The United States is home to a vast and complex banking system, with numerous financial institutions spread across the country. When discussing banking districts, it's essential to understand that the U.S. does not have a uniform definition or official designation for these areas. However, the concept generally refers to regions with a high concentration of banks, financial institutions, and related businesses, often serving as hubs for economic activity. The number of banking districts in the U.S. is not fixed, as it depends on various factors, including population density, economic development, and historical significance. Major cities like New York, Chicago, and San Francisco are renowned for their prominent financial districts, but many other urban centers also boast significant banking clusters, contributing to the nation's diverse and extensive financial landscape.

Explore related products

What You'll Learn

- Federal Reserve Districts: 12 districts, each with a Federal Reserve Bank, covering specific regions

- Major Banking Hubs: New York, San Francisco, Chicago, and others as key financial centers

- State Banking Regulations: Variations in state-level banking laws and district definitions

- Bank Concentration Areas: Regions with high numbers of banks, like the Northeast and Midwest

- Historical District Changes: Evolution of banking districts since the Federal Reserve Act of 1913

![]()

Federal Reserve Districts: 12 districts, each with a Federal Reserve Bank, covering specific regions

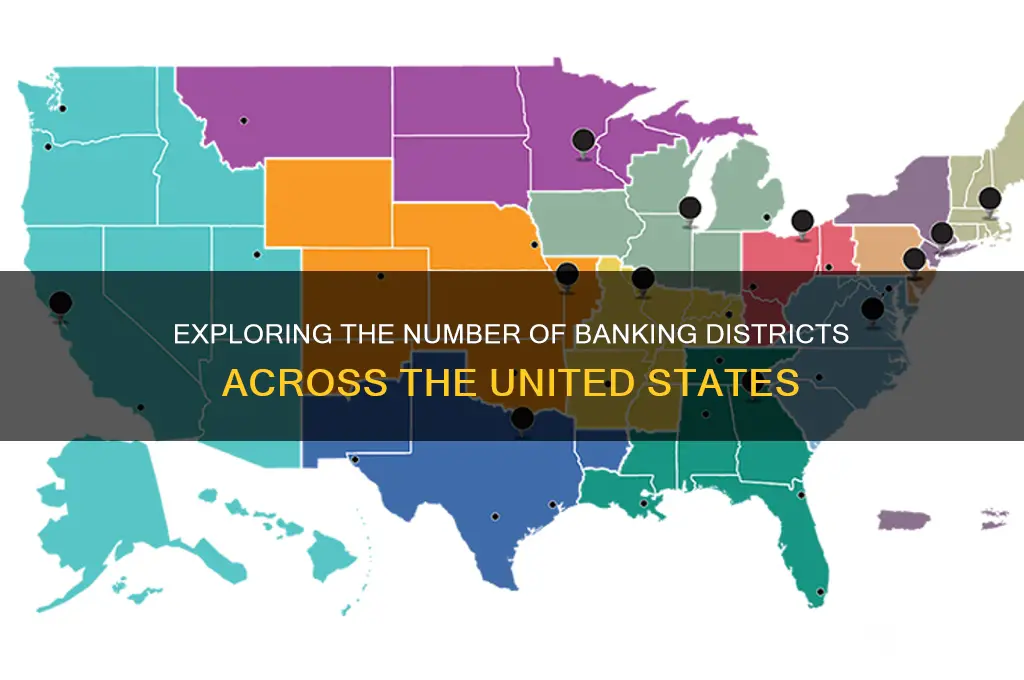

The United States is divided into 12 Federal Reserve Districts, each served by its own Federal Reserve Bank. These districts were established under the Federal Reserve Act of 1913 to ensure a decentralized yet coordinated banking system. Each district covers a specific geographic region, with the Federal Reserve Bank acting as the central banking authority for its area. This structure allows the Federal Reserve System to address regional economic conditions while maintaining a unified national monetary policy. The 12 districts are designed to reflect the economic diversity and needs of different parts of the country, ensuring that local perspectives are considered in policymaking.

