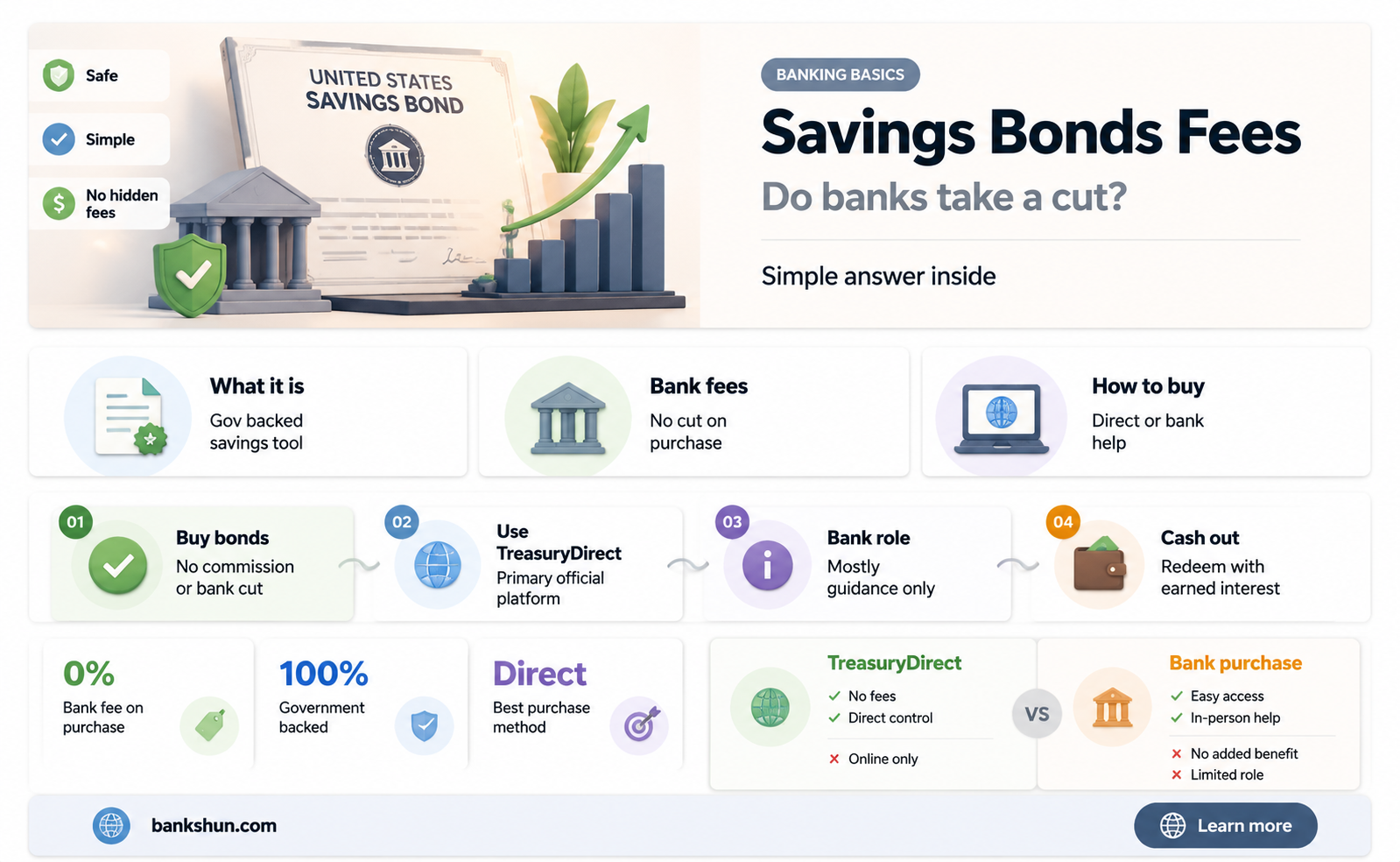

Savings bonds are a low-risk investment option, but do banks take a commission on them? This is an important question to ask when considering investing in savings bonds, as any fees could impact the overall return on investment.

