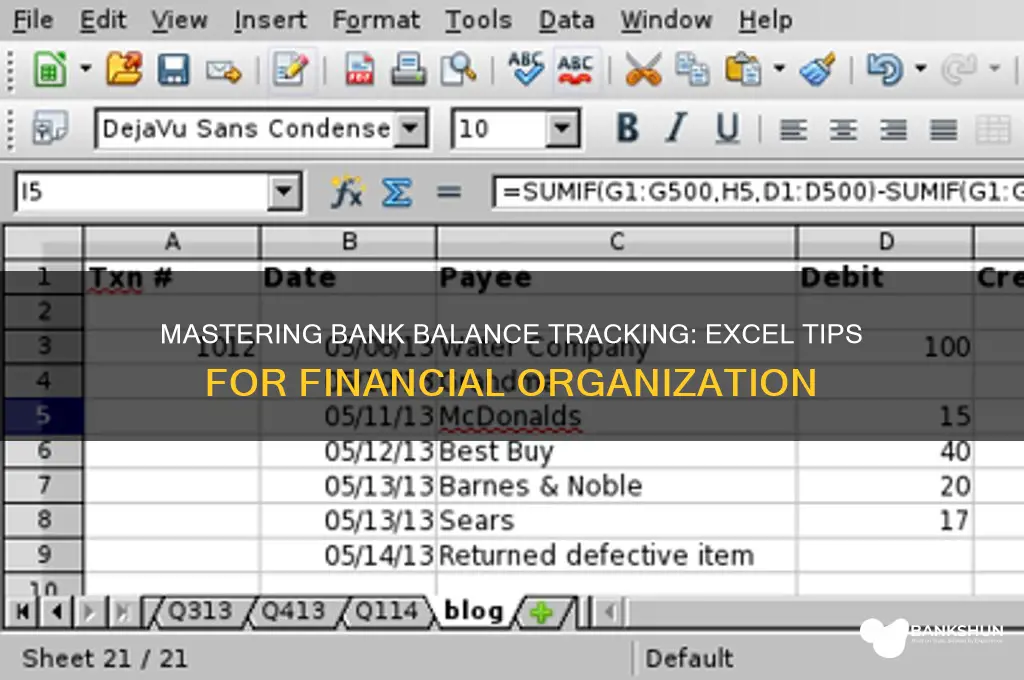

Maintaining your bank balance in Excel is an efficient way to track income, expenses, and overall financial health. By creating a structured spreadsheet, you can record transactions, categorize spending, and monitor account balances in real-time. Excel’s formulas, such as SUM, AVERAGE, and conditional formatting, simplify calculations and highlight trends, while regular updates ensure accuracy. This method not only helps you stay organized but also provides insights into budgeting, saving, and identifying areas for financial improvement. Whether for personal or business use, mastering this skill empowers you to take control of your finances with clarity and precision.

| Characteristics | Values |

|---|---|

| Track Transactions Regularly | Record all income and expenses as they occur. |

| Use Consistent Categories | Create categories (e.g., groceries, rent, salary) for better organization. |

| Reconcile Monthly | Compare your Excel sheet with bank statements to ensure accuracy. |

| Formula for Balance Calculation | Use =SUM(Income) - SUM(Expenses) to calculate the current balance. |

| Conditional Formatting | Highlight negative balances or low funds for quick identification. |

| Date Formatting | Use consistent date formats (e.g., MM/DD/YYYY) for sorting and filtering. |

| Automate Entries | Use templates or macros for recurring transactions. |

| Backup Data | Save Excel files regularly and keep backups in cloud storage. |

| Use Separate Sheets | Dedicate sheets for monthly/annual summaries and detailed transactions. |

| Error Checking | Use Excel’s error-checking tools to identify discrepancies. |

| Visualize Data | Create charts (e.g., pie charts, line graphs) to analyze spending patterns. |

| Password Protection | Secure sensitive financial data with passwords. |

| Mobile Accessibility | Use Excel mobile apps or cloud syncing for on-the-go updates. |

| Regular Updates | Update the sheet daily or weekly to maintain accuracy. |

| Notes/Comments | Add notes for unusual transactions or reminders. |

Explore related products

What You'll Learn

- Track Income & Expenses: Log all transactions with dates, categories, and amounts for clear financial tracking