The Federal Reserve Bank of New York (District 2) is often considered the most influential due to its role in implementing monetary policy and its proximity to Wall Street. It covers New York State, Northern New Jersey, Fairfield County in Connecticut, Puerto Rico, and the U.S. Virgin Islands. In contrast, the Federal Reserve Bank of San Francisco (District 12) serves the westernmost states, including California, Oregon, Washington, Alaska, and Hawaii, as well as American Samoa and Guam. Each district's boundaries were drawn based on economic ties, population, and geographic considerations at the time of the Federal Reserve's creation.

The Federal Reserve Bank of Chicago (District 7) is another key institution, covering the Midwest, including Illinois, Indiana, Iowa, Michigan, and Wisconsin. Similarly, the Federal Reserve Bank of Dallas (District 11) serves the southern states of Texas, northern Louisiana, and southern New Mexico. Each Federal Reserve Bank operates independently but collaborates with the Federal Reserve Board in Washington, D.C., to oversee the nation's banking system, manage monetary policy, and ensure financial stability.

Smaller districts, such as the Federal Reserve Bank of Minneapolis (District 9), cover less populous regions like Minnesota, Montana, North and South Dakota, and parts of Michigan and Wisconsin. Despite their size, these districts play a critical role in monitoring local economic conditions and providing financial services to member banks. The Federal Reserve Bank of Boston (District 1), the first district established, serves New England, including Massachusetts, Maine, New Hampshire, Rhode Island, and Vermont.

The remaining districts—Philadelphia (District 3), Cleveland (District 4), Richmond (District 5), Atlanta (District 6), St. Louis (District 8), and Kansas City (District 10)—each have their unique regional focus. For example, the Federal Reserve Bank of Atlanta covers the Southeast, including Alabama, Florida, Georgia, and parts of Louisiana, Mississippi, and Tennessee. This regional structure ensures that the Federal Reserve System remains responsive to the varied economic landscapes across the United States.

In summary, the 12 Federal Reserve Districts form the backbone of the U.S. banking system, with each district's Federal Reserve Bank playing a vital role in monetary policy, bank supervision, and financial services. This decentralized yet interconnected system allows the Federal Reserve to balance national economic goals with regional economic realities, making it a cornerstone of American financial stability.

Understanding the Banker's Offer Calculation in Deal or No Deal

You may want to see also

Explore related products

![]()

Major Banking Hubs: New York, San Francisco, Chicago, and others as key financial centers

The United States is home to numerous banking districts, but a few cities stand out as major banking hubs that dominate the financial landscape. Among these, New York City is undoubtedly the most prominent. As the financial capital of the world, New York houses Wall Street, the epicenter of global finance. It is home to the New York Stock Exchange (NYSE), NASDAQ, and the Federal Reserve Bank of New York, making it a critical hub for investment banking, asset management, and international finance. The city's banking district is not limited to Manhattan; it extends its influence globally, attracting major banks like JPMorgan Chase, Goldman Sachs, and Citigroup, which have significant operations here.

San Francisco is another key banking hub, particularly for technology-driven finance and venture capital. As the gateway to Silicon Valley, San Francisco has become a center for fintech innovation and startup funding. Major banks like Wells Fargo have their headquarters here, and the city is also a hub for wealth management and private banking. The San Francisco Federal Reserve Bank further solidifies its role in the national financial system. Its proximity to tech giants and emerging startups makes it a unique banking district, blending traditional finance with cutting-edge technology.

Chicago is the third major banking hub, serving as the financial center of the Midwest. It is home to the Chicago Board of Trade and the Chicago Mercantile Exchange, making it a global leader in derivatives and commodities trading. Major banks like Bank of America and BMO Harris Bank have significant operations in Chicago. The city's strategic location and robust infrastructure make it a vital hub for commercial banking, risk management, and financial services. The Federal Reserve Bank of Chicago also plays a crucial role in monetary policy and economic stability for the region.

