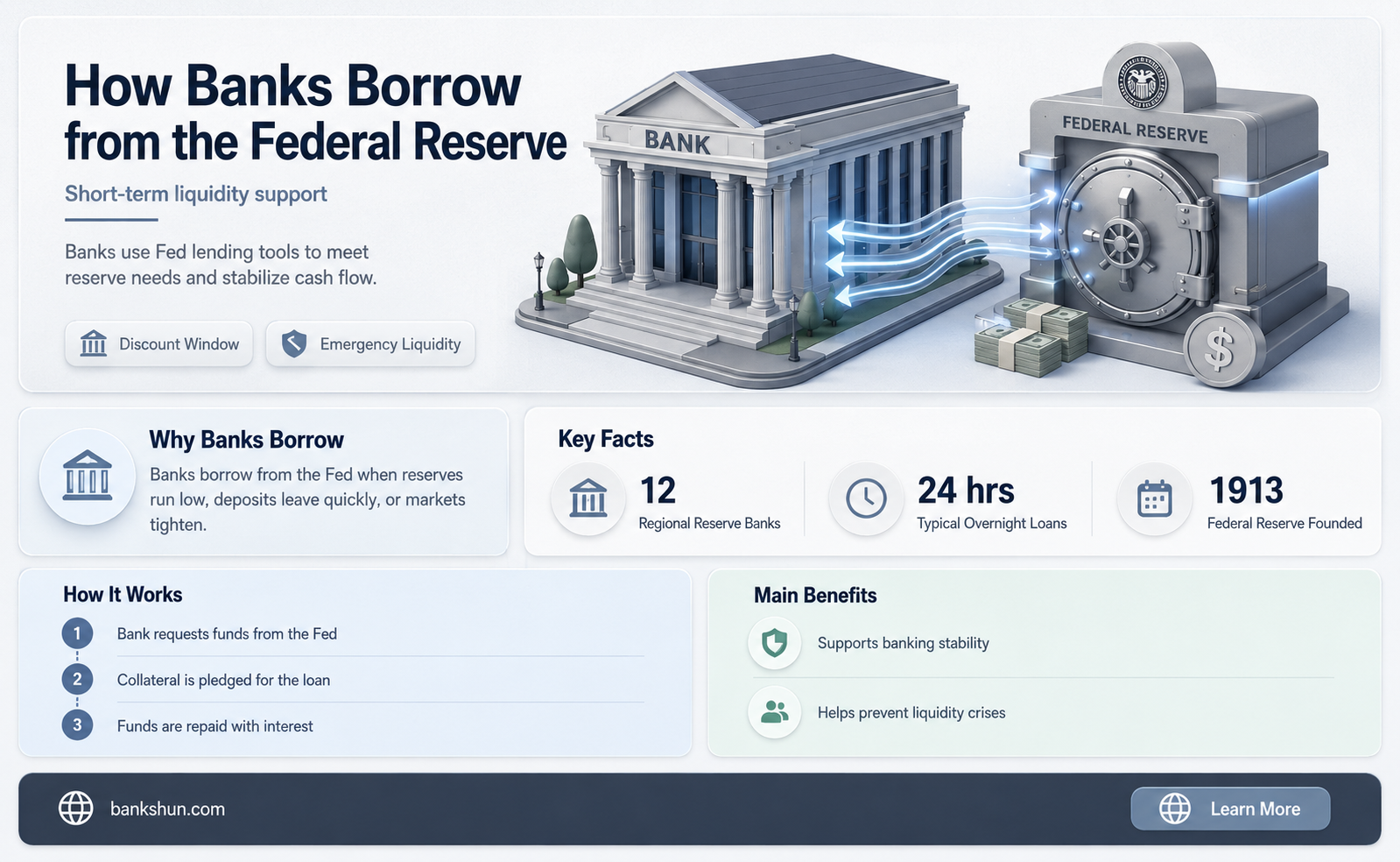

The US Federal Reserve System, also known as the Fed, is the country's central banking system and the world's most powerful economic institution. It is responsible for setting interest rates, managing the money supply, and regulating banks and the US payment system. Banks can borrow from the Federal Reserve when they require more capital to meet immediate withdrawal requirements or other liquidity issues. The Fed provides loans to member banks through its discount window using what is called the discount rate. This rate is used as the ceiling for its target rate range.