- Use Formulas: Apply SUM, AVERAGE, and IF functions to automate calculations and balance updates

- Create Charts: Visualize spending trends with pie charts or bar graphs for better insights

- Set Budgets: Allocate funds to categories and monitor progress against predefined spending limits

- Reconcile Statements: Compare Excel records with bank statements to identify discrepancies and errors

![]()

Track Income & Expenses: Log all transactions with dates, categories, and amounts for clear financial tracking

Maintaining a clear financial record begins with meticulous logging of every transaction. Each entry should include the date, category, and amount to create a transparent snapshot of your financial activity. For instance, if you spend $45 on groceries on March 15, log it as "03/15/2023, Groceries, -$45." This structured approach eliminates ambiguity and ensures every dollar is accounted for, whether it’s income from a freelance gig or a small expense like a coffee.

The power of categorization cannot be overstated. Assigning each transaction to a specific category—such as "Utilities," "Entertainment," or "Savings"—transforms raw data into actionable insights. Excel’s filtering tools allow you to quickly analyze spending patterns. For example, summing all entries under "Dining Out" for the month might reveal an area for budget cuts. Without categories, your data remains a jumbled list, lacking the clarity needed for informed decision-making.

Dates serve as the backbone of your financial timeline, enabling trend analysis and deadline tracking. For recurring expenses like rent or subscriptions, consistent date logging highlights payment cycles and prevents late fees. Pairing dates with Excel’s sorting function lets you view transactions chronologically or group them by month, making it easier to reconcile with bank statements. A missing date turns a precise record into a guessing game, undermining the entire system.

While logging transactions is straightforward, consistency is the linchpin of success. Dedicate 10–15 minutes daily or weekly to update your spreadsheet, ensuring no transaction slips through the cracks. Use Excel’s autocomplete feature for recurring entries to save time. For those who struggle with manual input, consider linking your bank account to Excel via third-party tools for automated imports, though this requires occasional verification to correct errors. Neglecting regular updates turns a dynamic tool into a static, outdated document.

Finally, the true value of this system lies in its ability to drive financial decisions. A well-maintained log becomes the foundation for budgeting, saving, and planning. For example, identifying that 20% of your income goes to "Transportation" might prompt exploring cheaper alternatives. Over time, this data can also highlight long-term trends, such as increasing utility costs, allowing you to adjust before they become unmanageable. Without this granular tracking, financial goals remain abstract, unsupported by concrete data.

Understanding Bank Bundles: How Many Hundreds Are in a Standard Stack?

You may want to see also

Explore related products

![]()

Use Formulas: Apply SUM, AVERAGE, and IF functions to automate calculations and balance updates

Excel's formulas are the backbone of efficient bank balance management, transforming static data into dynamic, self-updating records. The SUM function is your starting point. Instead of manually adding transactions, use `=SUM(A2:A100)` to instantly calculate the total inflows or outflows in a specified range. This not only saves time but eliminates human error, ensuring accuracy in your balance tracking. Pair this with absolute references (`$A$2:$A$100`) to maintain the range when copying formulas across rows or sheets, a small tweak with significant efficiency gains.

While SUM handles totals, AVERAGE provides context by revealing spending or earning trends. Apply `=AVERAGE(B2:B100)` to gauge monthly expenses or income, helping you identify anomalies or areas for adjustment. For instance, if your average monthly expenditure spikes, this formula flags the issue before it impacts your overall balance. Combining SUM and AVERAGE in adjacent columns creates a comprehensive snapshot of your financial health, all without manual intervention.

The IF function introduces conditional logic, automating balance updates based on transaction types. Use `=IF(C2="Deposit", D2, -D2)` to add deposits directly and subtract withdrawals, ensuring your running balance (`=E1+F2`) reflects real-time changes. This setup dynamically adjusts as new transactions are added, making it ideal for daily or weekly updates. For added precision, nest IF with AND or OR to categorize transactions (e.g., `=IF(AND(C2="Withdrawal", D2>500), -D2, 0)`) and filter out irrelevant entries.