| Characteristics | Values | |||

|---|---|---|---|---|

| Savings bonds are a | low-risk way to save money | |||

| U.S. savings bonds are | government-backed | |||

| Denominations range from | $25 to $10,000 | |||

| Bonds issued after April 2005 have a | fixed interest rate | |||

| Older bonds (1997-2005) have a | variable interest rate | |||

| Anyone who’s 18 or older with a valid Social Security number, U.S. bank account, and U.S. address | can purchase savings bonds | |||

| Savings bonds can be cashed in after | 1 year | |||

| There is a | penalty for cashing savings bonds within the first five years | |||

| Savings bonds can be kept until they fully mature, which is generally | 30 years | |||

| Only | electronic bonds | can be purchased these days, but | paper bonds | can still be cashed in |

| Types of bonds include | Series E/EE, Series I, or Series H/HH | |||

| Series E/EE bonds earn a | fixed rate of interest for up to 30 years | |||

| Series I bonds earn interest based on | combining a fixed rate and an inflation rate | |||

| Redemption tables allow you to find the values and interest earned for | Series EE savings bonds, Series E savings bonds, Series I savings bonds, and Savings Notes issued as far back as 1941 | |||

| The U.S. Department of the Treasury | no longer issues HH and other historical bond series | |||

| To buy, redeem, or manage electronic savings bonds, you will need to | create or log into your TreasuryDirect account | |||

| Paper bonds can only be purchased as part of your | IRS tax refund |

Explore related products

What You'll Learn

![]()

U.S. savings bonds are a low-risk investment

Savings bonds are also a low-risk investment due to their fixed or variable interest rates. Bonds issued after April 2005 have a fixed interest rate, while older bonds from 1997 to 2005 have a variable interest rate. The interest rate on Series I bonds, for example, changes every six months based on inflation, providing protection against inflation and preserving the value of the invested money. This feature is particularly attractive during periods of expected high inflation, as seen in the spring of 2021 when inflation began to rise in the United States.

The low-risk nature of U.S. savings bonds is further highlighted by their long-term maturity periods. Most savings bonds can be cashed in after one year, but they can earn interest for up to 30 years for Series EE and Series I bonds. However, cashing in the bonds before five years results in a penalty, typically the loss of the last three months of interest. Additionally, some bonds have a 20-year life, such as the HH bonds that reached final maturity in August 2024.

U.S. savings bonds are available in denominations ranging from $25 to $10,000, making them accessible to a wide range of investors. Anyone 18 or older with a valid Social Security number, U.S. bank account, and U.S. address can purchase these bonds. The process of cashing in savings bonds is straightforward and can be done through banks or directly with the U.S. Department of the Treasury. Overall, U.S. savings bonds offer a secure and stable investment option, particularly appealing during times of economic uncertainty or high inflation.

Crafting a Compelling Resume: Adding a Minor for Banking Roles

You may want to see also

Explore related products

![]()

You can cash in after one year

Savings bonds are a great, low-risk way to save money. They are backed by the US government, which means that they are reliable and secure. When you buy a US savings bond, you are lending money to the government, which it will pay back with interest.

There are several types of savings bonds, including Series E/EE, Series I, and Series H/HH. The US Department of the Treasury currently sells two types of savings bonds: the EE and I series. The EE bond earns a fixed rate of interest for up to 30 years, while the I bond earns interest based on a combination of a fixed rate and an inflation rate.

You can cash in your savings bonds after owning them for at least one year. However, it is important to note that if you cash in your bonds before five years, you will lose the last three months of interest. The longer you hold onto your savings bonds, the more they will earn you. So, while you have the option to cash in after one year, it may be beneficial to wait, especially if you want to avoid the penalty for early cash-in.

To cash in your savings bonds, you will need to provide proof of identity and partner with a notary to certify your signature on an unsigned FS Form 1522. After completing these steps, you can send the required documents to the US Department of the Treasury. If you are cashing in an electronic savings bond, you can log in to your TreasuryDirect account and use the link for cashing securities in ManageDirect.

