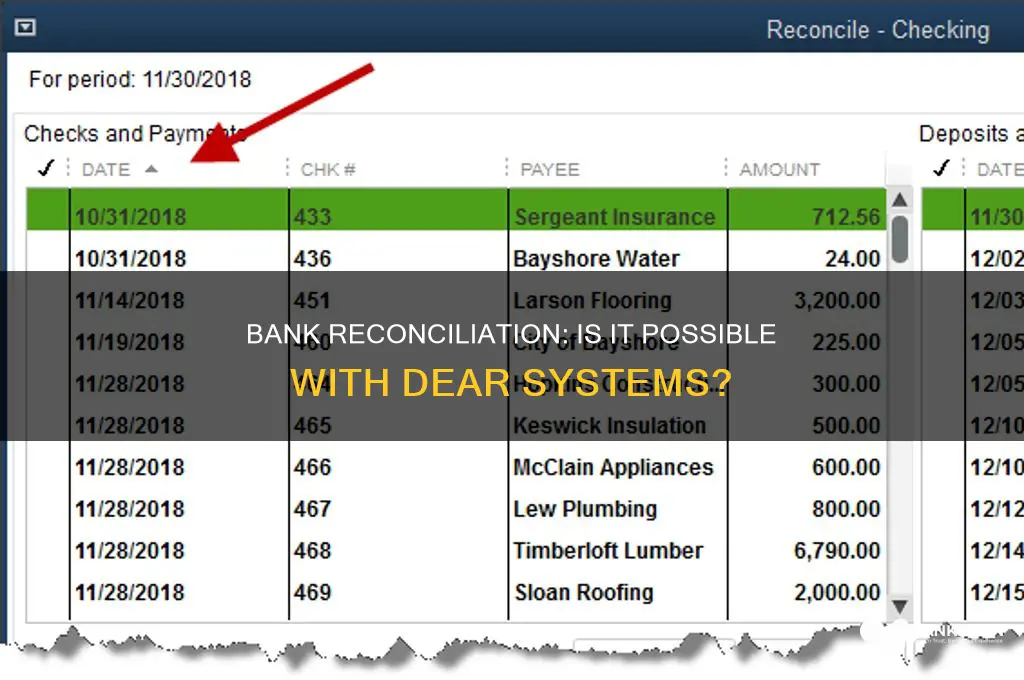

Bank reconciliation is the process of comparing the transactions in a bank statement to the transactions in one's records to ensure that they match. This process is important for detecting errors and preventing fraud, and it is usually performed monthly. DEAR Systems, a platform that helps businesses manage their finances, also has a bank reconciliation feature. After importing bank transactions into DEAR, users can review and match these transactions with those in DEAR, allowing them to verify the accuracy of their financial records.

Explore related products

What You'll Learn

![]()

Bank reconciliation is a process of matching transaction data between multiple systems

Bank reconciliation is a critical process for businesses to ensure the accuracy of their financial records and detect any errors or discrepancies. It is also an important tool for fraud detection and prevention. By regularly performing bank reconciliation, businesses can identify any fraudulent activities, such as unauthorised transactions, and take necessary actions. This process is usually done monthly, but businesses with a high volume of transactions may opt for a more frequent reconciliation, such as weekly or daily.

The process of bank reconciliation typically involves gathering financial records, including bank statements, invoices, financial statements, and cash books. These documents are then used to compare the ending cash balance of bank accounts with internal financial records. Transactions such as deposits, withdrawals, transfers, and payments are matched between the two sets of records to ensure they align.

DEAR Systems, a cloud-based accounting platform, also offers bank reconciliation capabilities. After importing account transactions from a bank, users can utilise the platform's features to match transactions between their bank statements and DEAR. This process ensures that the transactions in both systems align and provides users with a comprehensive view of their financial activities.

