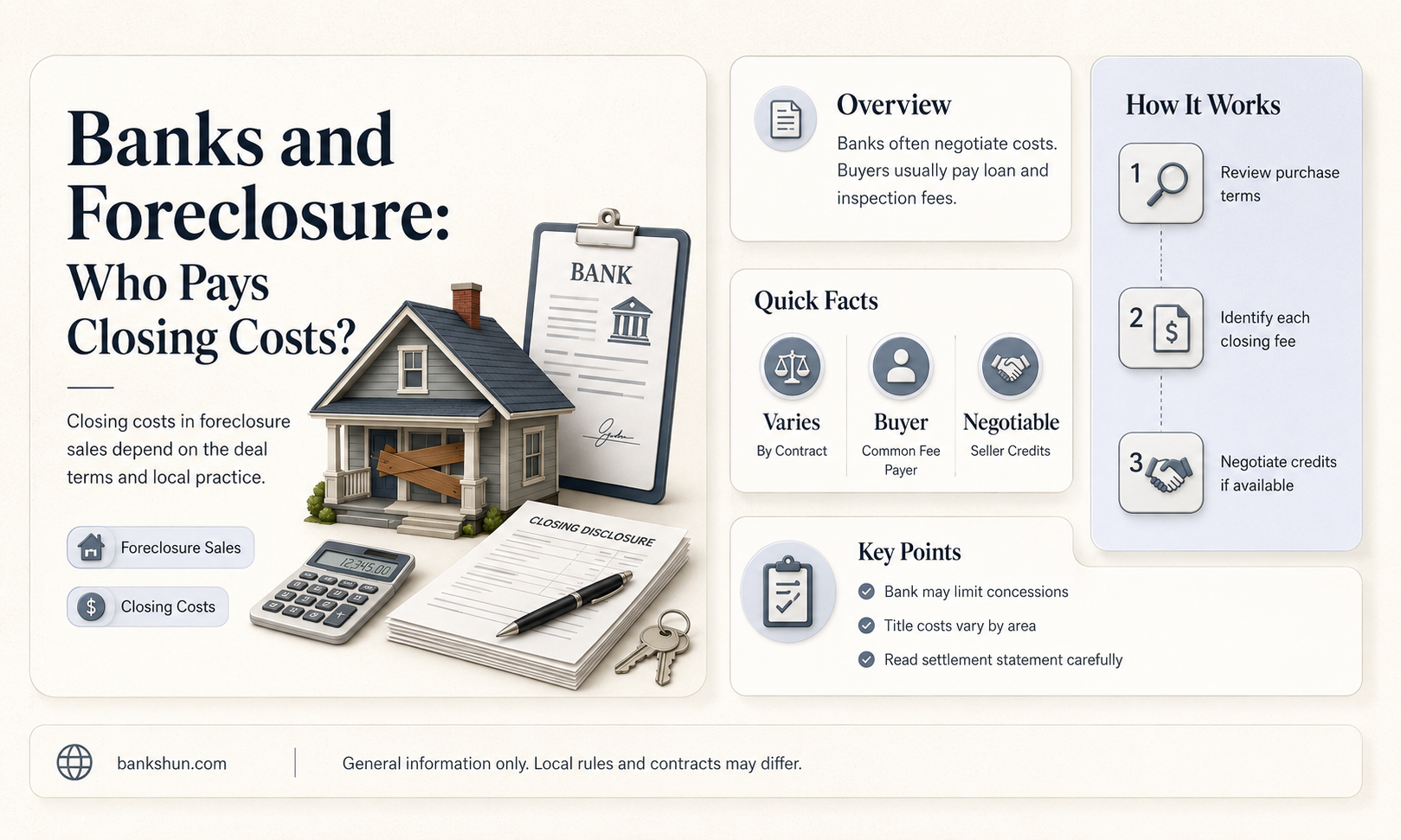

Foreclosed homes are often sold below market price, making them an attractive option for buyers on a budget. However, it is important to consider the potential for hidden costs, such as closing costs, which are fees added to the purchase price of a home. Closing costs are typically paid by both the buyer and the seller, and they can vary by lender, ranging from $50 to $500. In the case of a foreclosure, the bank may be motivated to sell the property quickly and may be willing to negotiate on closing costs. Additionally, the bank may pay for repairs to make the home inhabitable, but other problems may be left for the buyer to handle.

| Characteristics | Values |

|---|---|

| Who pays closing costs? | Buyer and seller |

| Can banks pay closing costs on foreclosures? | Banks may pay for repairs to make a foreclosed home habitable, but other problems are left for the new owner to handle. |

| How to lower closing costs | Negotiate with the seller or lender, or roll the costs into the total amount of your loan. |

| What do closing costs include? | Real estate agent commissions, appraisal fees, inspection fees, title search, tax monitoring services, insurance, and other fees. |

| Cost range | $50 to $500, depending on the lender |

Explore related products

What You'll Learn

![]()

Foreclosed properties are often sold below market price

When purchasing a foreclosed property, it's essential to understand that closing costs will still apply. Closing costs are the fees associated with finalizing a real estate transaction, and they can include expenses such as real estate agent commissions, appraisal fees, inspection fees, and various other charges. These costs are typically paid by both the buyer and the seller, and they can add up to a significant amount. While it's uncommon for banks to cover these costs, it's not impossible, especially if the property has been on the market for a long time.

