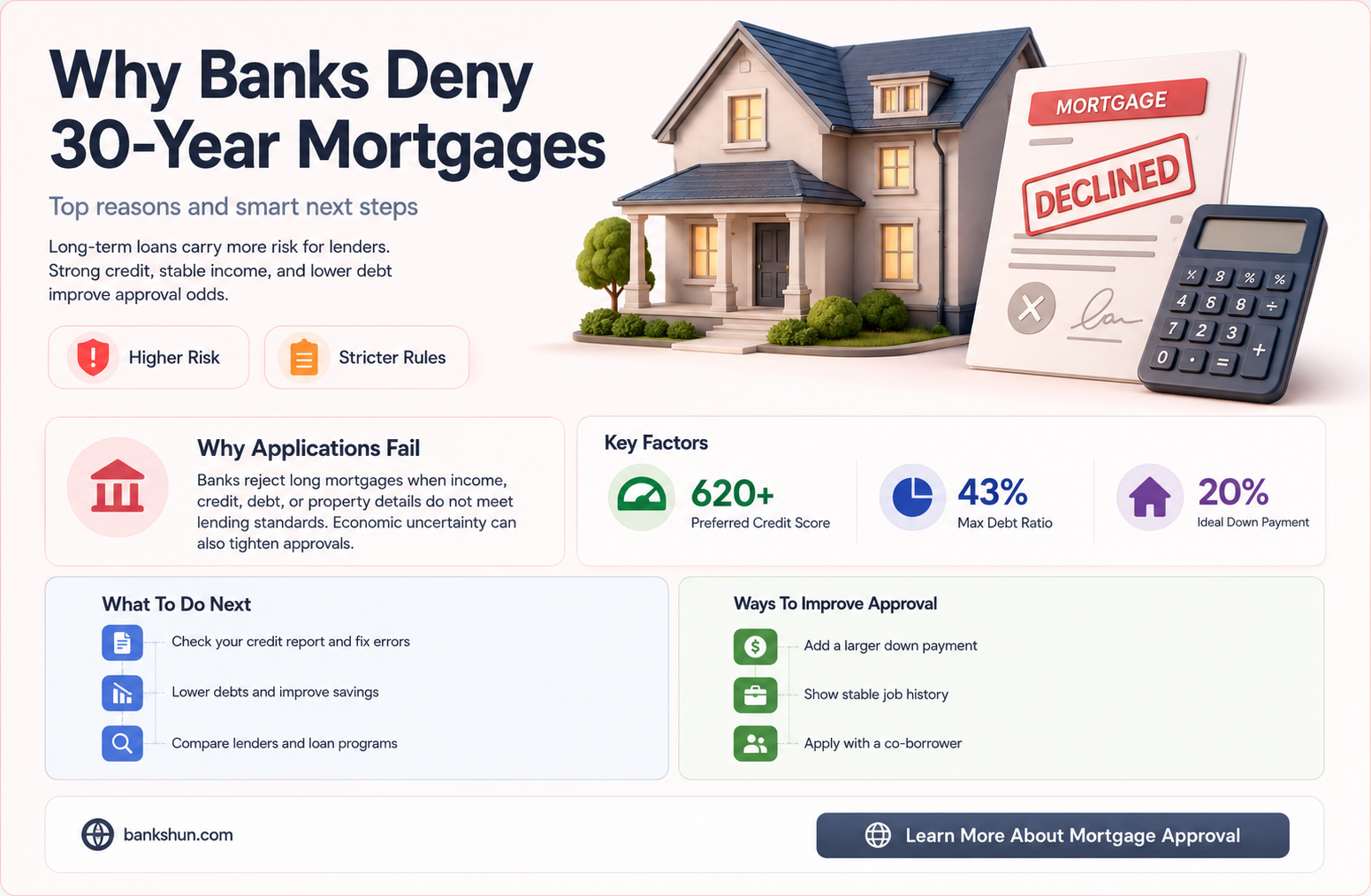

Banks may deny a 30-year mortgage for various reasons. While age is not a valid reason for denial, with strong anti-discrimination laws in place, income verification and debt-to-income requirements are crucial factors. Additionally, redlining, a discriminatory practice based on location and the racial makeup of a neighborhood, has been a persistent issue in the US, leading to lawsuits against several banks. Other reasons for mortgage denial include the property's appraised value being lower than the agreed-upon price and the absence of a cosigner.

