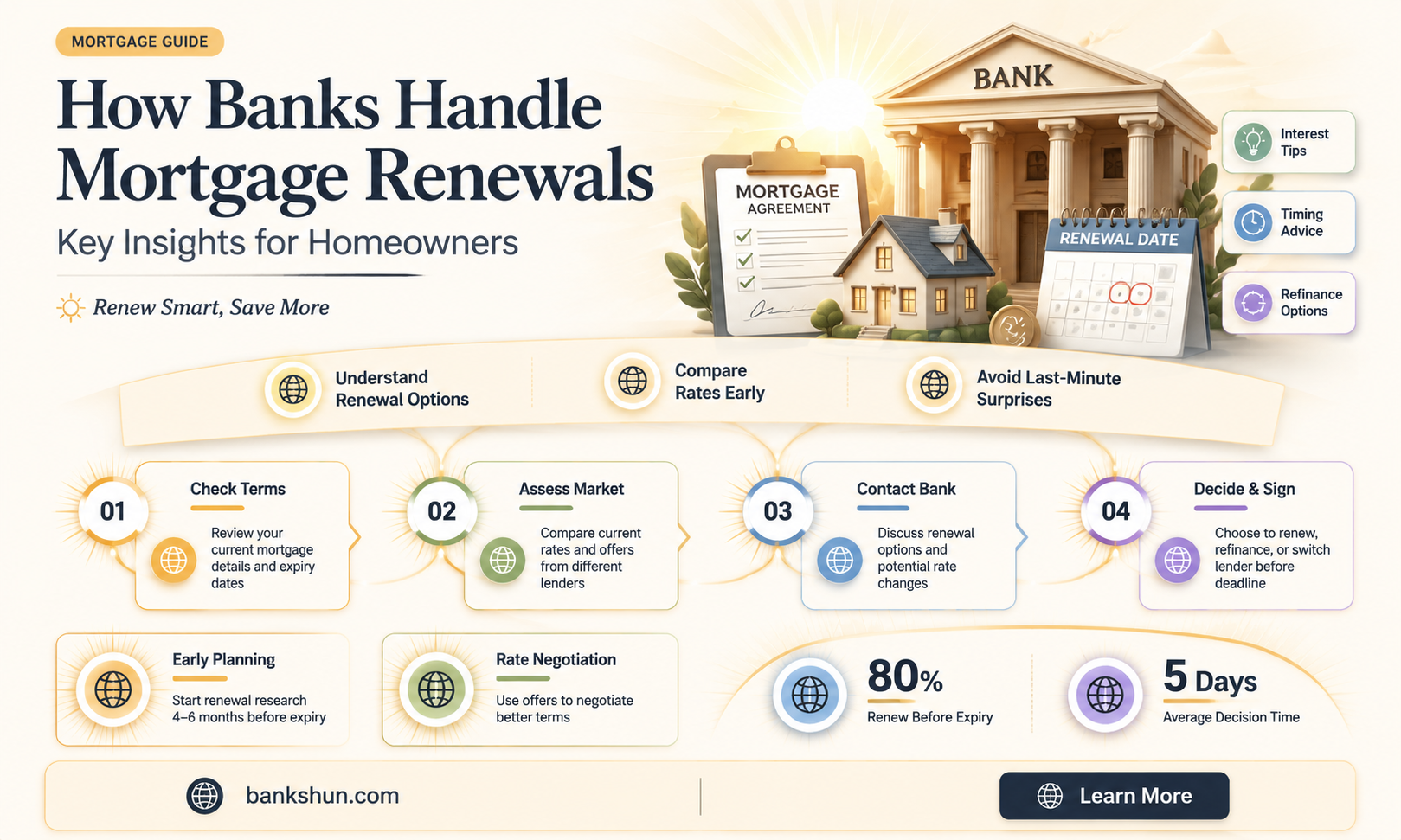

When your mortgage term ends, you have the option to either pay off your mortgage in full or renew it. Renewal allows you to review and adjust your mortgage term, type, payment frequency, and other features to suit your changing needs and goals. You can renew your mortgage with your current lender or move to another lender with better conditions. It is recommended to start exploring your options a few months before the end of your term, as your lender may automatically renew your mortgage term, which may not get you the best interest rate and conditions.