However, reliance on formulas demands vigilance. Always validate ranges to avoid errors—a misplaced cell reference can skew results. Use Excel’s trace precedents tool to audit formula dependencies, and format cells conditionally to highlight discrepancies (e.g., red for negative balances). Regularly reconcile formula-driven balances with bank statements to catch discrepancies early. While automation streamlines tracking, it’s no substitute for periodic manual checks.

In practice, integrating SUM, AVERAGE, and IF into a single sheet creates a self-sustaining system. For example, column A lists dates, B shows transaction types, C contains amounts, D calculates net impact (`=IF(B2="Deposit", C2, -C2)`), and E maintains the running balance (`=E1+D2`). This structure, coupled with monthly averages in column F (`=AVERAGE(C$2:C$100)`), offers both granular detail and high-level insights. By mastering these formulas, you transform Excel from a ledger into a proactive financial management tool.

QuickBooks Bank Promo Entry: A Step-by-Step Guide for Easy Redemption

You may want to see also

Explore related products

![]()

Create Charts: Visualize spending trends with pie charts or bar graphs for better insights

Visualizing your spending trends in Excel can transform raw data into actionable insights. Start by selecting the data range that includes your categories (e.g., groceries, utilities, entertainment) and corresponding amounts. Go to the Insert tab and choose a pie chart for a quick overview of where your money is going or a bar graph to track changes over time. Pie charts excel at showing proportions, making it clear which expenses dominate your budget, while bar graphs highlight trends, such as increasing rent or fluctuating dining costs.

When creating charts, ensure your data is clean and organized. Use consistent categories and avoid merging cells, as this can disrupt Excel’s ability to plot accurately. For pie charts, limit categories to 5–7 to prevent clutter; group smaller expenses into an "Other" category if necessary. Bar graphs work best with time-based data, so include a date column (e.g., monthly or quarterly) to track spending patterns. Customize your chart by adding titles, labels, and colors to enhance readability and focus on key areas.

A practical tip is to use conditional formatting in conjunction with charts. For instance, highlight expenses exceeding a certain threshold (e.g., 20% of your income) in red directly in your data table. This makes it easier to identify problem areas before they appear in the chart. Additionally, consider using sparklines for a compact, inline visualization of trends without overwhelming your spreadsheet. These mini-charts are ideal for quick glances at spending fluctuations.

Comparing chart types can help you choose the right one for your needs. Pie charts are ideal for static snapshots, such as analyzing a single month’s expenses, while bar graphs are better for dynamic views, like comparing quarterly spending. For deeper analysis, combine both: use a pie chart to identify the largest expense category and a bar graph to explore its monthly variations. This dual approach provides both breadth and depth in understanding your financial habits.

Finally, leverage Excel’s pivot charts for advanced users. Pivot charts allow you to dynamically filter and segment data, such as viewing expenses by category, month, or payment method. This flexibility is invaluable for uncovering hidden trends, like seasonal increases in travel costs or recurring subscriptions. By mastering these visualization tools, you’ll not only maintain your bank balance but also develop a proactive approach to financial management.

The Evolution of Banking: Diverse Institutions

You may want to see also

Explore related products

![]()

Set Budgets: Allocate funds to categories and monitor progress against predefined spending limits

Effective budget management begins with clear allocation. Divide your income into categories like groceries, utilities, entertainment, and savings. Assign each a realistic spending limit based on historical data or financial goals. For instance, if you spend $400 monthly on groceries, allocate $350 to challenge yourself to save $50. Use Excel’s SUMIF function to track expenses against these limits dynamically. For example, `=SUMIF(Category, "Groceries", Amount)` will tally all grocery expenses, letting you compare them to your $350 cap at a glance.

Monitoring progress requires visual clarity. Create a progress bar in Excel to show how close you are to hitting category limits. Use conditional formatting with a formula like `=D2/E2` (where D2 is spent amount and E2 is budgeted amount) to color-code cells. Green indicates you’re under budget, yellow warns of nearing the limit, and red signals overspending. Pair this with a sparkline chart to visualize spending trends over time, helping you identify patterns like mid-month overspending in dining out.

Automation reduces manual effort and error. Set up IF statements to flag overspending. For example, `=IF(D2>E2, "OVER BUDGET", "OK")` will alert you when a category exceeds its limit. Combine this with pivot tables to analyze spending across months or years. For instance, a pivot table grouping expenses by category and month reveals whether your $100 entertainment budget consistently gets depleted by week two, prompting adjustments.