In some cases, the bank may be willing to negotiate on closing costs, especially if the property has been sitting on their books for an extended period. This is because the longer a foreclosed property remains unsold, the more it costs the bank in maintenance, taxes, and other carrying costs. Therefore, buyers with a keen eye for negotiation may be able to persuade the bank to waive or reduce certain closing costs. However, it's important to remember that the bank's primary goal is to minimize its losses, so they may not always be flexible on these fees.

Additionally, it's worth noting that foreclosed properties may come with hidden problems. As previously mentioned, these homes are typically sold "as-is," and the bank may not be aware of or disclose all issues with the property. This means that buyers could inherit unknown problems, such as structural damage, pest infestations, or even legal issues like outstanding liens or unpaid taxes. Conducting a thorough title search and inspection can help uncover potential red flags, but it's ultimately the buyer's responsibility to perform due diligence and ensure they are comfortable with the risks involved.

Overall, while foreclosed properties can offer the opportunity to purchase a home below market value, it's important to approach these transactions with caution. Buyers should carefully consider the potential hidden costs, perform thorough inspections, and be prepared to negotiate with the bank to ensure they are getting a fair deal. By understanding the unique dynamics of purchasing a foreclosed property, buyers can make informed decisions and potentially secure a great deal on their new home.

Mortgage Denial: Age Discrimination in Banks?

You may want to see also

Explore related products

![]()

Vacant properties are subject to neglect, vandalism and theft

Vacant properties are subject to a host of issues, primarily neglect, vandalism, and theft. These properties are often left unoccupied for extended periods, leading to various challenges. Firstly, neglect can set in as routine maintenance and upkeep are neglected, leading to issues such as overgrown gardens, broken windows, or damaged roofs. This neglect can also lead to more severe problems, such as water damage or pest infestations, which can be costly to repair.

Vandalism is another significant concern for vacant properties. Unfortunately, vacant homes are often targets for vandals, who may break in, causing damage and leaving the property in a state of disrepair. In some cases, as mentioned, even the previous homeowners facing foreclosure have been known to vandalize their own homes out of anger before eviction. This vandalism can range from minor incidents, such as broken windows, to more severe cases of structural damage, posing safety hazards and requiring extensive repairs.

Theft is also a common issue with vacant properties. Without a regular presence at the property, thieves may target the home, stealing anything from appliances to copper wiring, causing significant financial loss to the owner. In some instances, thieves may even strip the home of essential components, such as plumbing or electrical fixtures, leaving behind extensive damage.

Additionally, vacant properties may face issues with squatters. These individuals may occupy the property illegally, causing damage and creating legal complications for the rightful owner. Dealing with squatters can be a lengthy and costly process, further burdening the owner.

To mitigate these issues, banks may step in to perform necessary repairs to make a vacant, foreclosed property inhabitable and more appealing to potential buyers. However, it's important to note that banks are not always aware of all the problems a foreclosed property may have, and they may not disclose known issues. As such, buyers should exercise caution and conduct thorough inspections before purchasing a foreclosed home.

Bank Errors: How Do They Affect Company Books?

You may want to see also

Explore related products

![]()

The bank may pay for repairs to make a home habitable

When a bank takes possession of a foreclosed home, it incurs various closing costs, including repairs to make the property habitable and marketable. While banks typically prefer to sell properties "as-is," in some cases, they may be willing to cover repair expenses to expedite the sale and minimize their holding costs. Here are some scenarios where a bank may consider paying for repairs:

- Habitability Issues: If a foreclosed home has significant issues that affect its habitability, such as unsafe electrical wiring, plumbing problems, roof leaks, or structural damage, the bank may be motivated to address these issues. Repairs that ensure the property meets basic safety and health standards can make it more attractive to potential buyers and help the bank sell the property faster.

- Increasing Property Value: In some cases, banks may strategically invest in select repairs or improvements to boost the property's value and marketability. This could include cosmetic updates, such as fresh paint, landscaping, or minor renovations. By investing in these repairs, the bank can potentially increase the selling price and recoup the costs upon sale.

- Negotiating Leverage for Buyers: Buyers interested in purchasing a foreclosed home can leverage the bank's desire to offload the property. During the negotiation process, buyers may request that the bank cover specific repair costs or offer a credit at closing. This approach can be particularly effective if the needed repairs are significant and affect the buyer's ability to obtain financing.