Beyond these three, other cities like Charlotte, North Carolina, and Houston, Texas, have emerged as significant banking hubs. Charlotte is often referred to as the "Wall Street of the South," with Bank of America and Truist Financial headquartered there. Its banking district is a major player in retail banking and corporate finance. Houston, on the other hand, is a key financial center for energy finance, given its proximity to the oil and gas industry. Major banks like JPMorgan Chase and Wells Fargo have substantial operations in Houston, catering to the unique financial needs of the energy sector.

While these cities represent the major banking hubs, the U.S. financial system is decentralized, with smaller banking districts in cities like Boston, Philadelphia, and Los Angeles also playing important roles. Boston, for instance, is a hub for asset management and fintech, while Philadelphia is known for its focus on consumer banking and financial technology. Los Angeles, with its strong ties to entertainment and real estate, offers specialized financial services in these sectors. Together, these banking districts form a diverse and interconnected financial network that underpins the U.S. economy.

In summary, while the exact number of banking districts in the U.S. is not fixed, the major hubs of New York, San Francisco, Chicago, Charlotte, and Houston are undeniably the most influential. Each of these cities brings unique strengths to the table, whether it's global finance, tech-driven innovation, commodities trading, or specialized industry financing. Understanding these hubs is essential for grasping the complexity and dynamism of the U.S. financial system.

How Banks Verify Employment for Mortgage Approval: A Comprehensive Guide

You may want to see also

Explore related products

![]()

State Banking Regulations: Variations in state-level banking laws and district definitions

The United States does not have a uniform definition of "banking districts," as the concept is not standardized across the country. Instead, banking regulations and oversight are primarily governed by a combination of federal and state laws, with significant variations at the state level. Each state has its own banking code and regulatory framework, which can lead to diverse interpretations and definitions of banking regions or districts. This state-by-state approach results in a complex patchwork of regulations that financial institutions must navigate.

State banking regulations often dictate the structure and operation of banks within their jurisdiction, including chartering requirements, licensing, and supervision. For instance, some states may define specific geographic areas as banking districts for regulatory purposes, while others might not use this terminology at all. In states like New York, the banking department oversees a network of branches and offices, but the focus is on the institution rather than a district-based model. California, on the other hand, has a more decentralized approach, with regional offices of the Department of Financial Protection and Innovation overseeing banks, but again, the emphasis is on the regulatory body's reach rather than defined districts.

The variation in state laws becomes more apparent when examining the powers granted to state banking regulators. Some states allow their banking departments to conduct on-site examinations and enforce compliance, while others have more limited authority. For example, Texas has a robust state banking system with its own regulatory body, the Texas Department of Banking, which supervises state-chartered banks and savings institutions, but it does not explicitly define banking districts. In contrast, smaller states might have fewer resources and rely more heavily on federal regulations, adopting a more uniform approach without distinct district definitions.

The number of banking districts, if defined, could vary widely depending on the state's size, population, and economic landscape. A densely populated state with multiple urban centers might establish several districts to manage oversight effectively. Conversely, a rural state with a smaller banking sector may not require such a structured district system. This flexibility in state-level regulations allows for a more tailored approach to banking supervision but also presents challenges for banks operating across multiple states, as they must adhere to different rules and definitions.

Understanding these state-level variations is crucial for banks and financial institutions operating in multiple jurisdictions. Compliance with local regulations is essential to avoid legal and operational issues. While the federal government provides a baseline of banking regulations, the state-by-state differences in laws and district definitions, if any, create a unique regulatory environment that requires careful consideration and adaptation by banking entities. This complexity underscores the importance of localized knowledge in the highly regulated banking industry.