| Characteristics | Values |

|---|---|

| Renewal options | Review your mortgage needs, make changes to your mortgage term, type, payment frequency or other features |

| Renewal time | Renewal process starts about 5 months before maturity date |

| Renewal process | Review renewal documents, select a renewal option, sign and return the documents before the renewal date |

| Renewal flexibility | You don't have to renew with the same lender; you can move your mortgage to another lender if their conditions better suit your needs |

| Renewal benefits | Renewing early can help save on interest costs if rates rise before the regular renewal date |

Explore related products

$16.53 $22.99

What You'll Learn

![]()

You don't have to stick with your current lender

When it comes time to renew your mortgage, it is important to remember that you don't have to stick with your current lender. While it might be more straightforward and quicker to renew with your current lender, it is worth shopping around to see what other lenders are offering.

There are a few reasons why you might want to switch lenders. Firstly, your financial situation may have changed since you took out your original mortgage, and you may now qualify for better rates or terms with a different lender. Secondly, you may be seeking a better offer than what your initial lender provided. Perhaps your current lender sold your mortgage to another company, and you are unhappy with the new servicer. Or maybe you want to access perks that some banks offer new customers, such as cashback that can be used to pay legal fees.

It is important to be transparent about your intentions to switch lenders with the home seller and your real estate agent. Additionally, you must get your mortgage preapproved by your new lender before making the switch. This step is relatively quick and is usually completed before the offer is made. Changing lenders can sometimes result in better deals and increased customer satisfaction, but it is important to consider the potential risks and costs involved. For example, switching lenders may cause delays in the overall process, change your closing costs, and require a new appraisal and credit check.

To make an informed decision, be sure to do your research, compare your options, and consider how creditor insurance for your mortgage can protect you financially against death, critical illness, disability, or job loss. You may also want to use a mortgage affordability calculator to determine whether the payments fit your budget. Remember, your mortgage should adapt to your life's changing needs and fit your lifestyle, financial situation, and future goals.

Bank CDs: FDIC Insurance and Level One Accounts

You may want to see also

Explore related products

$8.34 $17.99

![]()

Renewal fees may be waived if you renew early

When it comes to mortgage renewal, it's important to consider your changing needs and financial situation. Renewal is a great opportunity to review and make changes to your mortgage term, type, payment frequency, and other features. You can start investigating your renewal options about five months before your current mortgage expires. This is also a good time to do your research, compare options, and consider how creditor insurance can protect you financially against life's uncertainties.

Renewing your mortgage early can offer several benefits, including potential savings on interest costs if rates rise before your regular renewal date. Additionally, early renewal can provide financial certainty by allowing you to know your future regular payments, helping you budget more effectively. At RBC, you can renew up to 180 days before your term ends without incurring any penalties, and lenders often waive prepayment charges or other fees for early renewals.

It's worth noting that different lenders may have varying policies regarding early renewal. For instance, CIBC allows customers to renew their mortgages as early as 150 days before maturity, and they may waive prepayment charges or other fees depending on the mortgage type and incentives offered. However, it's always a good idea to consult with a representative from your lending institution to discuss the best options for your specific circumstances.

While renewing early can have advantages, it's important to carefully consider all aspects of your mortgage. This includes assessing the posted mortgage rate, amortization period, mortgage type (fixed-rate or variable-rate), and payment frequency. Each of these factors can significantly impact your overall payment plan and financial commitments. Therefore, it's beneficial to use the available tools, such as mortgage payment calculators, to make an informed decision that aligns with your financial goals and budget.

Wells Fargo ATM Access for Advisors

You may want to see also

Explore related products

![]()

Renewal is a good time to review your mortgage needs

Firstly, it is important to understand your current situation to navigate your mortgage renewal options with your needs in mind. For instance, your household income may have increased, allowing you to increase your payment frequency or pay off larger sums. On the other hand, you may have experienced a job loss, taken on more debt or started a family, and are now looking for a manageable payment schedule at a fixed rate.

Secondly, you should consider more than just the posted mortgage rate. If you shorten your amortization period and increase your mortgage payments, you'll pay down your mortgage faster. If you choose a fixed-rate mortgage, the interest rate stays the same but tends to be higher. Variable-rate mortgages, on the other hand, fluctuate with the market, meaning you could pay more or less interest depending on the market. Making more frequent payments will also help you pay less interest and more of the principal.

Thirdly, do your research and compare your options. Consider how creditor insurance for your mortgage can help protect you financially against death, critical illness, disability or job loss. You should also assess your insurance needs and how you will manage your mortgage in the event of any of these occurrences.