Explore related products

What You'll Learn

![]()

High debt-to-income ratio

A high debt-to-income ratio (DTI) is a common reason for banks to deny mortgage applications. DTI is the percentage of your monthly gross income that goes towards paying off debts such as credit cards, loans, and other monthly payments. Lenders use this ratio to assess whether you can afford to take on additional debt and manage the payments. A low DTI reflects a good balance between income and debt, making you a more attractive candidate for a loan.

Lenders typically consider two types of DTI: front-end and back-end. The front-end ratio includes only housing-related expenses, such as potential monthly mortgage payments, property taxes, insurance, and HOA fees, relative to your gross monthly income. This is calculated by adding up your monthly housing expenses, dividing it by your gross monthly income, and multiplying the result by 100. Lenders often prioritise other factors in mortgage applications, so the front-end ratio is less commonly used.

The back-end ratio is more commonly used as it provides a comprehensive view of your creditworthiness and monthly debt obligations. It includes all your monthly debt payments, such as credit cards, student loans, personal loans, car loans, alimony, and child support, in addition to the mortgage payment. To calculate your back-end DTI, add up all your monthly debt payments, divide the sum by your monthly gross income, and convert it into a percentage.

While the ideal front-end ratio is considered to be no more than 28%, and the back-end ratio no higher than 36%, lenders may approve borrowers with higher DTIs. In some cases, they may go as high as 50%, but this often requires compensating factors such as a strong credit history, financial reserves, or a higher down payment. Additionally, certain loan types, such as FHA and VA loans, typically allow for higher DTIs. However, a high DTI may result in less favourable interest rates and terms.

If you have a high DTI, there are several strategies you can employ to improve your chances of mortgage approval. These include paying off existing debts, increasing your income, purchasing a lower-priced home, or involving a spouse or partner with a lower DTI in your loan application. You can also explore alternative financing options from credit unions, online lenders, or community banks, which may have more flexible criteria.

Bank Deposits: Are Your Savings Safe?

You may want to see also

Explore related products

![]()

Poor credit score

A poor credit score can reduce your chances of getting a 30-year mortgage. Credit scores are a significant factor in determining whether an individual will be able to secure a mortgage and the interest rate they will pay. A higher credit score reflects a better credit history and makes borrowers eligible for lower interest rates. Most mortgage lenders use FICO scores, which are calculated based on information in an individual's credit report. This includes factors such as payment history, credit card debt, and the length of their credit history.

Lenders also use the debt-to-income (DTI) ratio to assess whether a borrower can afford mortgage payments. Taking on new debt during the loan closing process can impact this ratio and reduce the chances of mortgage approval. Additionally, applying for multiple new credit accounts in a short period can negatively affect an individual's credit score, further reducing the likelihood of mortgage approval.

However, there are steps that individuals with poor credit scores can take to improve their chances of securing a 30-year mortgage. Firstly, it is important to review one's credit report for any errors and have them corrected. Secondly, individuals can focus on improving their credit score by paying down credit card debt, maintaining a positive payment history, and reducing the number of new credit accounts opened. Additionally, seeking lenders that specialize in loans for borrowers with credit challenges or exploring different mortgage programs with lower credit score requirements, such as Federal Housing Administration (FHA) loans, can increase the chances of approval.

Banks' Risk of Failing: Who's Next?

You may want to see also

Explore related products

![]()

Low income

While it can be challenging to obtain a 30-year mortgage with a low income, it is not impossible. Banks generally cannot deny your loan application based on age or income level. Instead, they evaluate your ability to repay the loan by considering your financial criteria, including credit history, debt-to-income (DTI) ratio, income, and assets.

To improve your chances of obtaining a 30-year mortgage with a low income, aim for your mortgage payment to be less than 28% of your gross income and maintain a DTI ratio of 45% or less. Lenders view a lower DTI ratio favourably, as it indicates a stronger ability to repay the loan. You can improve your DTI ratio by consistently paying your bills on time and working on reducing your debt. Additionally, consider seeking assistance from co-signers, who can provide additional financial security for the lender.