Bank reconciliation is a critical function for maintaining accurate financial records and ensuring the proper stewardship of funds. It helps businesses, governments, and individuals detect errors, prevent fraud, and make informed decisions about their finances. By regularly performing this process, organisations can identify discrepancies, ensure compliance, and gain valuable insights into their cash flow and transaction history.

Bank Appraisals: High or Low?

You may want to see also

Explore related products

![]()

It helps to identify and prevent errors

Bank reconciliation is a process that helps identify and prevent errors. It involves comparing the transactions in a bank statement to those in a company's internal records. This process is important because it helps to ensure the accuracy of financial records and can help detect errors or fraud.

DEAR Systems, an accounting software, also has a bank reconciliation feature. After importing account transactions from your bank into DEAR, you need to reconcile them to ensure that the transactions match. This process can be done manually or automatically using Bank Rules. By creating rules, DEAR will automatically suggest matches between transactions, allowing for efficient reconciliation.

Reconciliation is a critical process for businesses to ensure accurate financial reporting and compliance. It helps businesses identify errors in their records, such as missing transactions or discrepancies in amounts. For example, a company might record a payment in its ledger, but the payment might not leave their bank account for several days due to delays in payment methods. This lag can cause temporary differences between the company's reported net income and the actual balance in their bank account.

Bank reconciliation also helps prevent fraud and ensures fiscal responsibility. By regularly performing reconciliations, businesses can detect fraudulent activity and ensure the timely creation of accurate financial records. It is recommended that businesses conduct reconciliations at least once a month or more frequently if they have a high volume of transactions.

Additionally, bank reconciliation can help improve balance sheet accuracy. By reconciling transactions, businesses can ensure that the amounts recorded on their balance sheets correspond to the transactions in their financial accounts. This process also helps confirm accounts receivable by identifying any outstanding customer debts. Overall, bank reconciliation is a valuable tool for businesses to maintain accurate financial records, detect and prevent errors, and ensure compliance.

Foreign Transaction Fees: Are All Banks Created Equal?

You may want to see also

Explore related products

![]()

It aids in fraud detection

Bank reconciliation is a process that compares a company's internal financial records to its bank statements. This process is available in DEAR Systems, where users can reconcile account transactions from their bank with transactions in DEAR.

Bank reconciliation plays a crucial role in fraud detection and prevention. Here's how it aids in fraud detection:

Verifying Accuracy

Bank reconciliation helps verify the accuracy of financial records. By cross-referencing bank accounts and financial records, companies can ensure that all transactions, including checks, deposits, transfers, and withdrawals, are legitimate and authorized. This process helps identify any fraudulent or unauthorized transactions, allowing businesses to take prompt action.

Detecting Discrepancies

Through bank reconciliation, organizations can identify discrepancies between their internal records and bank statements. This includes identifying missing transactions, incorrect amounts, or uncleared transactions. By investigating these discrepancies, businesses can uncover potential fraudulent activities and address them promptly.

Enhancing Security

Regular bank reconciliation ensures that financial records are accurate and secure. By staying on top of reconciliations, organizations can maintain better control over their cash flow and funds. This proactive approach helps minimize financial risks, protect against overdrafts, and enhance operational efficiency.

Streamlining Investigations

Bank reconciliation provides a comprehensive overview of financial activities, making it easier to investigate potential fraud. With all transactions in one place, auditors and accountants can quickly identify suspicious patterns or anomalies, enabling timely detection and resolution of fraudulent activities.

Automating Fraud Detection

With the advent of bank reconciliation software, fraud detection has become more efficient. These software tools use algorithms to automatically match transactions and flag discrepancies. By eliminating manual processes, organizations can detect issues in real-time, enhancing their ability to prevent and mitigate fraud.

In conclusion, bank reconciliation is a powerful tool in the fight against fraud. By regularly reconciling accounts, organizations can verify the accuracy of their financial records, detect discrepancies, enhance security, streamline investigations, and leverage automation to stay ahead of fraudulent activities. This process is integral to maintaining fiscal responsibility and safeguarding assets.