- Local Laws and Regulations: Depending on local laws and regulations, banks may be required to bring foreclosed properties up to certain safety and habitability standards before they can be sold. These requirements vary by jurisdiction, and banks must comply with applicable codes and ordinances. Failure to do so could result in fines or legal consequences.

- Protecting the Property's Value: In some instances, the bank may view necessary repairs as a means to protect the property's value and prevent further deterioration. For instance, if a foreclosed home has a leaking roof, the bank may choose to repair it promptly to avoid more extensive (and costly) water damage. By addressing critical issues, the bank can maintain the property's condition and market value.

- Bulk Sales and Investor Purchases: When banks sell multiple foreclosed properties in bulk to investors or companies, there may be negotiations regarding repair costs. In these transactions, the bank might agree to cover specific repairs or provide a discount that effectively allows the buyer to address the necessary fixes.

It is important to note that banks' willingness to pay for repairs varies and is often assessed on a case-by-case basis. Buyers interested in purchasing foreclosed properties should carefully inspect the home, identify necessary repairs, and negotiate with the bank accordingly. Real estate agents experienced in foreclosure sales can also provide valuable guidance on navigating these transactions and understanding the bank's role in covering closing costs and repairs.

The Grand Banks: A Dangerous, Foggy, and Treacherous Triangle

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![]()

The seller may be willing to negotiate on closing costs

When buying a house, closing costs are a part of every home loan and are paid by both the buyer and the seller. Closing costs include various fees, such as real estate agent commissions, appraisal fees, and inspection fees. These costs are typically outlined in the loan estimate provided by the lender.

In the case of a foreclosed property, the bank acts as the seller. While the bank may pay for repairs to make the home inhabitable, it is not always aware of all the problems with the property and may not disclose them. As a result, buyers of foreclosed properties may face unexpected costs.

When purchasing a foreclosed property, it is worth noting that the seller (the bank) may be willing to negotiate on closing costs, especially if a significant amount of time has passed since the foreclosure. In such cases, the bank may be eager to offload the property and could be open to reducing or eliminating the buyer's closing costs.

However, if the seller is not willing to negotiate on closing costs, buyers have other options. One option is to discuss the situation with their mortgage lender, who may be willing to include the closing costs in the total loan amount. While this approach can result in higher monthly payments and interest rates, it can be a viable solution for buyers who are short on cash in the short term.

Additionally, buyers can seek professional advice from real estate agents or lawyers. Real estate agents can guide buyers through the negotiation process and help them navigate the potential costs associated with the property. Lawyers, on the other hand, can provide legal expertise and assist with documentation, ensuring buyers are aware of any hidden charges or potential issues with the property.

Venmo and Cash Advances: What Banks Really Think

You may want to see also

Explore related products

![]()

Closing costs can be rolled into the total loan amount

When buying a house, closing costs are typically 3%–6% of the total loan balance. These costs are usually paid out of pocket, but they can sometimes be rolled into the total loan amount. This option is available if your total loan amount is below the bank's loan limits and if you do not exceed certain ratios like debt-to-income. Rolling closing costs into the loan may result in a higher monthly payment and a higher interest rate over time.

Closing costs are processing fees paid to the lender when a loan is closed. These costs include appraisal fees, attorney fees, and inspection fees. When buying a house in foreclosure, closing costs are still required, but they may be lowered or avoided depending on the circumstances. For example, if a significant amount of time has passed since the lender foreclosed on the property, the bank may be eager to sell the property and may be willing to negotiate on closing costs.

Additionally, the buyer may be able to negotiate with the seller to help cover closing costs as part of their concessions. For conventional loans, the maximum amount of seller concessions for an investment property is 2%. For FHA loans, the contribution limit on seller concessions is 6% based on the appraised value or purchase price of the house, whichever is lower. VA loan seller concessions have different rules depending on what they are being applied to, but they can be applied to various fees up to 4% of the total loan amount.

It is important to note that rolling closing costs into the loan is not always possible. It depends on the mortgage program and the specific closing costs in question. Some programs do not permit this as it can affect the debt-to-income ratio. Therefore, it is essential to discuss options with the lender and real estate agent to understand the specific closing costs and whether they can be included in the total loan amount.

Strict Penalties for Non-Compliance: Banks Under Regulatory Scrutiny

You may want to see also

Frequently asked questions

Banks do not typically pay closing costs on foreclosures. However, if the property has been vacant for a long time, the bank may be willing to negotiate on closing costs.

Closing costs are fees that are paid when a real estate transaction closes. They are paid by both the buyer and the seller and can include real estate agent commissions, appraisal fees, and inspection fees.

There are a few ways to lower closing costs. You can negotiate with the seller or lender, or you can shop around for a lender that offers lower closing costs. You may also be able to roll the closing costs into the total amount of your loan, but this will result in higher monthly payments and a higher interest rate.