HIV Donors and Blood Banks: Safety Protocols and Donor Management

You may want to see also

Explore related products

![District 9 [4K Ultra HD + Blu-ray + Digital] [4K UHD]](https://m.media-amazon.com/images/I/71tvNKfItiL._AC_UY218_.jpg)

![]()

Bank Concentration Areas: Regions with high numbers of banks, like the Northeast and Midwest

The United States is home to a vast and complex banking system, with thousands of banks spread across the country. When examining bank concentration areas, two regions stand out for their high numbers of banks: the Northeast and the Midwest. These regions have historically been hubs for financial activity, with major cities like New York, Boston, Chicago, and Philadelphia serving as centers for banking and finance. According to various sources, including the Federal Deposit Insurance Corporation (FDIC), these regions have a disproportionately high number of banks compared to other parts of the country. The Northeast, in particular, is often cited as having the highest concentration of banks, with states like New York, Pennsylvania, and Massachusetts leading the way.

The Midwest, while not as densely populated as the Northeast, also boasts a significant number of banks, particularly in states like Illinois, Ohio, and Michigan. Cities like Chicago and Detroit have long been centers for banking and finance, with a strong presence of both large national banks and smaller regional institutions. The concentration of banks in these areas can be attributed to a variety of factors, including historical patterns of settlement and economic development, as well as the presence of major financial markets and institutions. For example, the New York Stock Exchange and the Federal Reserve Bank of New York are both located in the Northeast, while the Chicago Board of Trade and the Federal Reserve Bank of Chicago are located in the Midwest. These institutions have helped to establish these regions as major hubs for financial activity, attracting banks and other financial institutions to the area.

In terms of the number of banking districts in the US, it's difficult to provide a precise figure, as the definition of a "banking district" can vary. However, according to the FDIC, there are over 5,000 FDIC-insured banks and savings institutions in the United States, spread across approximately 2,000 counties. While not all of these counties can be considered distinct banking districts, it's clear that the US banking system is highly decentralized, with a large number of institutions operating in different regions and markets. That being said, the Northeast and Midwest regions are notable for their high concentrations of banks, with some estimates suggesting that these regions are home to over 30% of all US banks. This concentration of banks has important implications for the economy, as it can affect the availability of credit, the cost of financial services, and the overall stability of the financial system.

The high concentration of banks in the Northeast and Midwest has also led to the development of specialized financial services and products in these regions. For example, the Northeast is known for its strength in investment banking, asset management, and securities trading, while the Midwest has a strong presence in commercial banking, agricultural lending, and community banking. This specialization has helped to establish these regions as leaders in different areas of finance, attracting businesses, investors, and financial professionals to the area. Furthermore, the presence of multiple banks in close proximity can also lead to increased competition, which can drive innovation, improve efficiency, and ultimately benefit consumers through lower prices and better services. However, it's also important to note that bank concentration can also pose risks, such as increased systemic risk and reduced financial stability, particularly in the event of a financial crisis or economic downturn.

In recent years, there has been a trend towards consolidation in the US banking industry, with larger banks acquiring smaller institutions and expanding their presence in different regions. This has led to some concerns about the potential for reduced competition and increased market power among the largest banks. However, despite these trends, the Northeast and Midwest regions remain important hubs for banking and finance, with a diverse range of institutions operating in these areas. As the US banking system continues to evolve, it will be interesting to see how these regions adapt and respond to changing market conditions, technological advancements, and shifts in consumer behavior. By understanding the dynamics of bank concentration areas, policymakers, regulators, and industry professionals can work together to promote a healthy, competitive, and stable banking system that meets the needs of consumers and supports economic growth and development.

In conclusion, the Northeast and Midwest regions of the United States are notable for their high concentrations of banks, with a large number of institutions operating in these areas. While the exact number of banking districts in the US is difficult to determine, it's clear that these regions play a critical role in the country's financial system. As hubs for banking and finance, the Northeast and Midwest have developed specialized expertise, attracted businesses and investors, and contributed to the overall growth and development of the US economy. By examining the factors that contribute to bank concentration in these regions, we can gain a better understanding of the dynamics of the US banking system and work towards promoting a more competitive, stable, and resilient financial sector. Ultimately, the health and stability of the US banking system will depend on a range of factors, including the distribution of banks across different regions, the level of competition among institutions, and the ability of regulators and policymakers to effectively oversee and manage the system.