Bank Security: 24/7 Guard Presence for Ultimate Protection

You may want to see also

Explore related products

![]()

It is used to track expenses

Bank reconciliation is a feature of DEAR Systems. After account transactions from your bank have been imported into DEAR, you need to reconcile them to make sure that the transactions from your bank statement and the transactions in DEAR match.

DEAR Systems can be used to track expenses. It integrates with accounting apps like Xero and QuickBooks, automatically creating entries and syncing invoices, bills, payments, and more. DEAR also has a full trial balance and a GL backend. When using Location as the tracking category, the value on the Order Header is used, not the location of the actual pick. DEAR can also be used to create a detailed Bill of Materials for your inventory and subassemblies, giving you a true picture of raw material, labour, and overhead costs.

There are several ways to track expenses. One way is to record every dollar you spend with an app, a notepad, a spreadsheet, or by reviewing bank and credit card statements. You can then categorize those expenses and set budgeting limits to help you reach your financial goals. You can also use a free budgeting app with expense-tracking functions, which typically enables you to track spending across various bank, credit card, and investment accounts.

Another way to track expenses is to make a spreadsheet. You can schedule a time, perhaps every day or every week, to plug all your expenses into the spreadsheet. You can also hang on to all of your receipts and bills and check your bank statements and credit card statements to make sure you don't miss a charge.

It is important to note that when you start expense tracking, you will have a lot of data to work with. As a next step, put your expenses into categories. Divide them into fixed versus variable expenses first, then sort them further based on the type of charge.

Recording Donations: Bank Ledger Management

You may want to see also

Explore related products

![]()

Bank reconciliation helps to ensure the proper stewardship of public monies

Bank reconciliation is a process that compares the transactions listed in a bank statement to the transactions recorded in the general ledger. It is a key internal control that helps ensure the proper stewardship of public monies.

In the context of DEAR Systems, bank reconciliation involves matching transactions imported from a bank account with transactions in DEAR. This process is important for ensuring that the transactions in DEAR accurately reflect the financial activity in the associated bank account. By performing bank reconciliation, businesses and individuals can detect errors, prevent fraud, and ensure the accuracy of their financial records.

DEAR Systems offers tools to facilitate bank reconciliation, such as the ability to create and apply rules for automatic reconciliation. Users can review imported transactions, match them with corresponding transactions in DEAR, and make any necessary adjustments. This process helps to ensure that the financial records in DEAR are up-to-date and accurate, which is crucial for effective financial management and decision-making.

The frequency of bank reconciliation depends on the volume of transactions and the complexity of accounting needs. It is generally recommended to perform bank reconciliation at least once a month. However, organisations with a high volume of transactions may benefit from more frequent reconciliations, such as weekly or even daily, to improve cash flow management and promptly identify and address any discrepancies.

By adopting a regular bank reconciliation process, organisations demonstrate their commitment to fiscal responsibility and the proper stewardship of public monies. This process helps to maintain accurate financial records, detect and prevent fraud, and facilitate timely financial reporting and audits. It is a critical internal control mechanism that contributes to the overall financial health and accountability of an organisation.

Digital Currency: Banks' Inevitable Future?

You may want to see also

Frequently asked questions

Bank reconciliation is the process of verifying the completeness of a transaction by matching a company’s balance sheet to its bank statement.

After account transactions from your bank have been imported into DEAR, you need to reconcile them to make sure that the transactions from your bank statement and the transactions in DEAR match.

Businesses conduct reconciliations once per month, or more frequently if they have a high volume of transactions.

Bank reconciliation helps businesses accurately report taxable income, boosts efficiency and productivity, and helps detect fraud and errors.

To perform bank reconciliation, you need to gather your financial records, including your bank statement(s) and any internal records. Compare the ending cash balance of your bank accounts to your internal financial records and match your deposits, credits, withdrawals, invoice payments, interest charges, and bank fees.