| Characteristics | Values |

|---|---|

| Purpose of Federal Reserve | To provide the nation with a safe, flexible, and stable monetary and financial system |

| Core responsibilities | Setting interest rates, managing the money supply, and regulating banks and the U.S. payment system |

| Role in lending to banks | Provides loans to member banks through its discount window using what is called the discount rate |

| Who can borrow? | Commercial banks |

| When can banks borrow? | When they require more capital to meet immediate withdrawal requirements or other liquidity issues |

| Interest rate | The Federal Reserve charges banks the discount rate, which is used as the ceiling for its target rate range |

| Preference | The Federal Reserve encourages banks to borrow from and lend to each other, rather than from the discount window |

| Types of credit | Primary credit, secondary credit, and seasonal credit |

| Primary credit | Available for banks in stable financial conditions |

| Secondary credit | For depository institutions that do not qualify for primary credit |

| Seasonal credit | Helps small depository institutions manage significant swings in their loans and deposits |

Explore related products

What You'll Learn

- Banks borrow from the Federal Reserve to meet temporary liquidity requirements

- The Federal Reserve encourages banks to borrow from each other

- The Federal Reserve offers three discount window programs

- The Federal Reserve acts as a lender of last resort

- The Federal Reserve influences the supply of money in the economy

![]()

Banks borrow from the Federal Reserve to meet temporary liquidity requirements

Banks borrow from the Federal Reserve, or the Fed, to meet temporary liquidity requirements. The Fed provides loans to member banks through its discount window using what is called the discount rate. Banks can borrow at the discount rate from the Federal Reserve when they require more capital to meet immediate withdrawal requirements or other liquidity issues. The Fed charges banks the discount rate, which is used as the ceiling for its target rate range. The Federal Reserve encourages banks to borrow from and lend to each other, rather than from the discount window.

Lending activity or a temporary liquidity crisis can deplete a commercial bank's cash reserves and leave it unable to support withdrawals. When a bank is in this state, it can borrow from another bank at a rate that falls somewhere in between the Federal Reserve's target rate range. Banks can opt to borrow from other banks, but they may not always find a lender. The Fed offers three discount window programs to depository institutions: primary credit, secondary credit, and seasonal credit. Primary credit is available for banks in stable financial conditions, while secondary credit is for depository institutions that do not qualify for primary credit. Seasonal credit helps small depository institutions manage significant swings in their loans and deposits.

The Federal Reserve, the central bank of the United States, provides the nation with a safe, flexible, and stable monetary and financial system. Providing liquidity in this way is one of the original purposes of the Federal Reserve System and other central banks around the world. The discount window plays an important role in supporting the liquidity and stability of the banking system and the effective implementation of monetary policy. By providing ready access to funding, the discount window helps depository institutions manage their liquidity risks efficiently and avoid actions that have negative consequences for their customers, such as withdrawing credit during times of market stress.

Are FaZe Banks and Alissa Violet Dating?

You may want to see also

Explore related products

![]()

The Federal Reserve encourages banks to borrow from each other

Banks can borrow from the Federal Reserve System (FRS) to meet temporary liquidity requirements. The Federal Reserve provides loans to member banks through its discount window using the discount rate. The discount rate is the ceiling for the Fed's target rate range. Banks can borrow at the discount rate from the Federal Reserve when they require more capital to meet immediate withdrawal requirements or other liquidity issues.

The Federal Reserve charges higher interest rates on its loans to encourage banks to borrow from each other. The Federal Reserve creates a range of interest rates for banks to use when they lend to other banks. The Federal Open Market Committee (FOMC) publishes the latest rate ranges eight times per year. These statements are used to stabilize the economy and encourage bank-to-bank lending. The Federal Reserve lends to depository institutions to assist with temporary funding issues.

The Federal Reserve, the central bank of the United States, provides the nation with a safe, flexible, and stable monetary and financial system. The Federal Reserve's lending to depository institutions plays an important role in supporting the liquidity and stability of the banking system and the effective implementation of monetary policy. By providing ready access to funding, the discount window helps depository institutions manage their liquidity risks efficiently and avoid actions that have negative consequences for their customers, such as withdrawing credit during times of market stress. Thus, the discount window supports the smooth flow of credit to households and businesses.

Understanding Deductible Bank Charges on Schedule C

You may want to see also

Explore related products

$14.95

$15.99

![]()

The Federal Reserve offers three discount window programs

Banks borrow from the Federal Reserve System (FRS) to meet temporary liquidity requirements. The Federal Reserve offers three discount window programs to depository institutions: primary credit, secondary credit, and seasonal credit. Each program has its own interest rate, or "'discount rate'", which is established by each Reserve Bank's board of directors and subject to review and determination by the Board of Governors of the Federal Reserve System. The rates for the three lending programs are the same across all Reserve Banks.

Primary credit is a lending program that serves as the principal safety valve for ensuring adequate liquidity in the banking system. It is available for banks in stable financial conditions and can be used as a backup source of short-term funds. After an institution is signed up for the discount window and has pledged collateral, the only other information the borrower needs to supply to their lending Reserve Bank when requesting an advance is the amount and term of the loan requested. Funds borrowed under the primary credit program can be used in the same way as funds borrowed from any other liquidity source.