Faze Banks and Alissa Violet: The Story of Their First Encounter

You may want to see also

Explore related products

![]()

Historical District Changes: Evolution of banking districts since the Federal Reserve Act of 1913

The Federal Reserve Act of 1913 established the Federal Reserve System, dividing the United States into 12 Federal Reserve Districts, each with its own Federal Reserve Bank. These districts were designed to decentralize banking operations and better serve the diverse economic needs of the nation. The original districts included Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco. Each district was delineated based on geographic, economic, and population considerations, ensuring that the Federal Reserve could effectively monitor and influence regional banking activities. This structure marked the beginning of a formalized banking district system in the U.S., replacing the previously fragmented and often unstable banking landscape.

In the decades following the establishment of the Federal Reserve, banking districts evolved in response to economic growth, urbanization, and technological advancements. The mid-20th century saw significant changes as the U.S. economy expanded rapidly, particularly after World War II. While the number of Federal Reserve Districts remained unchanged, the role and influence of these districts shifted. For example, the New York Federal Reserve District solidified its position as the financial epicenter of the nation, overseeing Wall Street and the global financial markets. Meanwhile, districts like Chicago and San Francisco grew in importance as their respective regions became hubs for industry, technology, and innovation. These changes reflected the dynamic nature of the U.S. economy and the adaptability of the Federal Reserve System.

The late 20th century brought further transformations to banking districts, driven by deregulation, globalization, and the rise of digital banking. The 1980s and 1990s saw the consolidation of banks and the emergence of megabanks, which operated across multiple districts. This trend challenged the traditional boundaries of banking districts, as financial institutions increasingly conducted business on a national and international scale. Despite these shifts, the Federal Reserve Districts retained their relevance, serving as critical nodes for monetary policy implementation and economic oversight. The Federal Reserve Act of 1913 had established a resilient framework that could accommodate these changes while maintaining regional focus.

In recent years, the evolution of banking districts has been shaped by technological innovation and the growing importance of fintech. While the 12 Federal Reserve Districts remain intact, their functions have expanded to include oversight of digital payment systems, cybersecurity, and the integration of new financial technologies. Districts like San Francisco and New York have become central to regulating and supporting fintech innovation, reflecting their regions' leadership in the tech sector. Meanwhile, other districts have adapted to address the unique economic challenges of their areas, such as agricultural financing in the Midwest or energy sector banking in the South. This adaptability underscores the enduring significance of the Federal Reserve Districts in a rapidly changing financial landscape.

Throughout their history, the Federal Reserve Districts have played a pivotal role in shaping the U.S. banking system, from stabilizing the economy during the Great Depression to navigating the complexities of the modern financial era. The number of districts has remained constant since 1913, but their functions and influence have evolved dramatically. This evolution highlights the foresight of the Federal Reserve Act, which created a flexible and decentralized system capable of responding to the nation's changing economic needs. As the U.S. banking sector continues to transform, the Federal Reserve Districts will undoubtedly remain essential to its stability and growth.

Does Bank Balance Count as Annual Income? Understanding Financial Definitions

You may want to see also

Frequently asked questions

There are 12 Federal Reserve Districts in the United States, each with its own Federal Reserve Bank.

The 12 Federal Reserve Districts are Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco.

While Federal Reserve Districts are the primary banking districts, the term can also refer to state-designated banking regions or areas with high concentrations of financial institutions, but these vary by state and are not standardized nationally.

![District B13/District 13: Ultimatum 2-Pack [Blu-ray]](https://m.media-amazon.com/images/I/51NbshdYOvL._AC_UY218_.jpg)

![Chappie / District 9 / Elysium - Set [Blu-ray]](https://m.media-amazon.com/images/I/91UAVlk4E3L._AC_UY218_.jpg)