Finally, you may qualify for a discounted interest rate that is lower than the rate quoted in your renewal letter. Discuss offers you have received from other financial institutions with your lender and decide whether to switch to another lender.

Free Wire Transfers: Which Banks Offer This Service?

You may want to see also

![]()

You can renew your mortgage online

When it comes to renewing your mortgage, you have the option to do it online. In fact, renewing your mortgage online can be a fast and convenient way to compare terms and find the right interest rate for you.

RBC Royal Bank, for example, offers an online Mortgage Renewal Tool that allows you to explore your options and complete your renewal at your convenience. You can access this tool through your online banking account or mobile app. Similarly, TD Bank offers a digital renewal process that can be completed through its EasyWeb Online Banking platform or mobile app.

When renewing your mortgage online, you will typically need to review and accept the terms and conditions of the renewal agreement. It is important to start the renewal process early, giving yourself time to research and compare different options. This includes considering the posted mortgage rate, amortization period, mortgage type (fixed-rate or variable-rate), and payment frequency.

Additionally, you may have the option to renew your mortgage early, which could help you save on interest costs and gain financial certainty. However, it is always recommended to consult with a representative or advisor from your financial institution to discuss the best options for your specific needs and goals.

Tuscaloosa Food Banks: Where to Find Them

You may want to see also

![]()

You can renew early to lock in current interest rates

When it comes to mortgage renewal, it's essential to consider more than just the posted mortgage rate. There are several factors to keep in mind, such as the interest rate environment, your financial goals, and the potential benefits and drawbacks of early renewal.

Firstly, understanding the interest rate environment is crucial. If interest rates are projected to rise, renewing your mortgage early can be advantageous as it allows you to lock in at the current lower rates. This decision can protect you from higher interest rates when your mortgage term ends. However, if interest rates are expected to drop, locking in a rate early might cause you to miss out on those lower rates in the future.

Secondly, your financial goals and circumstances play a significant role in deciding whether to renew early. Your financial situation, lifestyle, and objectives may have changed since your last mortgage agreement. For instance, if you're planning to start a family or make significant purchases, you might want to consider early renewal to benefit from lower interest rates and potentially reduce your overall financial burden.

Additionally, it's important to be aware of the potential benefits and drawbacks of early renewal. While renewing early can provide the advantage of locking in current interest rates, it may also come with certain costs or penalties for breaking your mortgage term early. These penalties could include extra charges or a higher interest rate on your new locked-in interest rate. Therefore, it's recommended to start exploring your options and shopping around for the best deals approximately four months (120 days) before your mortgage term ends. This way, you can make an informed decision and potentially negotiate a better rate with your lender or switch to a different lender offering more favourable terms.

In conclusion, renewing your mortgage early to lock in current interest rates can be a strategic decision, especially in a rate-increasing environment. However, it's crucial to carefully consider your personal financial situation, research and compare different options, and be mindful of any potential penalties or costs associated with early renewal. By staying informed and proactive, you can make the most suitable choice for your financial needs and goals.

Jos. A. Bank: A Brand Worth Trusting?

You may want to see also

Frequently asked questions

The process of renewing your mortgage involves reviewing your mortgage needs and making any desired changes to your mortgage term, type, payment frequency, or other features. You can renew your mortgage with your current lender or choose to move your mortgage to another lender if their conditions better suit your needs.

You can start investigating your mortgage renewal options about five months before your current term expires. Many lenders will contact you around 180 days before your renewal date to discuss your current mortgage needs. You may be able to renew your mortgage early, locking in the current interest rates and protecting yourself from further rate fluctuations.

When renewing your mortgage, consider more than just the posted mortgage rate. Assess the amortization period, mortgage type (fixed-rate or variable-rate), and payment frequency. Additionally, evaluate your insurance needs and consider how you will manage your mortgage in the event of job loss, critical illness, disability, or death.

Yes, you are not obligated to renew your mortgage with the same lender. You can shop around and compare offerings from different lenders to find the best interest rate and conditions that suit your needs. However, if your mortgage has a collateral charge, switching lenders may incur fees for removing the charge and registering the new one.

The specific steps to renew your mortgage may vary depending on your lender. Generally, you will need to review and select your renewal options, and sign and return the necessary documents before your renewal date. Some lenders offer convenient digital renewal processes through online banking platforms or mobile apps.