Secondary credit is a lending program available to depository institutions that do not qualify for primary credit. It is typically extended on a very short-term, overnight basis at a higher rate than the primary credit rate. There are restrictions on the uses of secondary credit extensions; it may not be used to fund an expansion of the borrower's assets. The secondary credit program also entails a higher level of Reserve Bank administration and oversight than the primary credit program.

Seasonal credit helps small depository institutions manage significant swings in their loans and deposits. It is available to assist small depository institutions with demonstrated liquidity pressures of a seasonal nature and is typically not available to institutions with deposits of $500 million or more. The interest rate applied to seasonal credit is a floating rate based on market rates.

Apple and Goldman Sachs: Physical Banks or Not?

You may want to see also

Explore related products

![]()

The Federal Reserve acts as a lender of last resort

Banks borrow from the Federal Reserve System (FRS) to meet temporary liquidity requirements. The Federal Reserve acts as a lender of last resort, providing emergency credit to financial institutions that are struggling financially and near collapse. This is one of the original purposes of the Federal Reserve System and other central banks around the world.

The Federal Reserve, the central bank of the United States, provides the nation with a safe, flexible, and stable monetary and financial system. The Federal Reserve System worked with the Treasury and other parts of the US government during the Great Financial Crisis to limit the damage caused by the crisis. The Fed deploys its lender-of-last-resort function to prevent the collapse of financial institutions and economic contagion.

The Fed provides loans to member banks through its discount window using what is called the discount rate. Banks can borrow at the discount rate from the Federal Reserve when they require more capital to meet immediate withdrawal requirements or other liquidity issues. The discount window helps depository institutions manage their liquidity risks efficiently and avoid actions that have negative consequences for their customers, such as withdrawing credit during times of market stress. Thus, the discount window supports the smooth flow of credit to households and businesses.

The Fed charges banks the discount rate, which is used as the ceiling for its target rate range. The Federal Reserve encourages banks to borrow from and lend to each other, rather than from the discount window. Lending activity or a temporary liquidity crisis can deplete a commercial bank's cash reserves and leave it unable to support withdrawals. When a bank is in this state, it can borrow from another bank at a rate that falls somewhere in between the Federal Reserve's target rate range.

Finding M&T Bank: Nearest Branch Locator

You may want to see also

Explore related products

![]()

The Federal Reserve influences the supply of money in the economy

The Federal Reserve System, or the Fed, is the US central banking system and the most powerful economic institution in the country, if not the world. Its core responsibilities include setting interest rates, influencing the supply of money in the economy, and regulating banks and the US payment system.

One of the ways the Fed influences the supply of money in the economy is by lending money to banks. Banks can borrow from the Fed to meet temporary liquidity requirements. The Fed provides loans to member banks through its discount window using the discount rate. Banks can borrow at this rate when they require more capital to meet immediate withdrawal requirements or other liquidity issues. The discount window rate is set by the Federal Open Market Committee (FOMC) and is used as the ceiling for the Fed's target rate range. The Fed encourages banks to borrow from each other, rather than from the discount window, to avoid negative consequences for their customers, such as withdrawing credit during times of market stress.

The Fed influences the supply of money in the economy by setting a target interest rate policy for the federal funds rate. This is the rate at which commercial banks borrow and lend excess reserves to other banks on an overnight basis. The Fed raises or lowers this rate to impact underlying economic conditions. For example, in 2022, as inflation surged, the FOMC began raising interest rates to make borrowing more expensive and slow economic activity. The Fed's strategy was designed to ease pricing pressures and reduce the inflation rate. In periods when the economy is slow or in a recession, the Fed tends to lower rates to try to stimulate economic activity and help the economy expand again.

The Fed also influences the supply of money in the economy through open-market operations, such as purchasing bonds and other assets. By purchasing bonds, the Fed increases the amount of reserves in the banking system, helping to lower the federal funds rate and ease borrowing conditions. During recent challenging economic periods, the Fed purchased US government bonds and mortgage-backed securities to boost economic activity. The Fed's market actions helped moderate longer-term borrowing costs.

Key Banks in North Carolina: Where Are They?

You may want to see also

Frequently asked questions

Banks borrow from the Federal Reserve to meet temporary liquidity requirements. This is done to support the liquidity and stability of the banking system and the effective implementation of monetary policy.

The discount window is the rate assigned by the Federal Open Market Committee (FOMC) which is used as the ceiling for the Fed's target rate range. Banks borrow at the discount rate from the Federal Reserve when they require more capital to meet immediate withdrawal requirements or other liquidity issues.

There are three types of credit available at the discount window: primary credit, secondary credit, and seasonal credit. Primary credit is available for banks in stable financial conditions, secondary credit is for depository institutions that do not qualify for primary credit, and seasonal credit helps small depository institutions manage significant swings in their loans and deposits.