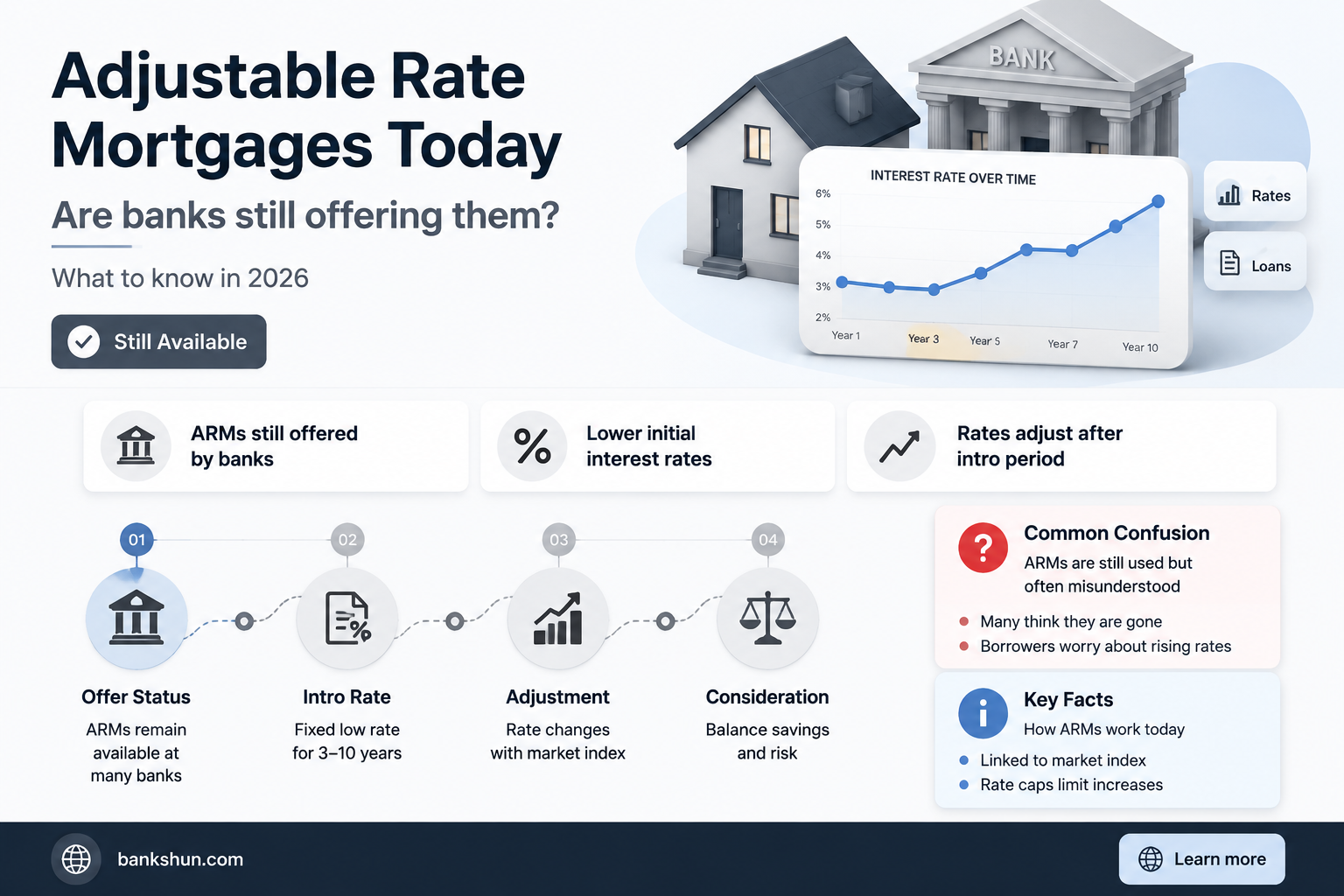

Adjustable-rate mortgages (ARMs) are still issued by banks and lenders, despite their negative reputation from the prior housing crisis. ARMs are a popular choice for borrowers hoping mortgage rates will decrease, as they can offer lower initial rates than fixed-rate mortgages. The interest rate on an ARM is fixed for an introductory period, typically between three to ten years, and then adjusts at regular intervals, usually every six months or year. While ARMs can provide savings for homebuyers, there is a risk that rates may increase significantly after the introductory period, resulting in higher monthly payments.