Flexibility is key to long-term success. Periodically review and adjust budgets based on actual spending. If your $200 utility allocation consistently leaves $50 unused, reallocate that to savings or a category that frequently overshoots. Use Excel’s data validation to create dropdown menus for reallocating funds between categories, ensuring changes are tracked systematically. This iterative approach keeps your budget aligned with evolving priorities.

Finally, integrate accountability into your system. Share your Excel budget with a partner or financial advisor using cloud platforms like OneDrive or Google Sheets. Schedule monthly reviews to discuss progress and make collaborative adjustments. Add a notes column to document reasons for overspending or reallocations, fostering transparency and informed decision-making. A shared, dynamic budget transforms Excel from a tracking tool into a platform for financial teamwork.

How Far is Durango Bank from Your Current Location?

You may want to see also

Explore related products

![]()

Reconcile Statements: Compare Excel records with bank statements to identify discrepancies and errors

Regularly reconciling your Excel records with bank statements is crucial for maintaining an accurate financial picture. Discrepancies, whether from data entry errors, pending transactions, or bank fees, can distort your understanding of your financial health. By systematically comparing your Excel data to official bank statements, you identify these inconsistencies and ensure your records reflect reality.

This process isn't just about catching mistakes; it's about proactive financial management.

Begin by ensuring your Excel spreadsheet is structured for reconciliation. Dedicate columns for date, transaction description, debit amount, credit amount, and running balance. Import or manually enter transactions from your bank statement, ensuring dates and descriptions match as closely as possible. Utilize Excel's sorting and filtering functions to arrange transactions chronologically and by type, making comparisons easier.

Consider using conditional formatting to highlight potential discrepancies, such as negative balances or transactions exceeding a certain threshold.

The core of reconciliation lies in the meticulous comparison of your Excel data with the bank statement. Start from the most recent transaction and work backwards, ticking off each entry in both records. Pay close attention to:

- Dates: Ensure transactions are recorded on the correct dates in both Excel and the statement.

- Amounts: Double-check that debits and credits match exactly. Even small discrepancies can indicate errors.

- Descriptions: While descriptions may vary slightly, they should be recognizable counterparts.

- Pending Transactions: Be mindful of transactions that haven't yet cleared the bank. Note them separately to avoid confusion.

Pro Tip: Use a separate column in Excel to mark reconciled transactions, clearly indicating which entries have been verified.

Discrepancies are inevitable. When you encounter a mismatch, investigate thoroughly. Common causes include:

- Data Entry Errors: Double-check for typos or transposed numbers in your Excel spreadsheet.

- Bank Fees or Interest: Ensure these are accounted for in your Excel records.

- Pending Transactions: Verify if the missing transaction is still processing.

- Duplicate Entries: Check for accidental double-recording of transactions.

Once identified, rectify errors promptly. Update your Excel spreadsheet to reflect the correct information and ensure your running balance is accurate. Important: Maintain a record of all adjustments made during reconciliation for future reference and audit purposes.

Regular reconciliation, done diligently, transforms your Excel spreadsheet from a simple record-keeper into a powerful tool for financial control and insight.

Does M&T Bank Accept Loose Coins? A Comprehensive Guide

You may want to see also

Frequently asked questions

Start by creating columns for Date, Description, Income, Expenses, and Balance. Enter your transactions under Income and Expenses, then use a formula like `=SUM(Income)-SUM(Expenses)` or a running balance formula (`=PREVIOUS CELL + Income - Expenses`) to calculate the Balance.

Use a running balance formula in the Balance column, such as `=D2+E2-F2` (assuming D is Income, E is Expenses, and F is the previous balance). Copy this formula down the column to automatically update the balance for each new transaction.

Add a Category column next to Description. Use conditional formatting or filters to group transactions by type (e.g., groceries, utilities, entertainment). You can also create pivot tables to analyze spending patterns.

Compare your Excel Balance column with your bank statement. Highlight unmatched transactions in Excel using conditional formatting or manually check for discrepancies. Adjust entries as needed to ensure both balances match.