There are also various loan options and programs specifically designed to help low-income individuals. These include federal, state, county, or local government agencies, nonprofits, or employers that offer loans, grants, tax credits, and down payment assistance. For example, the American Dream program assists buyers with limited resources, especially those with low-to-moderate incomes. Private lenders may also be an option, as they often have more flexibility with loan requirements and may accept lower credit scores or higher debt-to-income ratios.

Remember, it is your legal right to understand the reasons for any loan denials, and you can request a detailed explanation from the lender. By understanding these reasons, you can take steps to improve your financial situation and increase your chances of obtaining a 30-year mortgage in the future.

Bank Employees: Vaccination Requirements and the Law

You may want to see also

Explore related products

![]()

Incomplete or unverifiable information

Banks and lenders have been known to deny 30-year mortgages due to incomplete or unverifiable information. Incomplete credit applications make up over a tenth of mortgage rejections, while unverifiable information makes up 4.29%.

Lenders require extensive documentation of a borrower's financial history, including their employment history and credit history. If an application lacks all the required information, the lender will deny the application and report an "Incomplete credit application" as the reason. Lenders must verify the information provided, and if they cannot, they will deny the application and report "Unverifiable information" as the reason. This could be due to undisclosed loans or large account transfers, or the lender finding information that the applicant hasn't explained.

To avoid denial due to incomplete information, applicants should ensure they provide all the necessary documentation, including pay stubs, tax returns, bank statements, and other financial records. They should also ensure that all essential personal details, such as employment history and contact information, are included in the application. Lenders may also require two months of bank statements to prove that the borrower has the funds for a down payment.

To avoid denial due to unverifiable information, applicants should ensure that all their credit, employment, income, and residential documentation is up-to-date and in line with what the lender needs. Lenders use bank statements to verify that the borrower can afford the down payment, closing costs, and future mortgage payments, as well as consistent income and any activity that may indicate financial risk. They also assess the borrower's spending habits, account stability, risk assessment, and fraud detection.

It is important to note that racial disparities exist in the reasons given for mortgage denials. Black, Latino, and Asian applicants are more likely to be denied due to unverifiable information compared to similar White applicants.

How to Deduct Bank Fees on Form 1041

You may want to see also

Explore related products

![]()

High-risk area or issues with the house

Banks can deny a 30-year mortgage if the house is in a high-risk area or has issues. Lenders require insurance to protect their investments. If you're looking to buy a house in a high-risk area and can't find a homeowners insurance company to cover it, the lender probably won't give you a loan to buy it.

Insurers of last resort, like California's, have run out of money and been bailed out. Premiums have risen by more than 50% in some of the highest-risk zip codes in the US since the start of COVID. It is difficult to find private insurers willing to write policies in many of these areas.

Insurers and banks could exit these markets, making it harder to get a mortgage. Banks are already making changes to reduce their risk exposure, such as increasing the down payment for coastal and high-risk areas, decreasing the LTV ratio, and selling high-risk mortgages to the secondary market.

Additionally, if the house has serious problems, it may be unmortgageable. For instance, if the house appraises for less than you're paying, you could be turned down for a loan unless you can come up with extra money. Most mortgage lenders won't loan more than around 90% of the fair market value of a home.

Banks' Responsibility in Auto Dealer Fraud

You may want to see also

Frequently asked questions

No, it is illegal for banks to deny a 30-year mortgage based on age. The Equal Credit Opportunity Act (ECOA) prohibits lenders from denying credit based on age.

No, it is illegal for banks to deny a mortgage based on race. The Fair Housing Act of 1968 states that it is against the law to discriminate in any residential real estate transaction. However, Black and Hispanic individuals are denied home loans at nearly twice the rate of white individuals, indicating that discrimination may still occur.

Taking out a mortgage is a long-term commitment, and income may be sporadic at an older age. Seniors may find it challenging to make mortgage payments alongside other expenses on a fixed income.

Alternatives to a 30-year mortgage include a 15-year or 20-year mortgage. These options typically require higher monthly payments but result in paying less interest over time.

If your mortgage application is denied, you can try to find a loan elsewhere or get a cosigner to improve your chances of qualification. You can also work on improving your financial situation and creditworthiness before reapplying.