| Characteristics | Values |

|---|---|

| Availability | Adjustable-rate mortgages (ARMs) are still available from banks. |

| Pricing | ARMs are currently priced lower than fixed-rate mortgages. |

| Risk | ARM rates are influenced by Federal Reserve decisions and market fluctuations. ARM rates may increase after the initial fixed-rate period, potentially making payments unaffordable. |

| Types | Hybrid ARMs are the most common type, with an initial fixed-rate period followed by a floating rate for the remainder of the loan. Examples include 5/1, 5/6, 7/1, 7/6, 10/1, and 10/6 ARMs. |

| Lenders | Top ARM issuers include Chase, Bank of America, First Republic Bank, Wells Fargo, and U.S. Bank. |

| Market Share | In 2021, adjustable-rate mortgages accounted for about 10% of overall loan volume, while 30-year fixed-rate mortgages held a 70% share. |

Explore related products

$9.99

What You'll Learn

- Adjustable-rate mortgages are cheaper than fixed-rate mortgages

- ARM rates are influenced by Federal Reserve decisions

- ARM interest rates and payments may increase after the initial fixed-rate period

- ARM rates are tied to market fluctuations

- ARM loans are usually named by the length of time the interest rate remains fixed

![]()

Adjustable-rate mortgages are cheaper than fixed-rate mortgages

Banks still issue adjustable-rate mortgages (ARMs), which are also known as variable-rate mortgages. These differ from fixed-rate mortgages in that the interest rate may change periodically in accordance with market trends and a corresponding financial index. The initial interest rate on an ARM is usually lower than that of a comparable fixed-rate mortgage. For example, in 2024, the 5/1 ARM was priced at 4% compared to the 30-year fixed rate of 5.125% or higher. This means that a $500,000 loan would result in a monthly payment of $2,387.08 on the ARM.

The interest rate on a fixed-rate mortgage, on the other hand, remains the same throughout the loan's term, making budgeting easier and providing certainty about the monthly payment amount. However, when interest rates are high, qualifying for a fixed-rate mortgage can be more difficult due to higher payments.

The decision between an ARM and a fixed-rate mortgage depends on various factors. ARMs may be attractive if you plan to lower the principal balance early by making extra payments or if you intend to sell the property before the interest rate adjusts. Additionally, in a high-interest-rate market, an ARM can be beneficial due to its initially lower rate. However, it's important to consider the risks associated with ARMs, such as the potential for significant payment increases after the introductory period.

When considering an ARM, it's recommended to compare offers from multiple banks or mortgage companies and to understand the interest rate, fees, and rate cap structure. Tools like adjustable-rate calculators can help estimate how the mortgage payment may change over time.

Locating Bank 2 Sensor 1: Where Is It?

You may want to see also

Explore related products

![]()

ARM rates are influenced by Federal Reserve decisions

Banks still offer adjustable-rate mortgages (ARMs). These mortgages are unique financial products whose interest rates can fluctuate over time, influenced by the state of the economy.

The rates on ARMs are often tied to the Secured Overnight Financing Rate (SOFR) or the Treasury-Index (T-Bill). The Fed's rate decisions serve as a basis for savings instruments, so raising or lowering the federal funds rate can push the SOFR up or down. As a result, ARM rates also move in the same direction when the rate resets. Therefore, if the federal funds rate increases, borrowers can expect their ARM rates to increase at the next adjustment.

While the Fed does not set mortgage rates directly, its decisions influence the percentages lenders offer to prospective homeowners. Even if the Fed maintains its benchmark rate, mortgage rates can fluctuate. For example, in 2022 and 2023, the Fed increased the key interest rate to combat inflation, making it more expensive for Americans to borrow money. However, in late 2024, the Fed cut the rate three times, yet mortgage rates remained relatively high and even increased.

In summary, the Federal Reserve's decisions significantly affect the affordability and appeal of ARMs for borrowers. Prospective and current ARM holders should closely monitor the Fed's actions and stay informed about the economy's potential impact on their mortgages. Understanding these relationships is crucial for borrowers seeking to manage their ARMs effectively and make informed financial decisions.

Who is Friends With Whom? Sasha Banks and Alexa Bliss

You may want to see also

Explore related products

![]()

ARM interest rates and payments may increase after the initial fixed-rate period

Banks still issue adjustable-rate mortgages (ARMs), which are becoming more attractive to prospective buyers as they are currently priced lower than fixed-rate mortgages. However, it is important to understand the risks involved with ARMs.