Oxygen Sensor Location: Bank 2 Sensor Positioning Explained

You may want to see also

Explore related products

![]()

There is a penalty for cashing in within the first five years

Savings bonds are a great, low-risk way to save money. They are government-backed investments available in denominations ranging from $25 to $10,000. Bonds issued after April 2005 have a fixed interest rate, while older bonds (1997-2005) have a variable interest rate.

Anyone who is 18 or older with a valid Social Security number, US bank account, and US address can purchase savings bonds. They can be cashed in after a year, but there is a penalty for cashing them within the first five years. If you cash in the bond in less than five years, you will lose the last three months' worth of interest. For example, if you redeem a bond after 24 months, you will only receive 21 months of interest.

To avoid this penalty, it is generally beneficial to wait until the bond is fully mature, which is usually 30 years. However, if you are cashing in an electronic savings bond, you can log in to your TreasuryDirect account and use the link for cashing securities in ManageDirect. The cash will generally transfer to your checking or savings account within two business days of the request.

For Series H or HH paper bonds, you will need to mail the unsigned bonds to the US Treasury at the following address: Treasury Retail Securities Services, PO Box 2186 Minneapolis, MN 55480-0214. When cashing in a paper bond, they must be cashed in full.

Transfer Apple Cash to Your Bank Account

You may want to see also

Explore related products

![]()

Paper bonds can be purchased as part of an IRS tax refund

The U.S. Department of the Treasury currently sells two types of savings bonds: the EE and I series. Both series have different interest rates, which are either fixed or change with inflation. Paper bonds can be purchased as part of an IRS tax refund.

The Tax Time Savings Bonds (TTSB) program was established in 2010 to give tax filers, especially those with low and moderate incomes, the ability to buy paper Series I savings bonds using their tax refunds. Series I bonds are available in denominations ranging from $25 to $10,000. They can be purchased as gifts and are registered in the name of the recipient.

Series I bonds can be held indefinitely, but they only earn interest for up to 30 years. If you cash in the bond in less than five years, you will lose the last three months of interest. To cash in a paper bond, you must do so in full. You will need to provide proof of identity, such as a U.S. driver's license, and partner with a notary to notarize and certify your signature on an unsigned FS Form 1522.

You can determine the value of a paper bond using the savings bond calculator. The calculator provides redemption values for Series EE and I savings bonds issued as far back as 1941. For redemption values after May 2023, use the Savings Bond Calculator on the TreasuryDirect website.

Tap and Go: Are Banks Charging You for This?

You may want to see also

Explore related products

![]()

You can buy electronic bonds online

You can buy electronic savings bonds online through the US Department of the Treasury's official website, TreasuryDirect. Electronic bonds are available in the form of Series EE and Series I bonds. Series EE bonds have a fixed interest rate, while Series I bonds have a variable interest rate that changes with inflation. You can buy electronic savings bonds for yourself, your child, or as a gift for someone else.

To purchase electronic bonds online, you must have a TreasuryDirect account. Once you have an account, you can log in and choose the "BuyDirect" option. You will then be able to select whether you want to purchase EE or I bonds and fill out the necessary information. The value of the electronic savings bond can be determined by logging into your TreasuryDirect account.

It is important to note that there are specific conditions and restrictions when purchasing electronic savings bonds. For example, in a calendar year, you may buy up to $10,000 in Series EE electronic savings bonds and up to $10,000 in Series I electronic savings bonds for yourself. If you are buying savings bonds for a child, their TreasuryDirect account must be linked to your account or that of another adult custodian.

Additionally, electronic savings bonds can only be purchased in denominations ranging from $25 to $10,000. You can specify the owner of the bond, whether it is yourself, a child, or someone else as a beneficiary or gift recipient. It is also worth noting that the option to purchase electronic savings bonds will be discontinued after January 31, 2025.

Best Banks with No Overdraft Fees: Avoid Those Charges!

You may want to see also