The frequency of these increases in interest rates will depend on the specific ARM loan. For example, a 5/6 ARM has a fixed interest rate for the first 5 years, after which the interest rate is subject to adjustment once every 6 months. Similarly, a 10/1 ARM has a fixed interest rate for the first 10 years, after which the interest rate is adjusted annually.

It is important to note that not all ARMs will result in an increase in payments. When the index of interest rates declines, the payments on an ARM may decrease. However, this is not true for all ARMs, as some may set a cap on how much the interest rate can decrease over the life of the loan.

To manage the risk of increasing interest rates and payments, some ARMs have an interest rate cap structure. This provides protection from large interest rate swings by limiting the amount of interest rate change allowed during the adjustment period and the life of the loan. For example, a 1-year ARM may have an annual cap of a one percentage point increase and a life-of-loan cap of a five percentage point increase.

Routing Numbers: A US Banking System Exclusive?

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UY218_.jpg)

![]()

ARM rates are tied to market fluctuations

Banks still issue adjustable-rate mortgages (ARMs), which are becoming more popular due to the recent surge in fixed-rate mortgage prices. ARMs are typically priced lower than fixed-rate mortgages, making them an attractive option for prospective home buyers.

ARM rates are influenced by market fluctuations and are tied to an index rate that changes with the market. This means that if market conditions lead to a rate increase, ARM rates will also increase, resulting in higher monthly mortgage payments. Conversely, if market conditions cause interest rates to fall, ARM rates will decrease, leading to lower monthly payments. This fluctuation can make it challenging for borrowers to predict their payments accurately.

The index rate for ARMs is typically the Secured Overnight Financing Rate (SOFR), published daily by the New York Fed. This rate is used as a basis for ARM interest rate adjustments by lenders such as Bank of America. The London Interbank Offered Rate (LIBOR) was previously used as the index but was replaced by SOFR in October 2020 to increase long-term liquidity.

ARM rates are also influenced by Federal Reserve decisions. While the Fed has not changed its benchmark rate in 2025, it may consider cutting rates later in the year, which could impact ARM rates.

It's important to note that ARM rates are subject to adjustment after an initial fixed-rate period, which typically lasts between 3, 5, 7, or 10 years. During this initial period, the interest rate remains fixed, providing borrowers with some predictability. However, once the fixed-rate period ends, the ARM rate will fluctuate based on market conditions and the chosen index rate.

The Federal Reserve: Private Bank or Government Entity?

You may want to see also

![]()

ARM loans are usually named by the length of time the interest rate remains fixed

Banks still offer adjustable-rate mortgages (ARMs). However, they are considered riskier than fixed-rate mortgages because the interest rates can increase or decrease based on broader market trends. The interest rate on an ARM is determined by a fluctuating benchmark rate that usually reflects the general state of the economy.

Hybrid ARMs offer a mix of fixed and adjustable rates. During the fixed-rate period, the interest rate remains constant, providing stability and predictable payments. Once this period ends, the interest rate adjusts at predetermined intervals, such as every year or every six months. This information is crucial for borrowers to understand, as it directly impacts their monthly payments and overall affordability.

It is important to carefully consider the terms of an ARM before committing to one. While ARMs may offer lower initial interest rates and monthly payments than fixed-rate mortgages, there is a risk of substantial increases in the future. Borrowers should be aware of potential rate adjustments and their impact on financial planning. Consulting with a professional financial advisor can help individuals make informed decisions about mortgage options based on their specific circumstances.

Cash Out Refinance: Which Banks Offer This?

You may want to see also

Frequently asked questions

Yes, banks still issue adjustable-rate mortgages (ARMs).

Adjustable-rate mortgages can be cheaper than fixed-rate mortgages, especially during the introductory period. This can allow you to save money on your mortgage for the first few years.

Adjustable-rate mortgages have a fixed rate for a set number of years, typically between five and ten years. After that, the rate resets at regular intervals, usually once a year or every six months.

The biggest risk of an adjustable-rate mortgage is that the interest rate could increase after the initial fixed-rate period, pushing up your monthly mortgage payment.

You can get an adjustable-rate mortgage by applying to a bank or mortgage company. You will need to consider factors such as your credit score, down payment, and income when applying for an adjustable-rate mortgage.